Advertisement

- Hong Kong

- /

- Medical Equipment

- /

- SEHK:2190

Why Investors Shouldn't Be Surprised By Zylox-Tonbridge Medical Technology Co., Ltd.'s (HKG:2190) 37% Share Price Surge

Despite an already strong run, Zylox-Tonbridge Medical Technology Co., Ltd. (HKG:2190) shares have been powering on, with a gain of 37% in the last thirty days. The last 30 days bring the annual gain to a very sharp 91%.

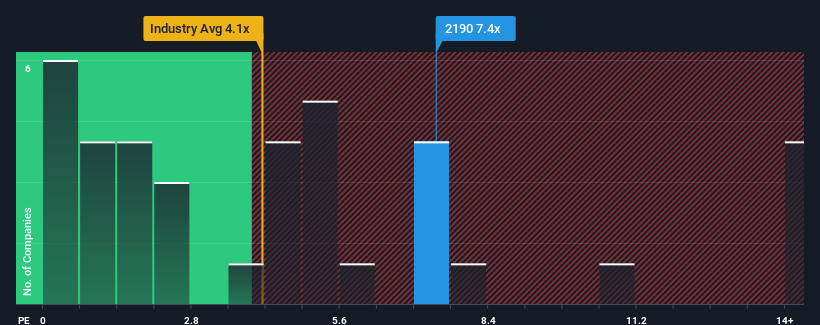

Since its price has surged higher, Zylox-Tonbridge Medical Technology may be sending very bearish signals at the moment with a price-to-sales (or "P/S") ratio of 7.4x, since almost half of all companies in the Medical Equipment industry in Hong Kong have P/S ratios under 4.1x and even P/S lower than 1.2x are not unusual. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's so lofty.

View our latest analysis for Zylox-Tonbridge Medical Technology

How Has Zylox-Tonbridge Medical Technology Performed Recently?

Zylox-Tonbridge Medical Technology certainly has been doing a good job lately as it's been growing revenue more than most other companies. It seems that many are expecting the strong revenue performance to persist, which has raised the P/S. If not, then existing shareholders might be a little nervous about the viability of the share price.

Keen to find out how analysts think Zylox-Tonbridge Medical Technology's future stacks up against the industry? In that case, our free report is a great place to start.Do Revenue Forecasts Match The High P/S Ratio?

The only time you'd be truly comfortable seeing a P/S as steep as Zylox-Tonbridge Medical Technology's is when the company's growth is on track to outshine the industry decidedly.

Retrospectively, the last year delivered an exceptional 48% gain to the company's top line. Spectacularly, three year revenue growth has ballooned by several orders of magnitude, thanks in part to the last 12 months of revenue growth. So we can start by confirming that the company has done a tremendous job of growing revenue over that time.

Shifting to the future, estimates from the four analysts covering the company suggest revenue should grow by 34% per year over the next three years. With the industry only predicted to deliver 30% per annum, the company is positioned for a stronger revenue result.

With this in mind, it's not hard to understand why Zylox-Tonbridge Medical Technology's P/S is high relative to its industry peers. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

What We Can Learn From Zylox-Tonbridge Medical Technology's P/S?

Shares in Zylox-Tonbridge Medical Technology have seen a strong upwards swing lately, which has really helped boost its P/S figure. While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

As we suspected, our examination of Zylox-Tonbridge Medical Technology's analyst forecasts revealed that its superior revenue outlook is contributing to its high P/S. Right now shareholders are comfortable with the P/S as they are quite confident future revenues aren't under threat. Unless these conditions change, they will continue to provide strong support to the share price.

Many other vital risk factors can be found on the company's balance sheet. You can assess many of the main risks through our free balance sheet analysis for Zylox-Tonbridge Medical Technology with six simple checks.

If you're unsure about the strength of Zylox-Tonbridge Medical Technology's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Valuation is complex, but we're here to simplify it.

Discover if Zylox-Tonbridge Medical Technology might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:2190

Zylox-Tonbridge Medical Technology

A medical device company, provides neuro- and peripheral-vascular interventional medical devices in the People’s Republic of China and internationally.

Flawless balance sheet with high growth potential.

Market Insights

Advertisement

Community Narratives

Apple: A Dying Star with an Overpriced Valuation

Fair Value US$177.34|19.1% overvalued

IN

Community Contributor

Avino a case for USD$20 per share within 5 years (assuming $3,500 gold, $100 silver and $4 copper).

Fair Value CA$26.79|86.0% undervalued

AG

Community Contributor

Riding the Defense Boom RENK Sees Revenue Climb at 15% CAGR by FY 2029

Fair Value €69.87|14.3% undervalued

CH

Community Contributor