Advertisement

Does Bison Finance Group (HKG:888) Have A Healthy Balance Sheet?

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, Bison Finance Group Limited (HKG:888) does carry debt. But the real question is whether this debt is making the company risky.

What Risk Does Debt Bring?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

View our latest analysis for Bison Finance Group

How Much Debt Does Bison Finance Group Carry?

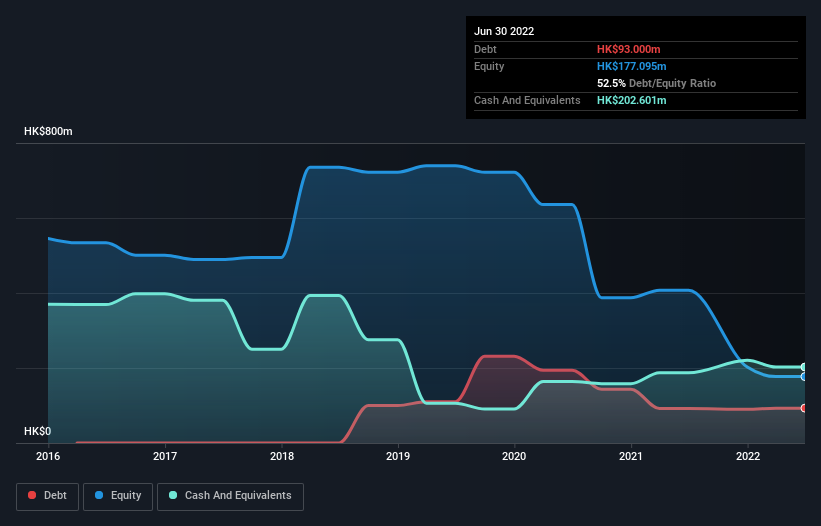

The chart below, which you can click on for greater detail, shows that Bison Finance Group had HK$93.0m in debt in June 2022; about the same as the year before. However, its balance sheet shows it holds HK$202.6m in cash, so it actually has HK$109.6m net cash.

How Strong Is Bison Finance Group's Balance Sheet?

The latest balance sheet data shows that Bison Finance Group had liabilities of HK$118.3m due within a year, and liabilities of HK$18.8m falling due after that. On the other hand, it had cash of HK$202.6m and HK$42.1m worth of receivables due within a year. So it can boast HK$107.6m more liquid assets than total liabilities.

This luscious liquidity implies that Bison Finance Group's balance sheet is sturdy like a giant sequoia tree. On this view, lenders should feel as safe as the beloved of a black-belt karate master. Succinctly put, Bison Finance Group boasts net cash, so it's fair to say it does not have a heavy debt load! When analysing debt levels, the balance sheet is the obvious place to start. But you can't view debt in total isolation; since Bison Finance Group will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

In the last year Bison Finance Group managed to produce its first revenue as a listed company, but given the lack of profit, shareholders will no doubt be hoping to see some strong increases.

So How Risky Is Bison Finance Group?

By their very nature companies that are losing money are more risky than those with a long history of profitability. And the fact is that over the last twelve months Bison Finance Group lost money at the earnings before interest and tax (EBIT) line. Indeed, in that time it burnt through HK$35m of cash and made a loss of HK$180m. Given it only has net cash of HK$109.6m, the company may need to raise more capital if it doesn't reach break-even soon. Overall, its balance sheet doesn't seem overly risky, at the moment, but we're always cautious until we see the positive free cash flow. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. For example Bison Finance Group has 2 warning signs (and 1 which is potentially serious) we think you should know about.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

Valuation is complex, but we're here to simplify it.

Discover if Bison Finance Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:888

Bison Finance Group

An investment holding company, provides media sales, design services, and production of advertisements for transit vehicle exteriors and interiors, shelters, and outdoor signage advertising business in Hong Kong.

Excellent balance sheet very low.

Market Insights

Advertisement

Community Narratives

Pole position to benefit from GENIUS Act

Fair Value US$233.04|59.7% undervalued

CH

Community Contributor

IREN will transform from bitcoin miner to leader in AI infrastructure

Fair Value US$21.48|13.5% undervalued

KA

Community Contributor

Behind the Assay: XRF Scientific’s Role in Modern Mining Economics

Fair Value AU$2.10|1.4% undervalued

RO

Community Contributor