Advertisement

- Hong Kong

- /

- Healthcare Services

- /

- SEHK:1406

Here's Why We're Watching Clarity Medical Group Holding's (HKG:1406) Cash Burn Situation

Just because a business does not make any money, does not mean that the stock will go down. For example, biotech and mining exploration companies often lose money for years before finding success with a new treatment or mineral discovery. But while the successes are well known, investors should not ignore the very many unprofitable companies that simply burn through all their cash and collapse.

Given this risk, we thought we'd take a look at whether Clarity Medical Group Holding (HKG:1406) shareholders should be worried about its cash burn. For the purposes of this article, cash burn is the annual rate at which an unprofitable company spends cash to fund its growth; its negative free cash flow. The first step is to compare its cash burn with its cash reserves, to give us its 'cash runway'.

See our latest analysis for Clarity Medical Group Holding

When Might Clarity Medical Group Holding Run Out Of Money?

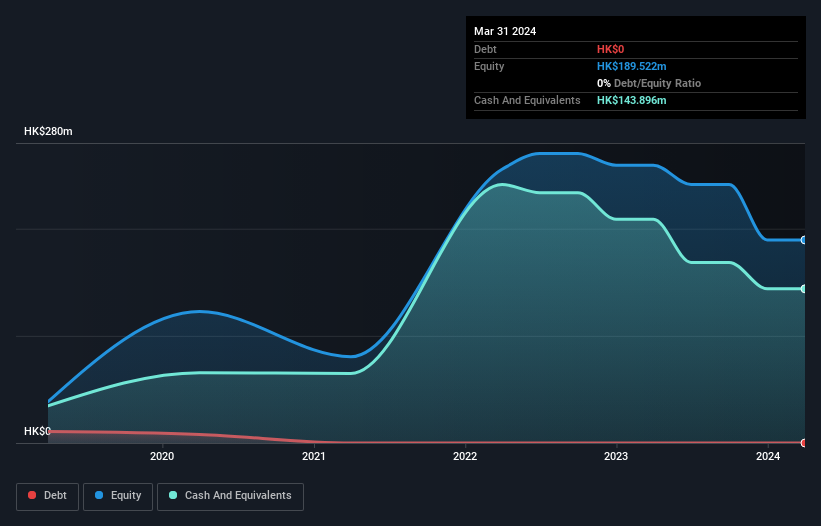

A company's cash runway is calculated by dividing its cash hoard by its cash burn. In March 2024, Clarity Medical Group Holding had HK$144m in cash, and was debt-free. Looking at the last year, the company burnt through HK$48m. That means it had a cash runway of about 3.0 years as of March 2024. That's decent, giving the company a couple years to develop its business. You can see how its cash balance has changed over time in the image below.

How Well Is Clarity Medical Group Holding Growing?

It was quite stunning to see that Clarity Medical Group Holding increased its cash burn by 246% over the last year. While that's concerning on it's own, the fact that operating revenue was actually down 11% over the same period makes us positively tremulous. Considering these two factors together makes us nervous about the direction the company seems to be heading. In reality, this article only makes a short study of the company's growth data. This graph of historic earnings and revenue shows how Clarity Medical Group Holding is building its business over time.

How Hard Would It Be For Clarity Medical Group Holding To Raise More Cash For Growth?

Even though it seems like Clarity Medical Group Holding is developing its business nicely, we still like to consider how easily it could raise more money to accelerate growth. Issuing new shares, or taking on debt, are the most common ways for a listed company to raise more money for its business. Many companies end up issuing new shares to fund future growth. By comparing a company's annual cash burn to its total market capitalisation, we can estimate roughly how many shares it would have to issue in order to run the company for another year (at the same burn rate).

Clarity Medical Group Holding has a market capitalisation of HK$209m and burnt through HK$48m last year, which is 23% of the company's market value. That's fairly notable cash burn, so if the company had to sell shares to cover the cost of another year's operations, shareholders would suffer some costly dilution.

Is Clarity Medical Group Holding's Cash Burn A Worry?

On this analysis of Clarity Medical Group Holding's cash burn, we think its cash runway was reassuring, while its increasing cash burn has us a bit worried. We don't think its cash burn is particularly problematic, but after considering the range of factors in this article, we do think shareholders should be monitoring how it changes over time. Separately, we looked at different risks affecting the company and spotted 2 warning signs for Clarity Medical Group Holding (of which 1 is significant!) you should know about.

Of course, you might find a fantastic investment by looking elsewhere. So take a peek at this free list of companies with significant insider holdings, and this list of stocks growth stocks (according to analyst forecasts)

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1406

Clarity Medical Group Holding

An investment holding company, provides ophthalmic healthcare services in Hong Kong.

Flawless balance sheet very low.

Similar Companies

Market Insights

Advertisement

Community Narratives

Nike's Direct-to-Consumer Focus Will Drive Future Growth

Fair Value US$87.90|18.2% undervalued

UN

Community Contributor

Novo Nordisk will dominate GLP-1 market with Ozempic and Wegovy growth

Fair Value US$89.59|12.1% undervalued

BE

Community Contributor

Rheinmetall could get 20-25% of EU-NATO 3%-GDP defence spending

Fair Value €7.57k|82.4% undervalued

NO

Community Contributor