Advertisement

- Hong Kong

- /

- Consumer Services

- /

- SEHK:1890

The Trends At China Kepei Education Group (HKG:1890) That You Should Know About

Did you know there are some financial metrics that can provide clues of a potential multi-bagger? Typically, we'll want to notice a trend of growing return on capital employed (ROCE) and alongside that, an expanding base of capital employed. Basically this means that a company has profitable initiatives that it can continue to reinvest in, which is a trait of a compounding machine. With that in mind, the ROCE of China Kepei Education Group (HKG:1890) looks decent, right now, so lets see what the trend of returns can tell us.

Understanding Return On Capital Employed (ROCE)

Just to clarify if you're unsure, ROCE is a metric for evaluating how much pre-tax income (in percentage terms) a company earns on the capital invested in its business. Analysts use this formula to calculate it for China Kepei Education Group:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.14 = CN¥443m ÷ (CN¥3.7b - CN¥522m) (Based on the trailing twelve months to June 2020).

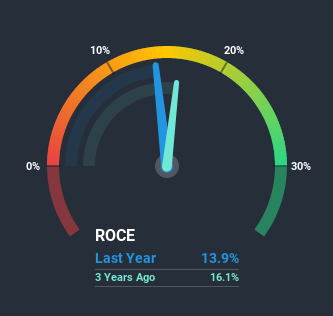

Therefore, China Kepei Education Group has an ROCE of 14%. On its own, that's a standard return, however it's much better than the 9.0% generated by the Consumer Services industry.

Check out our latest analysis for China Kepei Education Group

Above you can see how the current ROCE for China Kepei Education Group compares to its prior returns on capital, but there's only so much you can tell from the past. If you'd like, you can check out the forecasts from the analysts covering China Kepei Education Group here for free.

The Trend Of ROCE

The trend of ROCE doesn't stand out much, but returns on a whole are decent. The company has consistently earned 14% for the last four years, and the capital employed within the business has risen 208% in that time. Since 14% is a moderate ROCE though, it's good to see a business can continue to reinvest at these decent rates of return. Over long periods of time, returns like these might not be too exciting, but with consistency they can pay off in terms of share price returns.

One more thing to note, even though ROCE has remained relatively flat over the last four years, the reduction in current liabilities to 14% of total assets, is good to see from a business owner's perspective. This can eliminate some of the risks inherent in the operations because the business has less outstanding obligations to their suppliers and or short-term creditors than they did previously.

The Key Takeaway

The main thing to remember is that China Kepei Education Group has proven its ability to continually reinvest at respectable rates of return. Therefore it's no surprise that shareholders have earned a respectable 22% return if they held over the last year. So while investors seem to be recognizing these promising trends, we still believe the stock deserves further research.

China Kepei Education Group could be trading at an attractive price in other respects, so you might find our free intrinsic value estimation on our platform quite valuable.

While China Kepei Education Group isn't earning the highest return, check out this free list of companies that are earning high returns on equity with solid balance sheets.

If you decide to trade China Kepei Education Group, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SEHK:1890

China Kepei Education Group

An investment holding company, provides private vocational education services focusing on profession-oriented and vocational education in the People’s Republic of China.

Undervalued with adequate balance sheet and pays a dividend.

Market Insights

Advertisement

Community Narratives

Nike's Direct-to-Consumer Focus Will Drive Future Growth

Fair Value US$87.90|16.6% undervalued

UN

Community Contributor

Novo Nordisk will dominate GLP-1 market with Ozempic and Wegovy growth

Fair Value US$89.59|9.6% undervalued

BE

Community Contributor

Rheinmetall could get 20-25% of EU-NATO 3%-GDP defence spending

Fair Value €7.57k|80.9% undervalued

NO

Community Contributor