Nissin Foods Company Limited's (HKG:1475) Stock On An Uptrend: Could Fundamentals Be Driving The Momentum?

Nissin Foods' (HKG:1475) stock is up by a considerable 13% over the past three months. We wonder if and what role the company's financials play in that price change as a company's long-term fundamentals usually dictate market outcomes. In this article, we decided to focus on Nissin Foods' ROE.

ROE or return on equity is a useful tool to assess how effectively a company can generate returns on the investment it received from its shareholders. Put another way, it reveals the company's success at turning shareholder investments into profits.

Check out our latest analysis for Nissin Foods

How To Calculate Return On Equity?

ROE can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Nissin Foods is:

9.1% = HK$332m ÷ HK$3.7b (Based on the trailing twelve months to June 2024).

The 'return' is the yearly profit. That means that for every HK$1 worth of shareholders' equity, the company generated HK$0.09 in profit.

What Is The Relationship Between ROE And Earnings Growth?

We have already established that ROE serves as an efficient profit-generating gauge for a company's future earnings. We now need to evaluate how much profit the company reinvests or "retains" for future growth which then gives us an idea about the growth potential of the company. Generally speaking, other things being equal, firms with a high return on equity and profit retention, have a higher growth rate than firms that don’t share these attributes.

Nissin Foods' Earnings Growth And 9.1% ROE

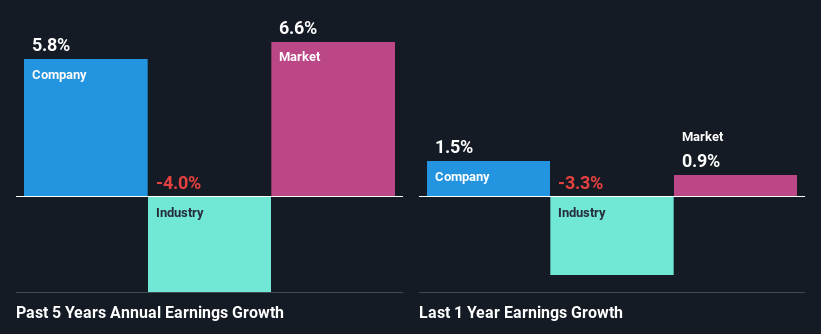

On the face of it, Nissin Foods' ROE is not much to talk about. Although a closer study shows that the company's ROE is higher than the industry average of 6.0% which we definitely can't overlook. This certainly adds some context to Nissin Foods' moderate 5.8% net income growth seen over the past five years. That being said, the company does have a slightly low ROE to begin with, just that it is higher than the industry average. So there might well be other reasons for the earnings to grow. Such as- high earnings retention or the company belonging to a high growth industry.

Next, on comparing with the industry net income growth, we found that the growth figure reported by Nissin Foods compares quite favourably to the industry average, which shows a decline of 4.0% over the last few years.

Earnings growth is an important metric to consider when valuing a stock. It’s important for an investor to know whether the market has priced in the company's expected earnings growth (or decline). This then helps them determine if the stock is placed for a bright or bleak future. What is 1475 worth today? The intrinsic value infographic in our free research report helps visualize whether 1475 is currently mispriced by the market.

Is Nissin Foods Making Efficient Use Of Its Profits?

Nissin Foods has a significant three-year median payout ratio of 51%, meaning that it is left with only 49% to reinvest into its business. This implies that the company has been able to achieve decent earnings growth despite returning most of its profits to shareholders.

Moreover, Nissin Foods is determined to keep sharing its profits with shareholders which we infer from its long history of seven years of paying a dividend. Upon studying the latest analysts' consensus data, we found that the company is expected to keep paying out approximately 50% of its profits over the next three years. Therefore, the company's future ROE is also not expected to change by much with analysts predicting an ROE of 9.7%.

Conclusion

On the whole, we do feel that Nissin Foods has some positive attributes. Specifically, its respectable ROE which likely led to the considerable growth in earnings. Yet, the company is retaining a small portion of its profits. Which means that the company has been able to grow its earnings in spite of it, so that's not too bad. Having said that, looking at the current analyst estimates, we found that the company's earnings are expected to gain momentum. To know more about the company's future earnings growth forecasts take a look at this free report on analyst forecasts for the company to find out more.

Valuation is complex, but we're here to simplify it.

Discover if Nissin Foods might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1475

Nissin Foods

Manufactures and sells instant noodles in Hong Kong, Mainland China, Canada, Australia, the United States, Taiwan, Macau, and internationally.

Flawless balance sheet with proven track record.