- Hong Kong

- /

- Energy Services

- /

- SEHK:1960

Shareholders May Be Wary Of Increasing TBK & Sons Holdings Limited's (HKG:1960) CEO Compensation Package

Key Insights

- TBK & Sons Holdings will host its Annual General Meeting on 19th of December

- CEO Han Tan's total compensation includes salary of RM1.03m

- The overall pay is comparable to the industry average

- TBK & Sons Holdings' three-year loss to shareholders was 41% while its EPS was down 83% over the past three years

The results at TBK & Sons Holdings Limited (HKG:1960) have been quite disappointing recently and CEO Han Tan bears some responsibility for this. Shareholders can take the chance to hold the board and management accountable for the unsatisfactory performance at the next AGM on 19th of December. It would also be an opportunity for shareholders to influence management through voting on company resolutions such as executive remuneration, which could impact the firm significantly. From our analysis, we think CEO compensation may need a review in light of the recent performance.

Check out our latest analysis for TBK & Sons Holdings

How Does Total Compensation For Han Tan Compare With Other Companies In The Industry?

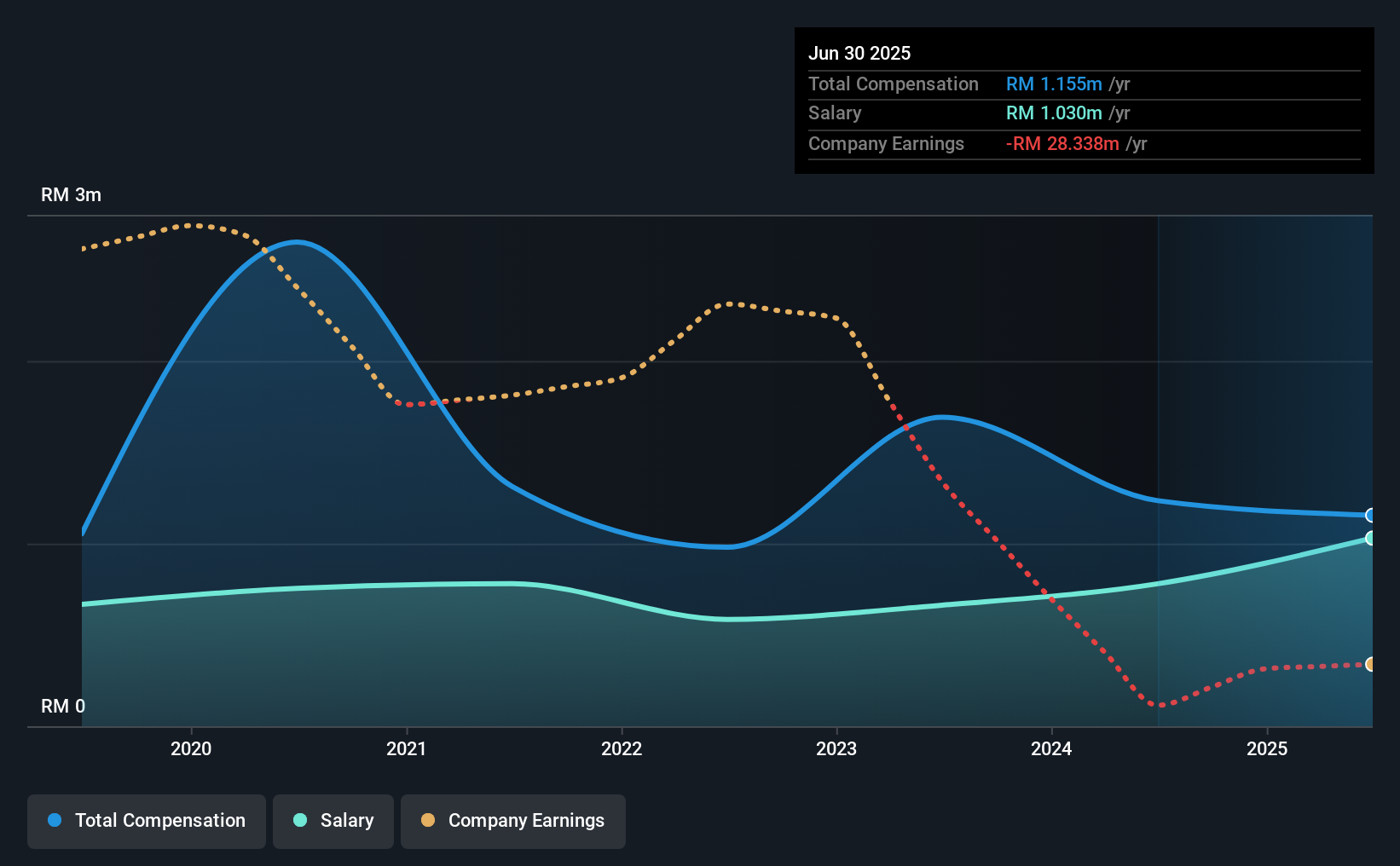

According to our data, TBK & Sons Holdings Limited has a market capitalization of HK$250m, and paid its CEO total annual compensation worth RM1.2m over the year to June 2025. That's slightly lower by 6.5% over the previous year. In particular, the salary of RM1.03m, makes up a huge portion of the total compensation being paid to the CEO.

On comparing similar-sized companies in the Hong Kong Energy Services industry with market capitalizations below HK$1.6b, we found that the median total CEO compensation was RM965k. From this we gather that Han Tan is paid around the median for CEOs in the industry.

| Component | 2025 | 2024 | Proportion (2025) |

| Salary | RM1.0m | RM780k | 89% |

| Other | RM125k | RM455k | 11% |

| Total Compensation | RM1.2m | RM1.2m | 100% |

On an industry level, roughly 77% of total compensation represents salary and 23% is other remuneration. TBK & Sons Holdings is paying a higher share of its remuneration through a salary in comparison to the overall industry. If total compensation veers towards salary, it suggests that the variable portion - which is generally tied to performance, is lower.

A Look at TBK & Sons Holdings Limited's Growth Numbers

TBK & Sons Holdings Limited has reduced its earnings per share by 83% a year over the last three years. It saw its revenue drop 66% over the last year.

Few shareholders would be pleased to read that EPS have declined. And the impression is worse when you consider revenue is down year-on-year. So given this relatively weak performance, shareholders would probably not want to see high compensation for the CEO. Although we don't have analyst forecasts, you might want to assess this data-rich visualization of earnings, revenue and cash flow.

Has TBK & Sons Holdings Limited Been A Good Investment?

The return of -41% over three years would not have pleased TBK & Sons Holdings Limited shareholders. So shareholders would probably want the company to be less generous with CEO compensation.

In Summary...

Along with the business performing poorly, shareholders have suffered with poor share price returns on their investments, suggesting that there's little to no chance of them being in favor of a CEO pay raise. At the upcoming AGM, they can question the management's plans and strategies to turn performance around and reassess their investment thesis in regards to the company.

We can learn a lot about a company by studying its CEO compensation trends, along with looking at other aspects of the business. That's why we did our research, and identified 3 warning signs for TBK & Sons Holdings (of which 1 is significant!) that you should know about in order to have a holistic understanding of the stock.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechValuation is complex, but we're here to simplify it.

Discover if TBK & Sons Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1960

TBK & Sons Holdings

An investment holding company, undertakes civil and structural works in the oil and gas industry in Malaysia and the People’s Republic of China.

Excellent balance sheet with low risk.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

Deep Value Multi Bagger Opportunity

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Trending Discussion