Advertisement

- Hong Kong

- /

- Healthcare Services

- /

- SEHK:383

Is China Medical & HealthCare Group (HKG:383) A Risky Investment?

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies China Medical & HealthCare Group Limited (HKG:383) makes use of debt. But the more important question is: how much risk is that debt creating?

When Is Debt A Problem?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

View our latest analysis for China Medical & HealthCare Group

What Is China Medical & HealthCare Group's Net Debt?

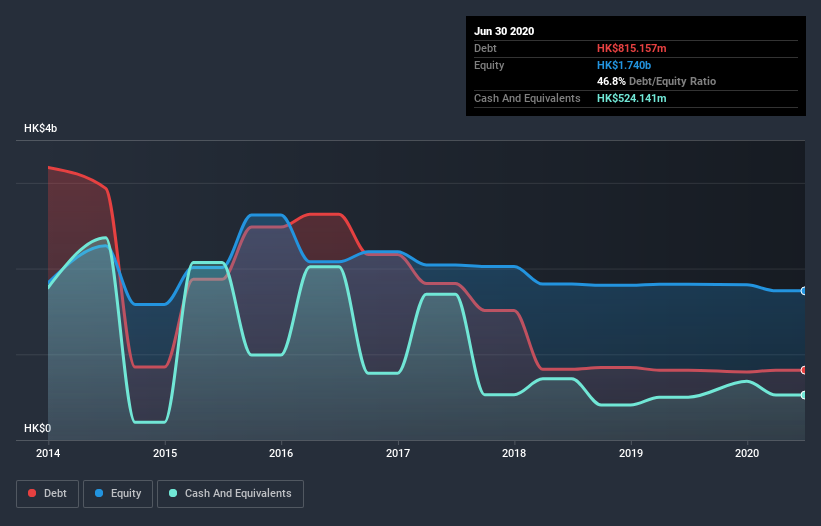

The chart below, which you can click on for greater detail, shows that China Medical & HealthCare Group had HK$815.2m in debt in June 2020; about the same as the year before. However, it does have HK$524.1m in cash offsetting this, leading to net debt of about HK$291.0m.

How Healthy Is China Medical & HealthCare Group's Balance Sheet?

We can see from the most recent balance sheet that China Medical & HealthCare Group had liabilities of HK$1.03b falling due within a year, and liabilities of HK$359.1m due beyond that. Offsetting this, it had HK$524.1m in cash and HK$87.2m in receivables that were due within 12 months. So it has liabilities totalling HK$780.7m more than its cash and near-term receivables, combined.

While this might seem like a lot, it is not so bad since China Medical & HealthCare Group has a market capitalization of HK$1.81b, and so it could probably strengthen its balance sheet by raising capital if it needed to. However, it is still worthwhile taking a close look at its ability to pay off debt. There's no doubt that we learn most about debt from the balance sheet. But you can't view debt in total isolation; since China Medical & HealthCare Group will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Over 12 months, China Medical & HealthCare Group made a loss at the EBIT level, and saw its revenue drop to HK$1.1b, which is a fall of 8.1%. That's not what we would hope to see.

Caveat Emptor

Importantly, China Medical & HealthCare Group had an earnings before interest and tax (EBIT) loss over the last year. Indeed, it lost HK$31m at the EBIT level. When we look at that and recall the liabilities on its balance sheet, relative to cash, it seems unwise to us for the company to have any debt. Quite frankly we think the balance sheet is far from match-fit, although it could be improved with time. However, it doesn't help that it burned through HK$109m of cash over the last year. So in short it's a really risky stock. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. Consider for instance, the ever-present spectre of investment risk. We've identified 1 warning sign with China Medical & HealthCare Group , and understanding them should be part of your investment process.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

When trading China Medical & HealthCare Group or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Tian An Medicare might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About SEHK:383

Tian An Medicare

An investment holding company, primarily operates hospitals in the People’s Republic of China and Hong Kong.

Excellent balance sheet with proven track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

Enterprise, AI & Cloud Growth Ahead, Waiting For the Right Price 💸

Fair Value US$204.74|6.7% overvalued

FR

Community Contributor

Good foundation, but now it's all about the next steps

Fair Value US$147.87|23.9% undervalued

TO

Community Contributor

XTB's Path to 100–120 PLN by 2028 Amid Market Volatility

Fair Value zł100.96|33.3% undervalued

DZ

Community Contributor