Advertisement

- Hong Kong

- /

- Personal Products

- /

- SEHK:1962

Evergreen Products Group (HKG:1962) Has A Pretty Healthy Balance Sheet

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We note that Evergreen Products Group Limited (HKG:1962) does have debt on its balance sheet. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first step when considering a company's debt levels is to consider its cash and debt together.

Check out the opportunities and risks within the HK Personal Products industry.

How Much Debt Does Evergreen Products Group Carry?

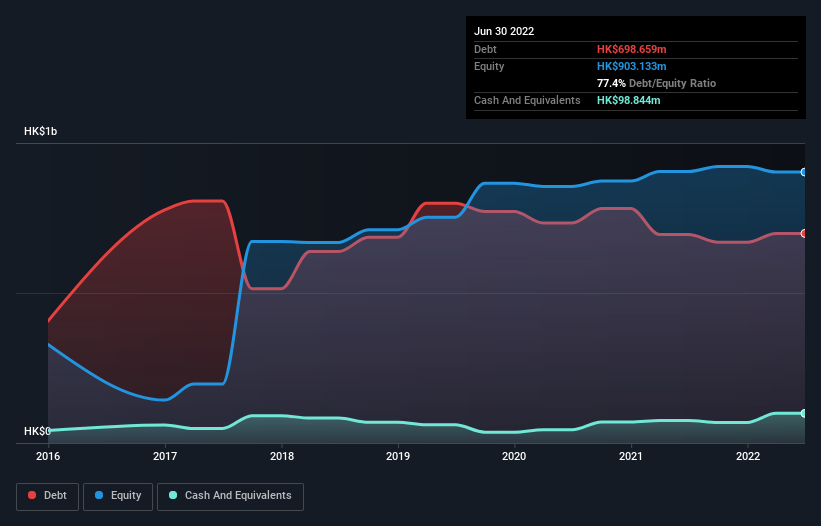

The chart below, which you can click on for greater detail, shows that Evergreen Products Group had HK$698.7m in debt in June 2022; about the same as the year before. However, it does have HK$98.8m in cash offsetting this, leading to net debt of about HK$599.8m.

How Strong Is Evergreen Products Group's Balance Sheet?

According to the last reported balance sheet, Evergreen Products Group had liabilities of HK$768.7m due within 12 months, and liabilities of HK$55.5m due beyond 12 months. Offsetting this, it had HK$98.8m in cash and HK$267.7m in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by HK$457.7m.

Given this deficit is actually higher than the company's market capitalization of HK$446.0m, we think shareholders really should watch Evergreen Products Group's debt levels, like a parent watching their child ride a bike for the first time. Hypothetically, extremely heavy dilution would be required if the company were forced to pay down its liabilities by raising capital at the current share price.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Evergreen Products Group has a rather high debt to EBITDA ratio of 5.3 which suggests a meaningful debt load. However, its interest coverage of 3.5 is reasonably strong, which is a good sign. Looking on the bright side, Evergreen Products Group boosted its EBIT by a silky 99% in the last year. Like a mother's loving embrace of a newborn that sort of growth builds resilience, putting the company in a stronger position to manage its debt. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Evergreen Products Group's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Over the last three years, Evergreen Products Group actually produced more free cash flow than EBIT. That sort of strong cash conversion gets us as excited as the crowd when the beat drops at a Daft Punk concert.

Our View

Both Evergreen Products Group's ability to to convert EBIT to free cash flow and its EBIT growth rate gave us comfort that it can handle its debt. But truth be told its net debt to EBITDA had us nibbling our nails. Looking at all this data makes us feel a little cautious about Evergreen Products Group's debt levels. While debt does have its upside in higher potential returns, we think shareholders should definitely consider how debt levels might make the stock more risky. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. Case in point: We've spotted 5 warning signs for Evergreen Products Group you should be aware of, and 1 of them is a bit unpleasant.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

Valuation is complex, but we're here to simplify it.

Discover if Evergreen Products Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1962

Evergreen Products Group

An investment holding company, engages in the manufacturing and trading of hair products in the United States of America, Germany, Japan, the People’s Republic of China, the United Kingdom, and internationally.

Good value with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

Pole position to benefit from GENIUS Act

Fair Value US$233.04|59.1% undervalued

CH

Community Contributor

IREN will transform from bitcoin miner to leader in AI infrastructure

Fair Value US$21.48|15.5% undervalued

KA

Community Contributor

Behind the Assay: XRF Scientific’s Role in Modern Mining Economics

Fair Value AU$2.10|0% overvalued

RO

Community Contributor