Advertisement

FriendTimes Inc. (HKG:6820) has announced that it will pay a dividend of HK$0.12 per share on the 8th of June. Based on this payment, the dividend yield on the company's stock will be 9.1%, which is an attractive boost to shareholder returns.

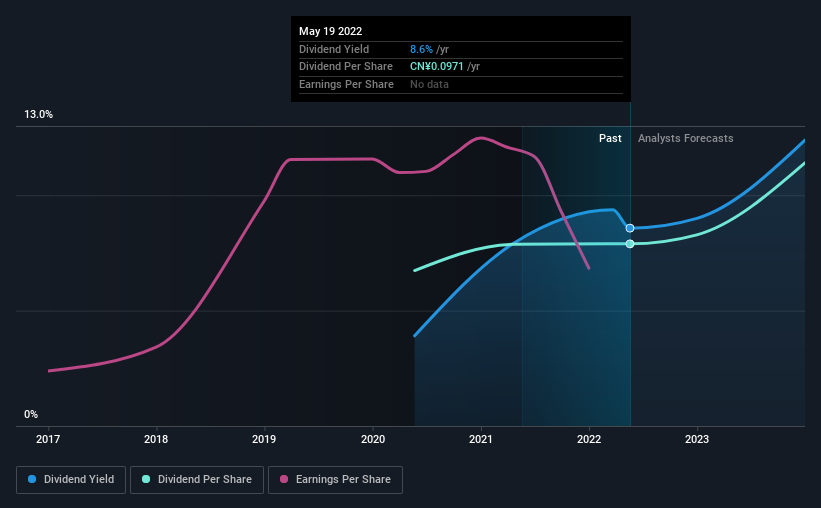

See our latest analysis for FriendTimes

FriendTimes' Dividend Is Well Covered By Earnings

While it is great to have a strong dividend yield, we should also consider whether the payment is sustainable. Prior to this announcement, FriendTimes' dividend was making up a very large proportion of earnings and perhaps more concerning was that it was 109% of cash flows. Paying out such a high proportion of cash flows certainly exposes the company to cutting the dividend if cash flows were to reduce.

Looking forward, earnings per share is forecast to rise by 79.7% over the next year. Assuming the dividend continues along the course it has been charting recently, our estimates show the payout ratio being 53% which brings it into quite a comfortable range.

FriendTimes Doesn't Have A Long Payment History

The dividend has been pretty stable looking back, but the company hasn't been paying one for very long. This makes it tough to judge how it would fare through a full economic cycle. The first annual payment during the last 2 years was CN¥0.083 in 2020, and the most recent fiscal year payment was CN¥0.097. This works out to be a compound annual growth rate (CAGR) of approximately 8.2% a year over that time. FriendTimes has a nice track record of dividend growth but we would wait until we see a longer track record before getting too confident.

FriendTimes' Dividend Might Lack Growth

Some investors will be chomping at the bit to buy some of the company's stock based on its dividend history. FriendTimes has impressed us by growing EPS at 23% per year over the past five years. Earnings per share is growing nicely, but the company is paying out most of its earnings as dividends. This might be sustainable, but we wonder why FriendTimes is not retaining those earnings to reinvest in growth.

FriendTimes' Dividend Doesn't Look Sustainable

In summary, while it's good to see that the dividend hasn't been cut, we are a bit cautious about FriendTimes' payments, as there could be some issues with sustaining them into the future. Strong earnings growth means FriendTimes has the potential to be a good dividend stock in the future, despite the current payments being at elevated levels. We don't think FriendTimes is a great stock to add to your portfolio if income is your focus.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. For example, we've picked out 1 warning sign for FriendTimes that investors should know about before committing capital to this stock. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:6820

FriendTimes

Through its subsidiaries, develops, publishes, distributes, and operates mobile games in the People’s Republic of China and internationally.

Reasonable growth potential with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

Nike's Direct-to-Consumer Focus Will Drive Future Growth

Fair Value US$87.90|22.7% undervalued

UN

Community Contributor

Novo Nordisk will dominate GLP-1 market with Ozempic and Wegovy growth

Fair Value US$89.59|14.2% undervalued

BE

Community Contributor

Rheinmetall could get 20-25% of EU-NATO 3%-GDP defence spending

Fair Value €7.57k|82.8% undervalued

NO

Community Contributor