Advertisement

- Hong Kong

- /

- Capital Markets

- /

- SEHK:430

Oriental Explorer Holdings (HKG:430) Is Due To Pay A Dividend Of HK$0.012

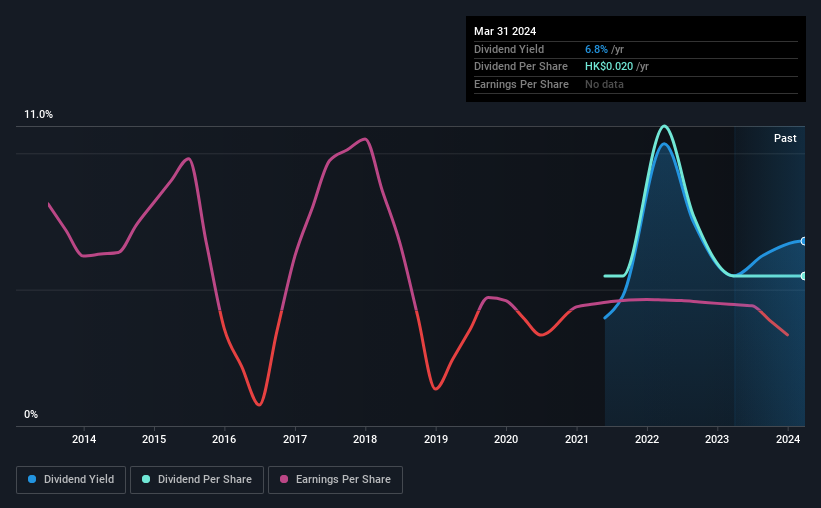

The board of Oriental Explorer Holdings Limited (HKG:430) has announced that it will pay a dividend on the 25th of June, with investors receiving HK$0.012 per share. This makes the dividend yield 6.8%, which will augment investor returns quite nicely.

Check out our latest analysis for Oriental Explorer Holdings

Oriental Explorer Holdings Might Find It Hard To Continue The Dividend

Impressive dividend yields are good, but this doesn't matter much if the payments can't be sustained. Even though Oriental Explorer Holdings isn't generating a profit, it is generating healthy free cash flows that easily cover the dividend. In general, cash flows are more important than the more traditional measures of profit so we feel pretty comfortable with the dividend at this level.

Looking forward, earnings per share could rise by 41.0% over the next year if the trend from the last few years continues. While it is good to see income moving in the right direction, it still looks like the company won't achieve profitability. Unless this happens fairly soon, the dividend could start to come under pressure.

Oriental Explorer Holdings' Dividend Has Lacked Consistency

Looking back, the dividend has been unstable but with a relatively short history, we think it may be a bit early to draw conclusions about long term dividend sustainability. There hasn't been much of a change in the dividend over the last 3 years. The dividend has seen some fluctuations in the past, so even though the dividend was raised this year, we should remember that it has been cut in the past.

The Company Could Face Some Challenges Growing The Dividend

Given that the dividend has been cut in the past, we need to check if earnings are growing and if that might lead to stronger dividends in the future. It's encouraging to see that Oriental Explorer Holdings has been growing its earnings per share at 41% a year over the past five years. While the company is not yet turning a profit, it is growing at a good rate. If this trajectory continues and the company can turn a profit soon, it could bode well for the dividend going forward.

Our Thoughts On Oriental Explorer Holdings' Dividend

Overall, we don't think this company makes a great dividend stock, even though the dividend wasn't cut this year. The payments haven't been particularly stable and we don't see huge growth potential, but with the dividend well covered by cash flows it could prove to be reliable over the short term. We would probably look elsewhere for an income investment.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. As an example, we've identified 3 warning signs for Oriental Explorer Holdings that you should be aware of before investing. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:430

Oriental Explorer Holdings

An investment holding company, engages in the property investment activities in Hong Kong and Mainland China.

Slight with imperfect balance sheet.

Market Insights

Advertisement

Community Narratives

SSAB in pole position when it comes to the combination of steel tariffs and the EU's investment drive

Fair Value SEK 86.87|35.6% undervalued

PI

Community Contributor

The Future of Lennar and Homebuilding Faces Short Term Challenges with Potential for Long Term Growth

Fair Value US$162.49|35.2% undervalued

ZE

Community Contributor

Saudi Aramco (SASE:2222): Not The Sexiest High Dividend Yield Stock, But One With Interesting 'Convertible-Like' Qualities

Fair Value ر.س37.02|30.0% undervalued

EV

Community Contributor