Advertisement

- Hong Kong

- /

- Metals and Mining

- /

- SEHK:3330

Three Undiscovered Asian Gems With Promising Potential

Simply Wall St

Reviewed by Simply Wall St

As global markets navigate a landscape marked by trade discussions and evolving monetary policies, small- and mid-cap indexes have shown resilience, posting gains for the fifth consecutive week. In this context of cautious optimism, the Asian market presents unique opportunities for investors seeking to uncover stocks with promising potential amidst broader economic shifts. Identifying such gems involves looking at companies that can adapt to changing trade dynamics and leverage regional economic strengths.

Top 10 Undiscovered Gems With Strong Fundamentals In Asia

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Standard Foods | 3.13% | -4.13% | -23.84% | ★★★★★★ |

| Powertip Image | 0.26% | 9.75% | 25.99% | ★★★★★★ |

| Shenzhen Chengtian Weiye Technology | NA | 0.96% | -23.07% | ★★★★★★ |

| Unitech Computer | 24.96% | 2.56% | 1.58% | ★★★★★☆ |

| Pacific Construction | 21.89% | -4.29% | 35.64% | ★★★★★☆ |

| Hong Leong Finance | 0.07% | 6.89% | 6.61% | ★★★★★☆ |

| Lungteh Shipbuilding | 55.17% | 28.09% | 42.33% | ★★★★★☆ |

| Nippon Sharyo | 53.44% | -0.74% | -11.37% | ★★★★☆☆ |

| Kwang Dong Pharmaceutical | 44.94% | 6.47% | 3.58% | ★★★★☆☆ |

| Yuan Cheng CableLtd | 88.11% | 9.84% | 42.67% | ★★★★☆☆ |

Underneath we present a selection of stocks filtered out by our screen.

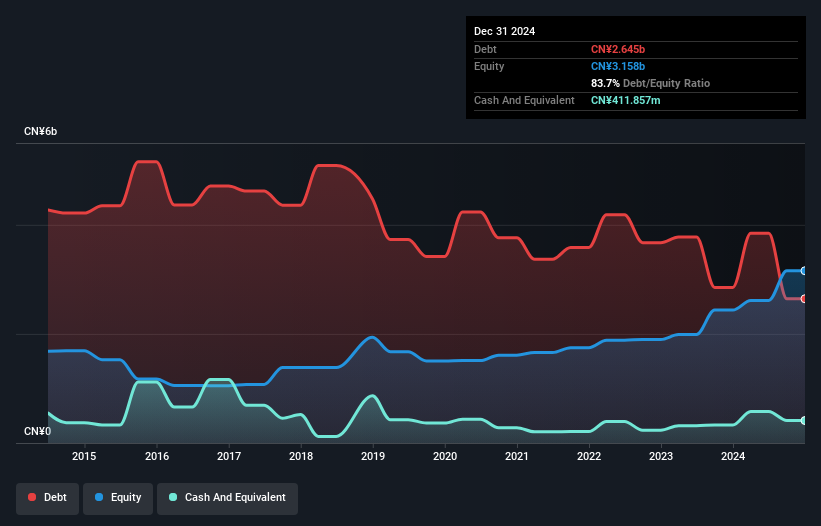

Lingbao Gold Group (SEHK:3330)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Lingbao Gold Group Company Ltd., along with its subsidiaries, focuses on the mining, processing, smelting, refining, and sale of gold products in China and has a market capitalization of approximately HK$12.15 billion.

Operations: The company's primary revenue stream comes from its smelting operations, generating CN¥12.04 billion. Mining activities in the People's Republic of China contribute CN¥2.31 billion, while operations in the Kyrgyz Republic add CN¥257.32 million to revenues. Retailing accounts for a smaller portion at CN¥8.53 million.

Lingbao Gold Group, a smaller player in the metals and mining sector, has shown impressive performance with earnings growth of 119% over the past year, significantly outpacing the industry average of 43%. Despite a high net debt to equity ratio of 70.7%, its interest payments are well covered by EBIT at 9.1 times. The company is trading at a substantial discount, valued at 48.2% below its estimated fair value. Recent developments include a follow-on equity offering raising HKD 234 million and projected net profit exceeding RMB 250 million for Q1 2025 due to increased gold output and market demand.

- Dive into the specifics of Lingbao Gold Group here with our thorough health report.

Explore historical data to track Lingbao Gold Group's performance over time in our Past section.

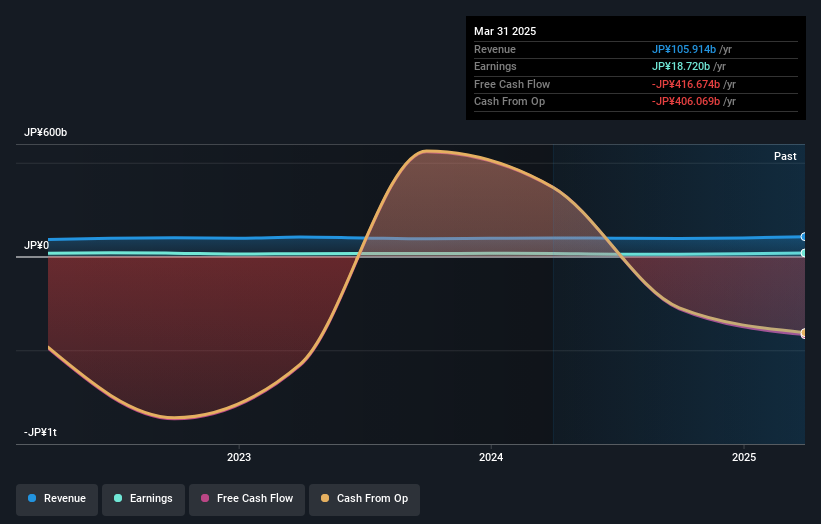

Shiga Bank (TSE:8366)

Simply Wall St Value Rating: ★★★★★☆

Overview: The Shiga Bank, Ltd. offers a range of banking products and services mainly in Japan and has a market capitalization of ¥276.04 billion.

Operations: Shiga Bank's revenue streams are derived from its diverse range of banking products and services offered primarily in Japan. The bank operates with a market capitalization of ¥276.04 billion, focusing on financial growth through its core banking operations.

With total assets of ¥7,528.2 billion and equity at ¥444.8 billion, Shiga Bank stands out with its robust financial foundation. The bank's deposits reach ¥5,828.8 billion against loans totaling ¥4,500.4 billion, but it faces challenges with a 1.8% bad loan ratio and a low allowance for these loans at 42%. Despite earnings growth of 3.8% annually over five years, recent one-off gains of ¥6.8 billion have skewed results somewhat; however, the bank's reliance on customer deposits for 82% of funding adds stability to its operations amidst industry volatility.

- Take a closer look at Shiga Bank's potential here in our health report.

Gain insights into Shiga Bank's past trends and performance with our Past report.

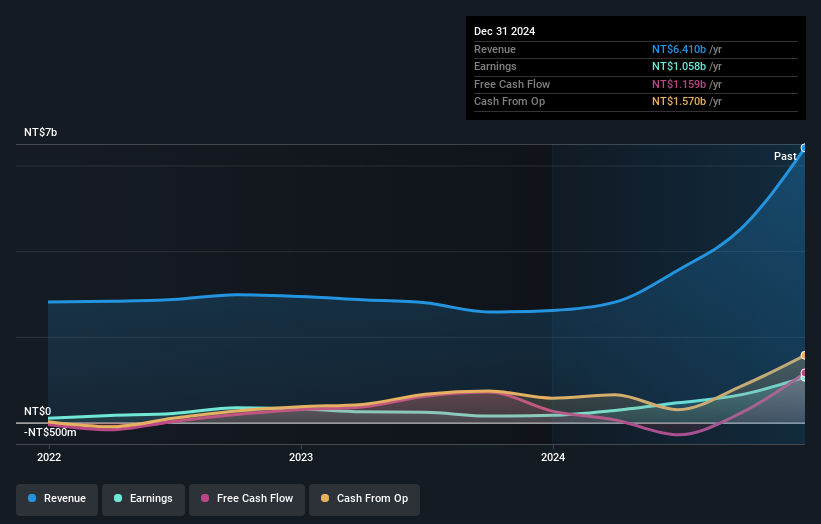

EZconn (TWSE:6442)

Simply Wall St Value Rating: ★★★★★☆

Overview: EZconn Corporation, with a market cap of NT$32.41 billion, manufactures and sells precision metal and optical fiber components for electronic products across Taiwan, Asia, the United States, and Europe.

Operations: EZconn Corporation generates revenue primarily from optical fiber components, contributing NT$5.90 billion, and high-frequency connectors, adding NT$508.67 million.

In the bustling landscape of Asian markets, EZconn stands out with its impressive earnings growth of 529.4% over the past year, surpassing industry norms. The company is trading at a notable 67.7% below its estimated fair value, presenting a potential opportunity for investors seeking undervalued stocks. Despite an increased debt-to-equity ratio from 19.9% to 25.3% over five years, EZconn's financial health remains robust with more cash than total debt and positive free cash flow. Recent board decisions include share repurchases up to TWD 2,088 million and proposed amendments to corporate bylaws, indicating strategic moves towards enhancing shareholder value and operational flexibility.

- Get an in-depth perspective on EZconn's performance by reading our health report here.

Review our historical performance report to gain insights into EZconn's's past performance.

Taking Advantage

- Embark on your investment journey to our 2672 Asian Undiscovered Gems With Strong Fundamentals selection here.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:3330

Lingbao Gold Group

Primarily engages in mining, processing, smelting, refining, and sale of gold products in the People’s Republic of China.

Outstanding track record with high growth potential.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.4% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.0% undervalued

EA

Community Contributor