Advertisement

- Hong Kong

- /

- Hospitality

- /

- SEHK:8412

Slammed 30% New Amante Group Limited (HKG:8412) Screens Well Here But There Might Be A Catch

The New Amante Group Limited (HKG:8412) share price has fared very poorly over the last month, falling by a substantial 30%. Still, a bad month hasn't completely ruined the past year with the stock gaining 46%, which is great even in a bull market.

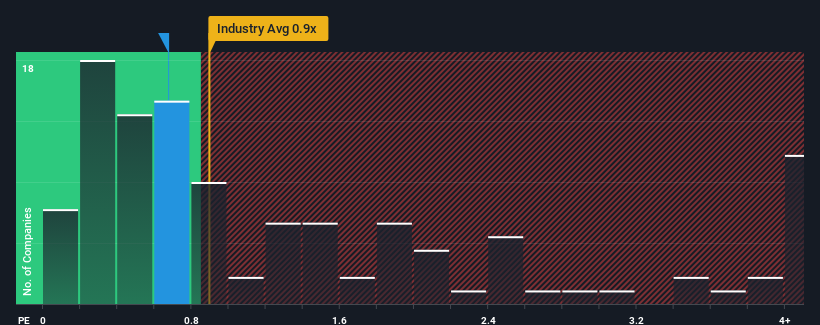

Even after such a large drop in price, you could still be forgiven for feeling indifferent about New Amante Group's P/S ratio of 0.7x, since the median price-to-sales (or "P/S") ratio for the Hospitality industry in Hong Kong is also close to 0.9x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/S.

Check out our latest analysis for New Amante Group

What Does New Amante Group's Recent Performance Look Like?

New Amante Group certainly has been doing a great job lately as it's been growing its revenue at a really rapid pace. The P/S is probably moderate because investors think this strong revenue growth might not be enough to outperform the broader industry in the near future. If that doesn't eventuate, then existing shareholders have reason to be feeling optimistic about the future direction of the share price.

Want the full picture on earnings, revenue and cash flow for the company? Then our free report on New Amante Group will help you shine a light on its historical performance.What Are Revenue Growth Metrics Telling Us About The P/S?

New Amante Group's P/S ratio would be typical for a company that's only expected to deliver moderate growth, and importantly, perform in line with the industry.

Retrospectively, the last year delivered an exceptional 145% gain to the company's top line. Pleasingly, revenue has also lifted 226% in aggregate from three years ago, thanks to the last 12 months of growth. Accordingly, shareholders would have definitely welcomed those medium-term rates of revenue growth.

Comparing that recent medium-term revenue trajectory with the industry's one-year growth forecast of 24% shows it's noticeably more attractive.

In light of this, it's curious that New Amante Group's P/S sits in line with the majority of other companies. It may be that most investors are not convinced the company can maintain its recent growth rates.

What Does New Amante Group's P/S Mean For Investors?

With its share price dropping off a cliff, the P/S for New Amante Group looks to be in line with the rest of the Hospitality industry. We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

We didn't quite envision New Amante Group's P/S sitting in line with the wider industry, considering the revenue growth over the last three-year is higher than the current industry outlook. It'd be fair to assume that potential risks the company faces could be the contributing factor to the lower than expected P/S. At least the risk of a price drop looks to be subdued if recent medium-term revenue trends continue, but investors seem to think future revenue could see some volatility.

We don't want to rain on the parade too much, but we did also find 3 warning signs for New Amante Group (1 is concerning!) that you need to be mindful of.

If these risks are making you reconsider your opinion on New Amante Group, explore our interactive list of high quality stocks to get an idea of what else is out there.

Valuation is complex, but we're here to simplify it.

Discover if New Amante Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:8412

New Amante Group

An investment holding company, engages in the operation of club and entertainment, and restaurant businesses primarily in Hong Kong.

Low and slightly overvalued.

Market Insights

Advertisement

Community Narratives

Scaling up in building materials with smart M&A and growing profitability

Fair Value US$2.77|30.0% undervalued

CM

Community Contributor

Hims: The Platform Powering Personalised Healthcare

Fair Value US$114.01|51.9% undervalued

BL

Community Contributor

Undervalued lottery company with strong fundamentals

Fair Value AU$15.00|34.5% undervalued

RO

Community Contributor

Proximus, transferring money from the impatient to the patient investor

Fair Value €16.62|55.1% undervalued

AX

Community Contributor