A Piece Of The Puzzle Missing From The People's Insurance Company (Group) of China Limited's (HKG:1339) 25% Share Price Climb

The People's Insurance Company (Group) of China Limited (HKG:1339) shares have continued their recent momentum with a 25% gain in the last month alone. Looking further back, the 24% rise over the last twelve months isn't too bad notwithstanding the strength over the last 30 days.

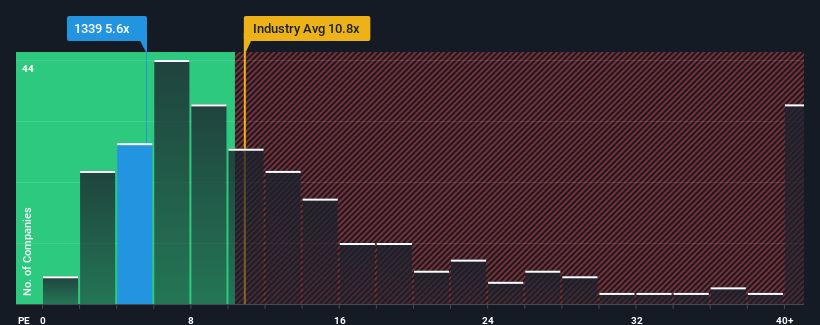

In spite of the firm bounce in price, given about half the companies in Hong Kong have price-to-earnings ratios (or "P/E's") above 10x, you may still consider People's Insurance Company (Group) of China as an attractive investment with its 5.6x P/E ratio. However, the P/E might be low for a reason and it requires further investigation to determine if it's justified.

People's Insurance Company (Group) of China could be doing better as its earnings have been going backwards lately while most other companies have been seeing positive earnings growth. The P/E is probably low because investors think this poor earnings performance isn't going to get any better. If this is the case, then existing shareholders will probably struggle to get excited about the future direction of the share price.

Check out our latest analysis for People's Insurance Company (Group) of China

What Are Growth Metrics Telling Us About The Low P/E?

In order to justify its P/E ratio, People's Insurance Company (Group) of China would need to produce sluggish growth that's trailing the market.

Retrospectively, the last year delivered a frustrating 4.6% decrease to the company's bottom line. Unfortunately, that's brought it right back to where it started three years ago with EPS growth being virtually non-existent overall during that time. So it appears to us that the company has had a mixed result in terms of growing earnings over that time.

Shifting to the future, estimates from the eleven analysts covering the company suggest earnings should grow by 10% per annum over the next three years. With the market predicted to deliver 12% growth each year, the company is positioned for a comparable earnings result.

In light of this, it's peculiar that People's Insurance Company (Group) of China's P/E sits below the majority of other companies. It may be that most investors are not convinced the company can achieve future growth expectations.

The Key Takeaway

Despite People's Insurance Company (Group) of China's shares building up a head of steam, its P/E still lags most other companies. While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

Our examination of People's Insurance Company (Group) of China's analyst forecasts revealed that its market-matching earnings outlook isn't contributing to its P/E as much as we would have predicted. There could be some unobserved threats to earnings preventing the P/E ratio from matching the outlook. At least the risk of a price drop looks to be subdued, but investors seem to think future earnings could see some volatility.

You always need to take note of risks, for example - People's Insurance Company (Group) of China has 1 warning sign we think you should be aware of.

If P/E ratios interest you, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1339

People's Insurance Company (Group) of China

An investment holding company, provides insurance products and services in the People’s Republic of China and Hong Kong.

Undervalued with solid track record and pays a dividend.

Similar Companies

Market Insights

Community Narratives