Advertisement

- Hong Kong

- /

- Energy Services

- /

- SEHK:3337

Investors Still Aren't Entirely Convinced By Anton Oilfield Services Group's (HKG:3337) Earnings Despite 30% Price Jump

Anton Oilfield Services Group (HKG:3337) shares have continued their recent momentum with a 30% gain in the last month alone. The last month tops off a massive increase of 179% in the last year.

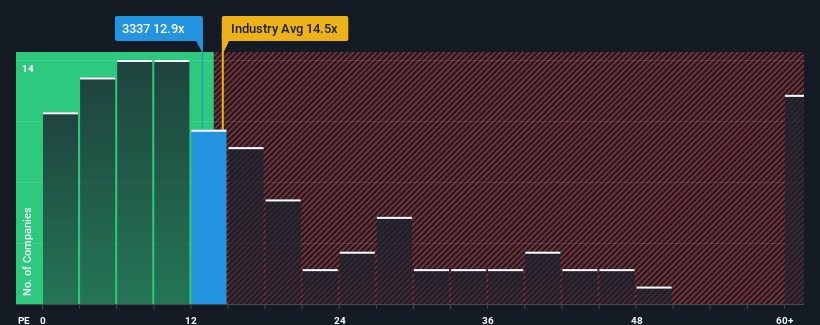

Even after such a large jump in price, it's still not a stretch to say that Anton Oilfield Services Group's price-to-earnings (or "P/E") ratio of 12.8x right now seems quite "middle-of-the-road" compared to the market in Hong Kong, where the median P/E ratio is around 11x. Although, it's not wise to simply ignore the P/E without explanation as investors may be disregarding a distinct opportunity or a costly mistake.

With earnings growth that's superior to most other companies of late, Anton Oilfield Services Group has been doing relatively well. One possibility is that the P/E is moderate because investors think this strong earnings performance might be about to tail off. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's not quite in favour.

Check out our latest analysis for Anton Oilfield Services Group

How Is Anton Oilfield Services Group's Growth Trending?

In order to justify its P/E ratio, Anton Oilfield Services Group would need to produce growth that's similar to the market.

If we review the last year of earnings growth, the company posted a terrific increase of 27%. The latest three year period has also seen an excellent 230% overall rise in EPS, aided by its short-term performance. Accordingly, shareholders would have probably welcomed those medium-term rates of earnings growth.

Shifting to the future, estimates from the only analyst covering the company suggest earnings should grow by 29% over the next year. That's shaping up to be materially higher than the 18% growth forecast for the broader market.

In light of this, it's curious that Anton Oilfield Services Group's P/E sits in line with the majority of other companies. Apparently some shareholders are skeptical of the forecasts and have been accepting lower selling prices.

The Bottom Line On Anton Oilfield Services Group's P/E

Anton Oilfield Services Group's stock has a lot of momentum behind it lately, which has brought its P/E level with the market. It's argued the price-to-earnings ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

We've established that Anton Oilfield Services Group currently trades on a lower than expected P/E since its forecast growth is higher than the wider market. There could be some unobserved threats to earnings preventing the P/E ratio from matching the positive outlook. It appears some are indeed anticipating earnings instability, because these conditions should normally provide a boost to the share price.

The company's balance sheet is another key area for risk analysis. You can assess many of the main risks through our free balance sheet analysis for Anton Oilfield Services Group with six simple checks.

Of course, you might also be able to find a better stock than Anton Oilfield Services Group. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:3337

Anton Oilfield Services Group

An investment holding company, operates as an integrated oilfield technology services company in the People’s Republic of China, Iraq, and internationally.

Flawless balance sheet and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

Apple: A Dying Star with an Overpriced Valuation

Fair Value US$177.34|19.1% overvalued

IN

Community Contributor

Avino a case for USD$20 per share within 5 years (assuming $3,500 gold, $100 silver and $4 copper).

Fair Value CA$26.79|86.0% undervalued

AG

Community Contributor

Riding the Defense Boom RENK Sees Revenue Climb at 15% CAGR by FY 2029

Fair Value €69.87|14.3% undervalued

CH

Community Contributor