Advertisement

- Hong Kong

- /

- Basic Materials

- /

- SEHK:1847

Does YCIH Green High-Performance Concrete Company Limited (HKG:1847) Have A Place In Your Dividend Stock Portfolio?

Dividend paying stocks like YCIH Green High-Performance Concrete Company Limited (HKG:1847) tend to be popular with investors, and for good reason - some research suggests a significant amount of all stock market returns come from reinvested dividends. If you are hoping to live on your dividends, it's important to be more stringent with your investments than the average punter. Regular readers know we like to apply the same approach to each dividend stock, and we hope you'll find our analysis useful.

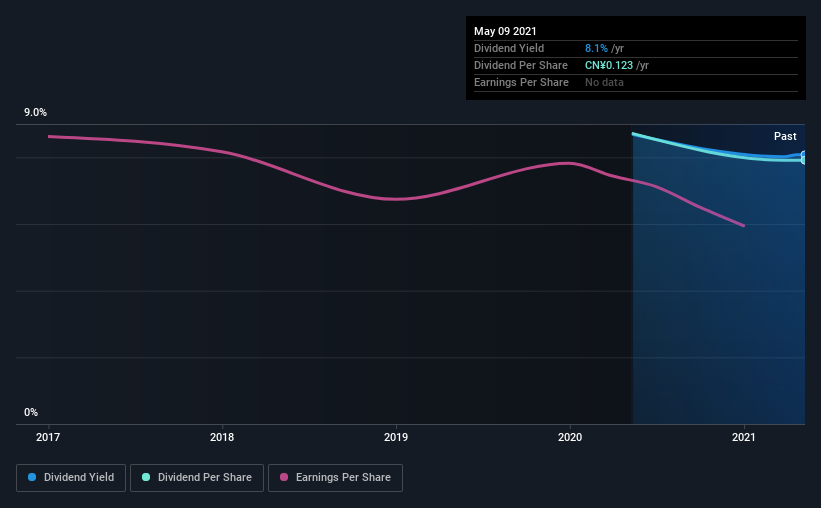

YCIH Green High-Performance Concrete has only been paying a dividend for a year or so, so investors might be curious about its 8.1% yield. There are a few simple ways to reduce the risks of buying YCIH Green High-Performance Concrete for its dividend, and we'll go through these below.

Explore this interactive chart for our latest analysis on YCIH Green High-Performance Concrete!

Payout ratios

Dividends are usually paid out of company earnings. If a company is paying more than it earns, then the dividend might become unsustainable - hardly an ideal situation. Comparing dividend payments to a company's net profit after tax is a simple way of reality-checking whether a dividend is sustainable. Looking at the data, we can see that 27% of YCIH Green High-Performance Concrete's profits were paid out as dividends in the last 12 months. A medium payout ratio strikes a good balance between paying dividends, and keeping enough back to invest in the business. One of the risks is that management reinvests the retained capital poorly instead of paying a higher dividend.

In addition to comparing dividends against profits, we should inspect whether the company generated enough cash to pay its dividend. Last year, YCIH Green High-Performance Concrete paid a dividend while reporting negative free cash flow. While there may be an explanation, we think this behaviour is generally not sustainable.

With a strong net cash balance, YCIH Green High-Performance Concrete investors may not have much to worry about in the near term from a dividend perspective.

We update our data on YCIH Green High-Performance Concrete every 24 hours, so you can always get our latest analysis of its financial health, here.

Dividend Volatility

From the perspective of an income investor who wants to earn dividends for many years, there is not much point buying a stock if its dividend is regularly cut or is not reliable. This company has been paying a dividend for less than 2 years, which we think is too soon to consider it a reliable dividend stock. This works out to be a decline of approximately 9.2% per year over that time.

When a company's per-share dividend falls we question if this reflects poorly on either external business conditions, or the company's capital allocation decisions. Either way, we find it hard to get excited about a company with a declining dividend.

Dividend Growth Potential

Examining whether the dividend is affordable and stable is important. However, it's also important to assess if earnings per share (EPS) are growing. Over the long term, dividends need to grow at or above the rate of inflation, in order to maintain the recipient's purchasing power. It's not great to see that YCIH Green High-Performance Concrete's have fallen at approximately 7.2% over the past five years. Declining earnings per share over a number of years is not a great sign for the dividend investor. Without some improvement, this does not bode well for the long term value of a company's dividend.

We'd also point out that YCIH Green High-Performance Concrete issued a meaningful number of new shares in the past year. Trying to grow the dividend when issuing new shares reminds us of the ancient Greek tale of Sisyphus - perpetually pushing a boulder uphill. Companies that consistently issue new shares are often suboptimal from a dividend perspective.

Conclusion

To summarise, shareholders should always check that YCIH Green High-Performance Concrete's dividends are affordable, that its dividend payments are relatively stable, and that it has decent prospects for growing its earnings and dividend. YCIH Green High-Performance Concrete has a low payout ratio, which we like, although it paid out virtually all of its generated cash. Earnings per share have been falling, and the company has a relatively short dividend history - shorter than we like, anyway. In summary, YCIH Green High-Performance Concrete has a number of shortcomings that we'd find it hard to get past. Things could change, but we think there are likely more attractive alternatives out there.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. For example, we've identified 2 warning signs for YCIH Green High-Performance Concrete (1 is potentially serious!) that you should be aware of before investing.

Looking for more high-yielding dividend ideas? Try our curated list of dividend stocks with a yield above 3%.

If you're looking for stocks to buy, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SEHK:1847

YCIH Green High-Performance Concrete

Operates as a ready-mixed concrete producer in the People's Republic of China.

Mediocre balance sheet with low risk.

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|10.9% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|12.0% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.7% undervalued

TR

Community Contributor