Angelalign Technology (SEHK:6699) shares have retreated roughly 2% after a challenging week, extending a downtrend that has lingered all month. Investors appear to be weighing recent returns against the company’s annual growth metrics.

Despite rallying earlier in the quarter, Angelalign Technology’s momentum has faded in recent weeks as the share price dipped 9.1% over the past month and the 1-year total shareholder return stands at -8.5%. Investors seem to be recalibrating their outlook based on the company’s underlying growth profile and recent shifts in sentiment.

With shares down and growth metrics pointing upward, does Angelalign Technology now offer a rare value play for investors, or is the current price already factoring in all of its future potential?

Advertisement

Price-to-Earnings of 57.4x: Is it justified?

Currently, Angelalign Technology is trading at a price-to-earnings (P/E) ratio of 57.4x, which is well above both its industry peers and its own estimated fair value.

The P/E ratio is a widely used valuation metric that compares a company’s current share price to its per-share earnings. For healthcare technology companies like Angelalign, high P/E ratios can sometimes be justified if investors expect strong future growth or margin improvements. However, the premium should still align with sector realities.

Angelalign’s P/E of 57.4x is significantly higher than the Hong Kong Medical Equipment industry average of 21.1x and its peer average of 50.1x. It is also far above the estimated fair P/E of 19.6x, revealing a strong disconnect between current market expectations and fundamental value. This level suggests buyers may be pricing in robust future performance, but the valuation gap poses a risk if growth slows or expectations change.

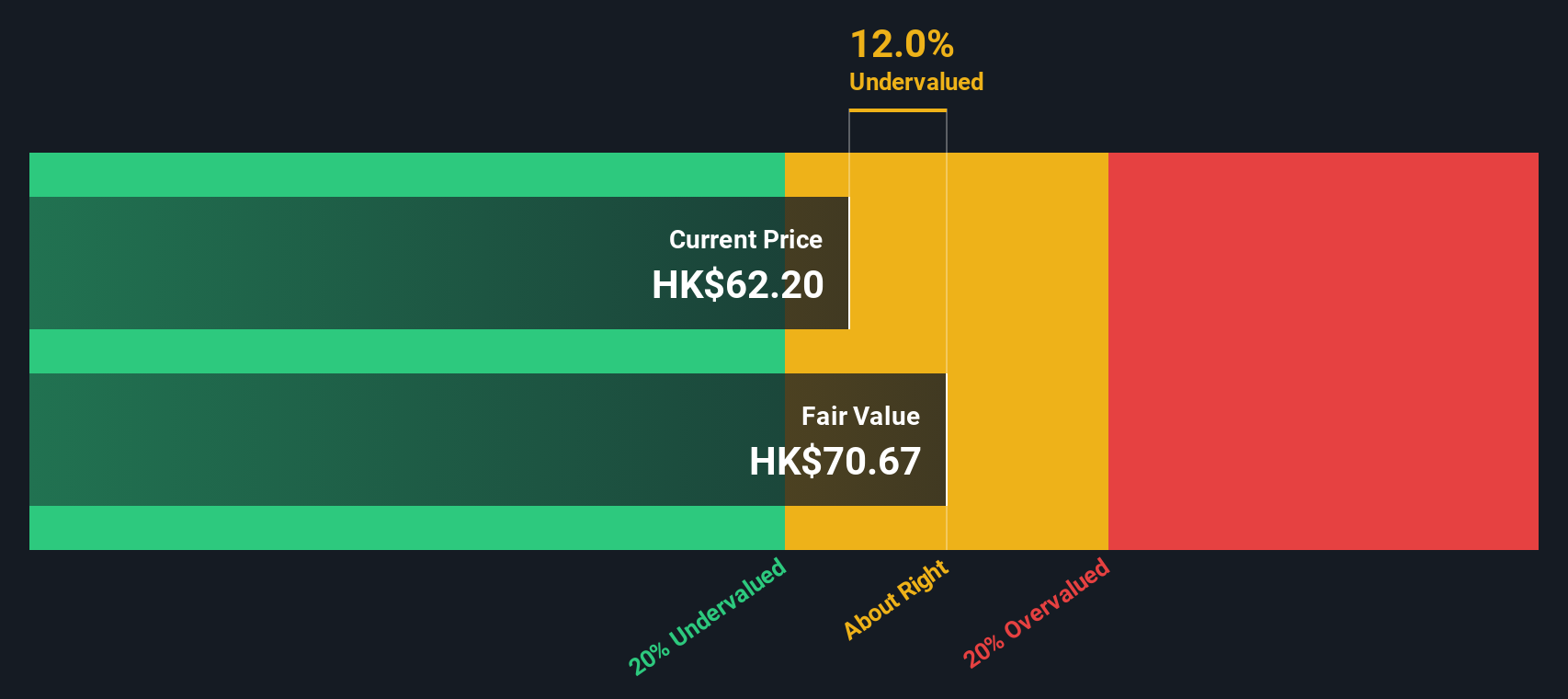

Looking at Angelalign Technology through the lens of our DCF model, the picture shifts. While the current share price appears expensive relative to earnings, the SWS DCF model suggests the stock is trading about 12.7% below its estimated fair value. Could the market be undervaluing future cash flow potential, or are the risks reflected in the valuation for a reason?

If you have a different perspective or enjoy digging into the numbers yourself, you can build your own data-driven narrative in just a few minutes, and Do it your way.

A good starting point is our analysis highlighting 4 key rewards investors are optimistic about regarding Angelalign Technology.

Looking for More Investment Ideas?

Seize the chance to take your portfolio further. These hand-picked screeners could reveal overlooked gems, sector leaders, or future trends you do not want to miss out on.

Catch the wave of artificial intelligence innovation by targeting these 24 AI penny stocks, set to reshape industries and create lasting value.

Position yourself at the frontier of computing by exploring these 26 quantum computing stocks, featuring companies pushing the boundaries of what technology can do.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency • Be alerted to new Warning Signs or Risks via email or mobile • Track the Fair Value of your stocks

An investment holding company, researches and designs, manufactures, sells, and markets clear aligner treatment solutions in the People’s Republic of China and internationally.