Advertisement

- Hong Kong

- /

- Entertainment

- /

- SEHK:8368

Creative China Holdings (HKG:8368) Takes On Some Risk With Its Use Of Debt

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. Importantly, Creative China Holdings Limited (HKG:8368) does carry debt. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we think about a company's use of debt, we first look at cash and debt together.

Check out our latest analysis for Creative China Holdings

What Is Creative China Holdings's Net Debt?

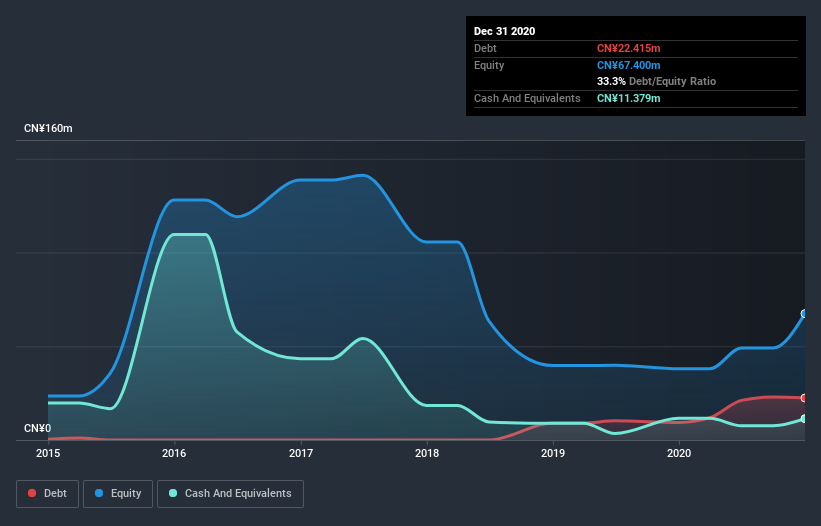

As you can see below, at the end of December 2020, Creative China Holdings had CN¥22.4m of debt, up from CN¥9.36m a year ago. Click the image for more detail. However, it also had CN¥11.4m in cash, and so its net debt is CN¥11.0m.

How Healthy Is Creative China Holdings' Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Creative China Holdings had liabilities of CN¥106.3m due within 12 months and liabilities of CN¥49.4m due beyond that. Offsetting these obligations, it had cash of CN¥11.4m as well as receivables valued at CN¥92.2m due within 12 months. So it has liabilities totalling CN¥52.1m more than its cash and near-term receivables, combined.

This deficit isn't so bad because Creative China Holdings is worth CN¥94.9m, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

While Creative China Holdings's low debt to EBITDA ratio of 0.41 suggests only modest use of debt, the fact that EBIT only covered the interest expense by 4.8 times last year does give us pause. So we'd recommend keeping a close eye on the impact financing costs are having on the business. Notably, Creative China Holdings's EBIT launched higher than Elon Musk, gaining a whopping 8,200% on last year. There's no doubt that we learn most about debt from the balance sheet. But it is Creative China Holdings's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So we always check how much of that EBIT is translated into free cash flow. During the last two years, Creative China Holdings burned a lot of cash. While that may be a result of expenditure for growth, it does make the debt far more risky.

Our View

While Creative China Holdings's conversion of EBIT to free cash flow has us nervous. For example, its EBIT growth rate and net debt to EBITDA give us some confidence in its ability to manage its debt. Looking at all the angles mentioned above, it does seem to us that Creative China Holdings is a somewhat risky investment as a result of its debt. Not all risk is bad, as it can boost share price returns if it pays off, but this debt risk is worth keeping in mind. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. Case in point: We've spotted 2 warning signs for Creative China Holdings you should be aware of.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

When trading Creative China Holdings or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SEHK:8368

Creative China Holdings

An investment holding company, primarily provides film and television program original script creation, adaptation, production and licensing, and related services in the People’s Republic of China, Hong Kong, and Southeast Asia.

Excellent balance sheet low.

Market Insights

Advertisement

Community Narratives

The Most Undervalued of the Magnificent 7

Fair Value US$237.43|36.3% undervalued

IN

Community Contributor

PVA TePla's New Strategy Aims for 22% Revenue Growth in Semiconductor Recovery

Fair Value €19.19|20.8% undervalued

MI

Community Contributor