When Brockman Mining Limited (HKG:159) reported its results to June 2022 its auditors, Ernst & Young LLP could not be sure that it would be able to continue as a going concern in the next year. This means that, based on the financial results to that date, the company arguably should raise capital, or otherwise strengthen the balance sheet, as soon as possible.

Since the company probably needs cash fairly quickly, it may be in a position where it has to accept whatever terms it can get. So shareholders should absolutely be taking a close look at how risky the balance sheet is. The biggest concern we would have is the company's debt, since its lenders might force the company into administration if it cannot repay them.

Check out our latest analysis for Brockman Mining

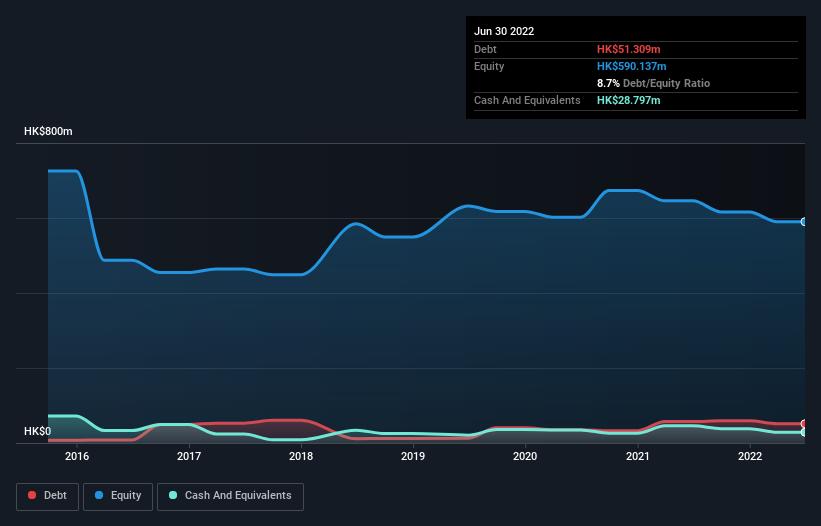

How Much Debt Does Brockman Mining Carry?

As you can see below, Brockman Mining had HK$51.3m of debt at June 2022, down from HK$57.2m a year prior. However, because it has a cash reserve of HK$28.8m, its net debt is less, at about HK$22.5m.

How Strong Is Brockman Mining's Balance Sheet?

According to the last reported balance sheet, Brockman Mining had liabilities of HK$16.3m due within 12 months, and liabilities of HK$158.8m due beyond 12 months. On the other hand, it had cash of HK$28.8m and HK$21.0k worth of receivables due within a year. So its liabilities total HK$146.3m more than the combination of its cash and short-term receivables.

Given Brockman Mining has a market capitalization of HK$1.70b, it's hard to believe these liabilities pose much threat. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward. Carrying virtually no net debt, Brockman Mining has a very light debt load indeed. When analysing debt levels, the balance sheet is the obvious place to start. But it is Brockman Mining's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Since Brockman Mining has no significant operating revenue, shareholders probably hope it will develop a valuable new mine before too long.

Caveat Emptor

Over the last twelve months Brockman Mining produced an earnings before interest and tax (EBIT) loss. Indeed, it lost HK$40m at the EBIT level. When we look at that and recall the liabilities on its balance sheet, relative to cash, it seems unwise to us for the company to have any debt. Quite frankly we think the balance sheet is far from match-fit, although it could be improved with time. Another cause for caution is that is bled HK$20m in negative free cash flow over the last twelve months. So to be blunt we think it is risky. We prefer to avoid a company after its auditor has expressed any uncertainty about its ability to continue as a going concern. That's because we find it more comfortable to invest in companies that always keep the balance sheet reasonably strong. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. Case in point: We've spotted 2 warning signs for Brockman Mining you should be aware of, and 1 of them can't be ignored.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Brockman Mining might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:159

Brockman Mining

An investment holding company, engages in the exploration and development of iron ore mining projects in Australia and Hong Kong.

Low risk with imperfect balance sheet.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

A case for USD $14.81 per share based on book value. Be warned, this is a micro-cap dependent on a single mine.

Occidental Petroleum to Become Fairly Priced at $68.29 According to Future Projections

Agfa-Gevaert is a digital and materials turnaround opportunity, with growth potential in ZIRFON, but carrying legacy risks.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)