- Hong Kong

- /

- Healthcare Services

- /

- SEHK:1515

Analyst Forecasts For China Resources Medical Holdings Company Limited (HKG:1515) Are Surging Higher

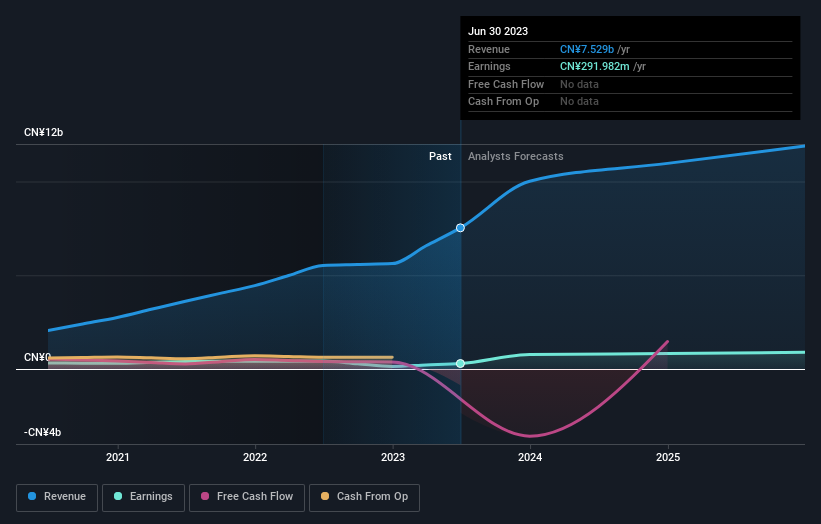

China Resources Medical Holdings Company Limited (HKG:1515) shareholders will have a reason to smile today, with the analysts making substantial upgrades to this year's statutory forecasts. Consensus estimates suggest investors could expect greatly increased statutory revenues and earnings per share, with analysts modelling a real improvement in business performance.

Following the upgrade, the latest consensus from China Resources Medical Holdings' six analysts is for revenues of CN¥10b in 2023, which would reflect a substantial 33% improvement in sales compared to the last 12 months. Statutory earnings per share are presumed to shoot up 170% to CN¥0.61. Before this latest update, the analysts had been forecasting revenues of CN¥8.1b and earnings per share (EPS) of CN¥0.50 in 2023. So we can see there's been a pretty clear increase in analyst sentiment in recent times, with both revenues and earnings per share receiving a decent lift in the latest estimates.

See our latest analysis for China Resources Medical Holdings

Despite these upgrades, the analysts have not made any major changes to their price target of CN¥8.12, suggesting that the higher estimates are not likely to have a long term impact on what the stock is worth. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. Currently, the most bullish analyst values China Resources Medical Holdings at CN¥11.98 per share, while the most bearish prices it at CN¥5.48. This is a fairly broad spread of estimates, suggesting that the analysts are forecasting a wide range of possible outcomes for the business.

Of course, another way to look at these forecasts is to place them into context against the industry itself. The analysts are definitely expecting China Resources Medical Holdings' growth to accelerate, with the forecast 77% annualised growth to the end of 2023 ranking favourably alongside historical growth of 30% per annum over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to grow their revenue at 15% per year. It seems obvious that, while the growth outlook is brighter than the recent past, the analysts also expect China Resources Medical Holdings to grow faster than the wider industry.

The Bottom Line

The biggest takeaway for us from these new estimates is that analysts upgraded their earnings per share estimates, with improved earnings power expected for this year. Fortunately, analysts also upgraded their revenue estimates, and our data indicates sales are expected to perform better than the wider market. The lack of change in the price target is puzzling, but with a serious upgrade to this year's earnings expectations, it might be time to take another look at China Resources Medical Holdings.

Even so, the longer term trajectory of the business is much more important for the value creation of shareholders. At Simply Wall St, we have a full range of analyst estimates for China Resources Medical Holdings going out to 2025, and you can see them free on our platform here..

Of course, seeing company management invest large sums of money in a stock can be just as useful as knowing whether analysts are upgrading their estimates. So you may also wish to search this free list of stocks that insiders are buying.

If you're looking to trade China Resources Medical Holdings, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1515

China Resources Medical Holdings

An investment holding company, provides general healthcare, hospital management, and other hospital-related services in the People’s Republic of China.

Undervalued with solid track record and pays a dividend.

Market Insights

Community Narratives