Advertisement

- Hong Kong

- /

- Healthcare Services

- /

- SEHK:6639

SEHK Growth Companies With High Insider Ownership Showcasing Promising Futures

Simply Wall St

Reviewed by Simply Wall St

Amidst a landscape of fluctuating global markets, the Hong Kong stock market continues to present unique opportunities for discerning investors. This article explores three growth-oriented companies in the SEHK with high insider ownership, a trait often associated with strong confidence in a company's future prospects and alignment of interests between shareholders and management.

Top 10 Growth Companies With High Insider Ownership In Hong Kong

| Name | Insider Ownership | Earnings Growth |

| iDreamSky Technology Holdings (SEHK:1119) | 20.1% | 104.1% |

| Fenbi (SEHK:2469) | 32.4% | 43% |

| Joy Spreader Group (SEHK:6988) | 36.5% | 107.6% |

| DPC Dash (SEHK:1405) | 38.2% | 89.7% |

| Zylox-Tonbridge Medical Technology (SEHK:2190) | 18.5% | 79.3% |

| Adicon Holdings (SEHK:9860) | 22.3% | 29.6% |

| Tian Tu Capital (SEHK:1973) | 34% | 70.5% |

| Biocytogen Pharmaceuticals (Beijing) (SEHK:2315) | 13.9% | 100.1% |

| Zhejiang Leapmotor Technology (SEHK:9863) | 15% | 76.5% |

| Beijing Airdoc Technology (SEHK:2251) | 28.2% | 83.9% |

Here's a peek at a few of the choices from the screener.

Biocytogen Pharmaceuticals (Beijing) (SEHK:2315)

Simply Wall St Growth Rating: ★★★★★☆

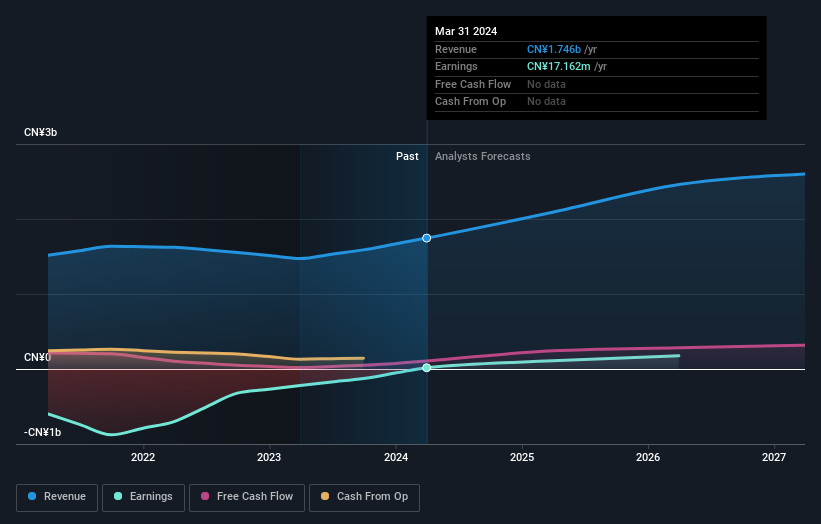

Overview: Biocytogen Pharmaceuticals (Beijing) Co., Ltd. is a biotechnology firm focused on the research and development of antibody-based drugs, operating in the People’s Republic of China, the United States, and internationally, with a market capitalization of approximately HK$2.99 billion.

Operations: Biocytogen Pharmaceuticals generates revenue primarily through Animal Models Selling (CN¥293.68 million), Pre-Clinical Pharmacology and Efficacy Evaluation (CN¥193.40 million), Antibody Development (CN¥175.87 million), and Gene Editing (CN¥74.33 million).

Insider Ownership: 13.9%

Earnings Growth Forecast: 100.1% p.a.

Biocytogen Pharmaceuticals (Beijing) demonstrates potential as a growth company with high insider ownership, despite its challenges. Recently, the firm announced collaborations with BioCopy AG and ABL Bio Inc., leveraging its proprietary platforms to develop novel cancer therapies and antibody-drug conjugates. Although it reported a significant reduction in net loss from CNY 601.95 million to CNY 382.95 million year-over-year, the company still operates at a loss. However, revenue growth is robust at 34.3% over the past year, outpacing industry averages significantly, with expectations of continued expansion and profitability within three years.

- Click here to discover the nuances of Biocytogen Pharmaceuticals (Beijing) with our detailed analytical future growth report.

- Insights from our recent valuation report point to the potential undervaluation of Biocytogen Pharmaceuticals (Beijing) shares in the market.

Beauty Farm Medical and Health Industry (SEHK:2373)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Beauty Farm Medical and Health Industry Inc. operates in the healthcare sector and has a market capitalization of approximately HK$3.77 billion.

Operations: Beauty Farm Medical and Health Industry Inc. generates revenue primarily from three segments: Aesthetic Medical Services (CN¥850.36 million), Subhealth Medical Services (CN¥101.04 million), and Beauty and Wellness Services through both direct stores and franchisees (CN¥1.19 billion).

Insider Ownership: 33.9%

Earnings Growth Forecast: 22.9% p.a.

Beauty Farm Medical and Health Industry Inc. in Hong Kong highlights promising growth with high insider ownership. The company's recent dividend increase to HK$110.8 million underscores strong financial health, complemented by a robust year-over-year earnings growth from CNY 1,635.41 million to CNY 2,145.07 million and net income doubling to CNY 215.66 million. Forecasts suggest an annual profit growth of 22.9% and revenue expansion at 18.6%, both outpacing the local market significantly, while trading at a substantial discount to its estimated fair value.

- Unlock comprehensive insights into our analysis of Beauty Farm Medical and Health Industry stock in this growth report.

- Our valuation report unveils the possibility Beauty Farm Medical and Health Industry's shares may be trading at a premium.

Arrail Group (SEHK:6639)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Arrail Group Limited, a company that operates dental hospitals and clinics in China, has a market capitalization of approximately HK$2.51 billion.

Operations: The company generates its revenue primarily through two segments: Arrail Dental, which contributed CN¥0.73 billion, and Rytime Dental, with CN¥0.86 billion in revenues.

Insider Ownership: 14.7%

Earnings Growth Forecast: 109.7% p.a.

Arrail Group, despite trading at 72.8% below its estimated fair value, presents challenges with insider activities and modest growth forecasts in Hong Kong. While there has been significant insider selling recently, the company is expected to turn profitable within three years. Its revenue growth forecast of 12% per year outpaces the local market's 7.8%, but remains below more aggressive growth benchmarks. Analysts anticipate a potential price increase of 67.4%, reflecting optimism about its future profitability and earnings expansion projected at 109.7% annually.

- Delve into the full analysis future growth report here for a deeper understanding of Arrail Group.

- According our valuation report, there's an indication that Arrail Group's share price might be on the cheaper side.

Key Takeaways

- Reveal the 51 hidden gems among our Fast Growing SEHK Companies With High Insider Ownership screener with a single click here.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:6639

Excellent balance sheet and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

Apple: A Dying Star with an Overpriced Valuation

Fair Value US$177.34|19.2% overvalued

IN

Community Contributor

Avino a case for USD$20 per share within 5 years (assuming $3,500 gold, $100 silver and $4 copper).

Fair Value CA$26.79|86.0% undervalued

AG

Community Contributor

Riding the Defense Boom RENK Sees Revenue Climb at 15% CAGR by FY 2029

Fair Value €69.87|20.5% undervalued

CH

Community Contributor