Advertisement

- Hong Kong

- /

- Metals and Mining

- /

- SEHK:1258

Are Robust Financials Driving The Recent Rally In China Nonferrous Mining Corporation Limited's (HKG:1258) Stock?

Most readers would already be aware that China Nonferrous Mining's (HKG:1258) stock increased significantly by 18% over the past month. Given the company's impressive performance, we decided to study its financial indicators more closely as a company's financial health over the long-term usually dictates market outcomes. In this article, we decided to focus on China Nonferrous Mining's ROE.

Return on equity or ROE is an important factor to be considered by a shareholder because it tells them how effectively their capital is being reinvested. Put another way, it reveals the company's success at turning shareholder investments into profits.

How Is ROE Calculated?

Return on equity can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for China Nonferrous Mining is:

18% = US$557m ÷ US$3.0b (Based on the trailing twelve months to December 2024).

The 'return' is the profit over the last twelve months. So, this means that for every HK$1 of its shareholder's investments, the company generates a profit of HK$0.18.

Check out our latest analysis for China Nonferrous Mining

What Is The Relationship Between ROE And Earnings Growth?

Thus far, we have learned that ROE measures how efficiently a company is generating its profits. We now need to evaluate how much profit the company reinvests or "retains" for future growth which then gives us an idea about the growth potential of the company. Assuming all else is equal, companies that have both a higher return on equity and higher profit retention are usually the ones that have a higher growth rate when compared to companies that don't have the same features.

A Side By Side comparison of China Nonferrous Mining's Earnings Growth And 18% ROE

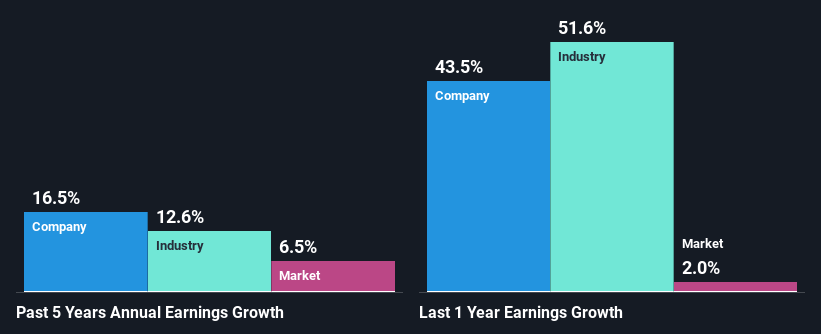

To start with, China Nonferrous Mining's ROE looks acceptable. Further, the company's ROE compares quite favorably to the industry average of 12%. This certainly adds some context to China Nonferrous Mining's decent 17% net income growth seen over the past five years.

Next, on comparing with the industry net income growth, we found that China Nonferrous Mining's growth is quite high when compared to the industry average growth of 13% in the same period, which is great to see.

The basis for attaching value to a company is, to a great extent, tied to its earnings growth. It’s important for an investor to know whether the market has priced in the company's expected earnings growth (or decline). By doing so, they will have an idea if the stock is headed into clear blue waters or if swampy waters await. If you're wondering about China Nonferrous Mining's's valuation, check out this gauge of its price-to-earnings ratio, as compared to its industry.

Is China Nonferrous Mining Efficiently Re-investing Its Profits?

China Nonferrous Mining has a healthy combination of a moderate three-year median payout ratio of 40% (or a retention ratio of 60%) and a respectable amount of growth in earnings as we saw above, meaning that the company has been making efficient use of its profits.

Additionally, China Nonferrous Mining has paid dividends over a period of at least ten years which means that the company is pretty serious about sharing its profits with shareholders.

Summary

On the whole, we feel that China Nonferrous Mining's performance has been quite good. In particular, it's great to see that the company is investing heavily into its business and along with a high rate of return, that has resulted in a sizeable growth in its earnings. Having said that, the company's earnings growth is expected to slow down, as forecasted in the current analyst estimates. To know more about the latest analysts predictions for the company, check out this visualization of analyst forecasts for the company.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1258

China Nonferrous Mining

An investment holding company, engages in the exploration, mining, ore processing, leaching, smelting, and sale of copper cathodes, blister copper, copper anodes.

Flawless balance sheet, undervalued and pays a dividend.

Market Insights

Advertisement

Community Narratives

Rocket Lab USA Will Ignite a 30% Revenue Growth Journey

Fair Value US$31.72|43.6% undervalued

KI

Community Contributor

EasyJet weirdly unloved by investors in spite of relatively attractive metrics

Fair Value UK£6.95|36.4% undervalued

PI

Community Contributor

HEXPOL AB: Sustained Long Term Growth, Stable Margins, and Strategic M&A

Fair Value SEK 122.27|28.4% undervalued

MA

Community Contributor