Advertisement

- Hong Kong

- /

- Capital Markets

- /

- SEHK:3908

Here's Why I Think China International Capital (HKG:3908) Might Deserve Your Attention Today

For beginners, it can seem like a good idea (and an exciting prospect) to buy a company that tells a good story to investors, even if it completely lacks a track record of revenue and profit. And in their study titled Who Falls Prey to the Wolf of Wall Street?' Leuz et. al. found that it is 'quite common' for investors to lose money by buying into 'pump and dump' schemes.

In the age of tech-stock blue-sky investing, my choice may seem old fashioned; I still prefer profitable companies like China International Capital (HKG:3908). While that doesn't make the shares worth buying at any price, you can't deny that successful capitalism requires profit, eventually. In comparison, loss making companies act like a sponge for capital - but unlike such a sponge they do not always produce something when squeezed.

See our latest analysis for China International Capital

How Quickly Is China International Capital Increasing Earnings Per Share?

As one of my mentors once told me, share price follows earnings per share (EPS). That means EPS growth is considered a real positive by most successful long-term investors. It certainly is nice to see that China International Capital has managed to grow EPS by 30% per year over three years. As a general rule, we'd say that if a company can keep up that sort of growth, shareholders will be smiling.

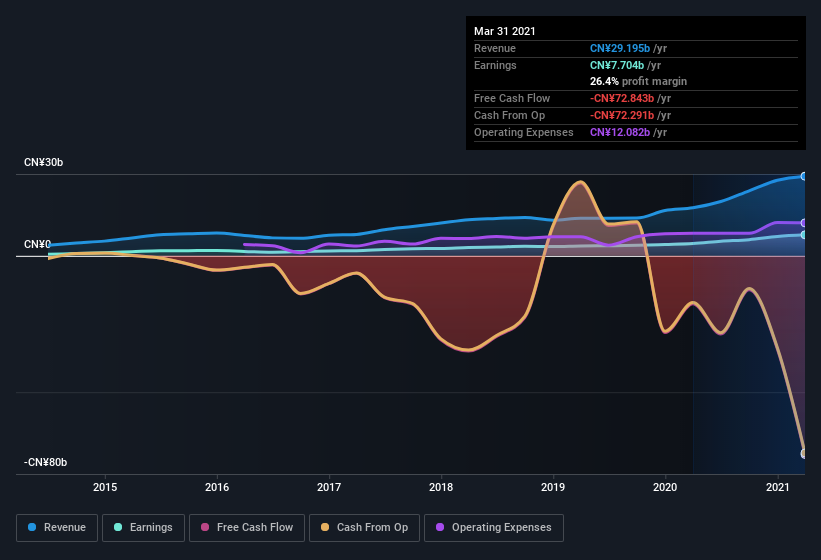

I like to see top-line growth as an indication that growth is sustainable, and I look for a high earnings before interest and taxation (EBIT) margin to point to a competitive moat (though some companies with low margins also have moats). Not all of China International Capital's revenue this year is revenue from operations, so keep in mind the revenue and margin numbers I've used might not be the best representation of the underlying business. China International Capital maintained stable EBIT margins over the last year, all while growing revenue 66% to CN¥29b. That's a real positive.

You can take a look at the company's revenue and earnings growth trend, in the chart below. For finer detail, click on the image.

You don't drive with your eyes on the rear-view mirror, so you might be more interested in this free report showing analyst forecasts for China International Capital's future profits.

Are China International Capital Insiders Aligned With All Shareholders?

Like the kids in the streets standing up for their beliefs, insider share purchases give me reason to believe in a brighter future. That's because insider buying often indicates that those closest to the company have confidence that the share price will perform well. However, insiders are sometimes wrong, and we don't know the exact thinking behind their acquisitions.

First things first; I didn't see insiders sell China International Capital shares in the last year. Even better, though, is that the CEO & Executive Director, Zhaohui Huang, bought a whopping CN¥3.7m worth of shares, paying about CN¥12.62 per share, on average. Big buys like that give me a sense of opportunity; actions speak louder than words.

The good news, alongside the insider buying, for China International Capital bulls is that insiders (collectively) have a meaningful investment in the stock. Indeed, they hold CN¥274m worth of its stock. That shows significant buy-in, and may indicate conviction in the business strategy. Even though that's only about 0.1% of the company, it's enough money to indicate alignment between the leaders of the business and ordinary shareholders.

Is China International Capital Worth Keeping An Eye On?

For growth investors like me, China International Capital's raw rate of earnings growth is a beacon in the night. Better still, insiders own a large chunk of the company and one has even been buying more shares. So I do think this is one stock worth watching. Even so, be aware that China International Capital is showing 2 warning signs in our investment analysis , and 1 of those is a bit unpleasant...

As a growth investor I do like to see insider buying. But China International Capital isn't the only one. You can see a a free list of them here.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

When trading stocks or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SEHK:3908

China International Capital

Provides financial services in Mainland China and internationally.

Reasonable growth potential with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Nike's Direct-to-Consumer Focus Will Drive Future Growth

Fair Value US$87.90|18.2% undervalued

UN

Community Contributor

Novo Nordisk will dominate GLP-1 market with Ozempic and Wegovy growth

Fair Value US$89.59|12.1% undervalued

BE

Community Contributor

Rheinmetall could get 20-25% of EU-NATO 3%-GDP defence spending

Fair Value €7.57k|82.8% undervalued

NO

Community Contributor