Advertisement

- Hong Kong

- /

- Hospitality

- /

- SEHK:520

What Xiabuxiabu Catering Management (China) Holdings Co., Ltd.'s (HKG:520) 26% Share Price Gain Is Not Telling You

Xiabuxiabu Catering Management (China) Holdings Co., Ltd. (HKG:520) shares have had a really impressive month, gaining 26% after a shaky period beforehand. But the last month did very little to improve the 59% share price decline over the last year.

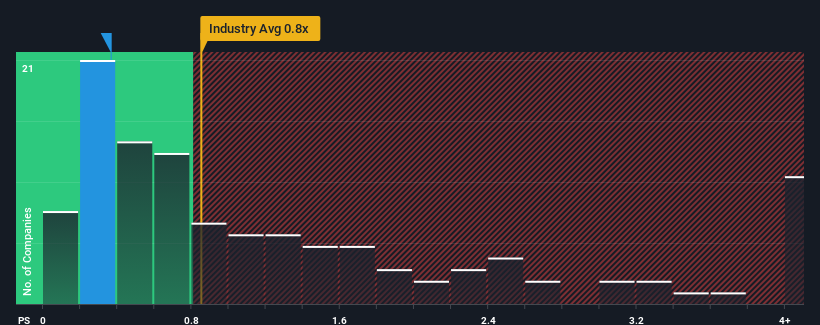

Even after such a large jump in price, it's still not a stretch to say that Xiabuxiabu Catering Management (China) Holdings' price-to-sales (or "P/S") ratio of 0.4x right now seems quite "middle-of-the-road" compared to the Hospitality industry in Hong Kong, where the median P/S ratio is around 0.8x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/S.

Check out our latest analysis for Xiabuxiabu Catering Management (China) Holdings

How Has Xiabuxiabu Catering Management (China) Holdings Performed Recently?

With revenue growth that's inferior to most other companies of late, Xiabuxiabu Catering Management (China) Holdings has been relatively sluggish. One possibility is that the P/S ratio is moderate because investors think this lacklustre revenue performance will turn around. If not, then existing shareholders may be a little nervous about the viability of the share price.

Want the full picture on analyst estimates for the company? Then our free report on Xiabuxiabu Catering Management (China) Holdings will help you uncover what's on the horizon.What Are Revenue Growth Metrics Telling Us About The P/S?

The only time you'd be comfortable seeing a P/S like Xiabuxiabu Catering Management (China) Holdings' is when the company's growth is tracking the industry closely.

Taking a look back first, we see that the company grew revenue by an impressive 25% last year. As a result, it also grew revenue by 8.5% in total over the last three years. So we can start by confirming that the company has actually done a good job of growing revenue over that time.

Shifting to the future, estimates from the eleven analysts covering the company suggest revenue should grow by 12% each year over the next three years. Meanwhile, the rest of the industry is forecast to expand by 16% per annum, which is noticeably more attractive.

With this information, we find it interesting that Xiabuxiabu Catering Management (China) Holdings is trading at a fairly similar P/S compared to the industry. Apparently many investors in the company are less bearish than analysts indicate and aren't willing to let go of their stock right now. Maintaining these prices will be difficult to achieve as this level of revenue growth is likely to weigh down the shares eventually.

The Bottom Line On Xiabuxiabu Catering Management (China) Holdings' P/S

Xiabuxiabu Catering Management (China) Holdings appears to be back in favour with a solid price jump bringing its P/S back in line with other companies in the industry While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

Given that Xiabuxiabu Catering Management (China) Holdings' revenue growth projections are relatively subdued in comparison to the wider industry, it comes as a surprise to see it trading at its current P/S ratio. When we see companies with a relatively weaker revenue outlook compared to the industry, we suspect the share price is at risk of declining, sending the moderate P/S lower. A positive change is needed in order to justify the current price-to-sales ratio.

Many other vital risk factors can be found on the company's balance sheet. Our free balance sheet analysis for Xiabuxiabu Catering Management (China) Holdings with six simple checks will allow you to discover any risks that could be an issue.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:520

Xiabuxiabu Catering Management (China) Holdings

An investment holding company, operates Chinese hotpot restaurants in the People’s Republic of China.

Undervalued with moderate growth potential.

Market Insights

Advertisement

Community Narratives

The Most Undervalued of the Magnificent 7

Fair Value US$237.43|36.3% undervalued

IN

Community Contributor

PVA TePla's New Strategy Aims for 22% Revenue Growth in Semiconductor Recovery

Fair Value €19.19|20.8% undervalued

MI

Community Contributor