NetEase (SEHK:9999) continues to leverage its financial health and innovative product offerings to maintain a strong market position, as evidenced by its high return on equity and recent successful game release. However, challenges such as rising costs and potential shareholder dilution may constrain growth, requiring strategic cost management and careful navigation of regulatory changes. In the following discussion, we will explore how NetEase's strategic initiatives and market conditions are expected to impact its future performance.

Core Advantages Driving Sustained Success for NetEase

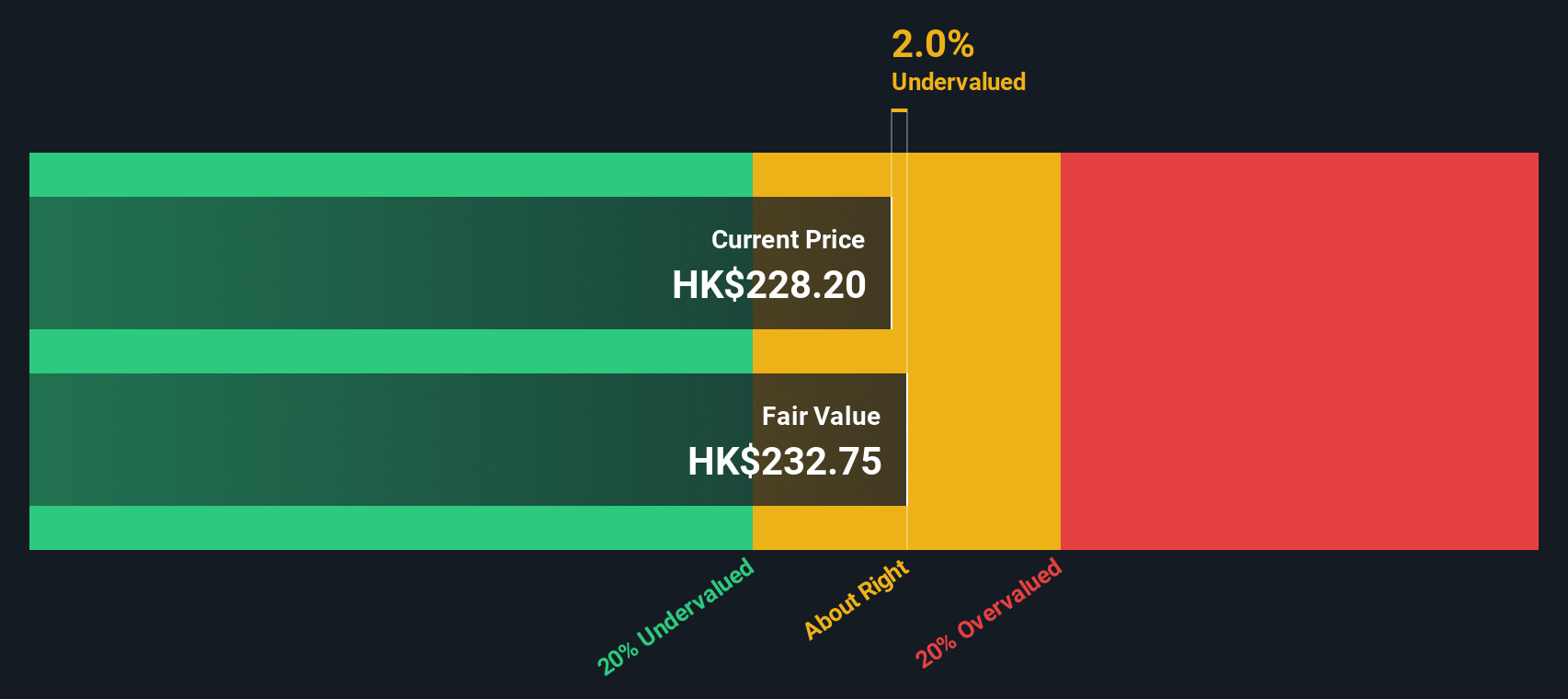

With a high Return on Equity of 21.7%, NetEase demonstrates effective management and profitability. The company's earnings growth of 12.3% surpasses the Entertainment industry average of 10.1%, reflecting its strong market position. Product innovation, such as the latest game release achieving over 5 million downloads, showcases NetEase's commitment to responding to market demands. The company's financial health is sound, with more cash than total debt, and a low dividend payout ratio of 39.6% ensures sustainable dividends. Additionally, NetEase is trading at HK$123.6, significantly undervalued compared to its estimated fair value of HK$246.54, indicating potential for stock price appreciation.

NetEase faces challenges such as a slower expected revenue growth of 7.3%, which lags behind the Hong Kong market's 7.7% growth. The management team, with an average tenure of 1.4 years, may lack the experience needed to navigate complex market dynamics. Shareholder dilution, with a 3.1% increase in total shares outstanding, could impact investor confidence. Rising costs, noted by a 10% increase in the cost of goods sold, pressure margins, necessitating improved cost management strategies.

Potential Strategies for Leveraging Growth and Competitive Advantage

Analysts forecast a target price more than 20% higher than the current share price, highlighting potential appreciation. The company's significant discount to its estimated fair value presents an opportunity for strategic investments. Continued profit and revenue growth, forecasted at 7.88% per year, positions NetEase to capitalize on emerging opportunities. Strategic alliances and product-related announcements could further enhance market position and drive expansion.

NetEase must navigate economic headwinds and regulatory hurdles that could impact performance. Changes in gaming regulations may affect operations, requiring agility in strategy adjustments. Supply chain vulnerabilities pose risks to production schedules, necessitating robust mitigation strategies. Additionally, competitive pressures in the gaming sector demand continuous innovation to maintain market share.

NetEase's strong Return on Equity of 21.7% and earnings growth of 12.3% underscore its effective management and solid market position, which are critical for sustaining profitability in the competitive entertainment sector. The company's strategic focus on innovation and financial health, evidenced by more cash than debt and a sustainable dividend payout, positions it well for future growth. Trading at HK$123.6, significantly below its estimated fair value of HK$246.54, suggests a substantial opportunity for stock price appreciation, especially with analysts forecasting a target price over 20% higher. This undervaluation, combined with potential strategic alliances and product expansions, indicates that NetEase is poised to capitalize on emerging opportunities and enhance shareholder value, provided it effectively navigates external economic and regulatory challenges.

Seize The Opportunity

Are you invested in NetEase already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Valuation is complex, but we're here to simplify it.

Discover if NetEase might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Simply Wall St analyst Simply Wall St and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

About SEHK:9999

NetEase

Engages in online games, music streaming, online intelligent learning services, and internet content services businesses in China and internationally.