Advertisement

- Hong Kong

- /

- Energy Services

- /

- SEHK:3337

Asian Growth Stocks With Strong Insider Confidence

Simply Wall St

Reviewed by Simply Wall St

In the current climate of heightened uncertainty and mixed economic signals, Asian markets have shown resilience, with some sectors experiencing growth despite global challenges. In this environment, companies with strong insider ownership can signal confidence in their long-term prospects, making them attractive to investors seeking stability and potential growth.

Top 10 Growth Companies With High Insider Ownership In Asia

| Name | Insider Ownership | Earnings Growth |

| Zhejiang Jolly PharmaceuticalLTD (SZSE:300181) | 23.3% | 26% |

| Sineng ElectricLtd (SZSE:300827) | 36.3% | 41.4% |

| Seojin SystemLtd (KOSDAQ:A178320) | 32.1% | 39.3% |

| Laopu Gold (SEHK:6181) | 36.4% | 47.2% |

| Global Tax Free (KOSDAQ:A204620) | 21.8% | 89.3% |

| M31 Technology (TPEX:6643) | 27.2% | 72.4% |

| BIWIN Storage Technology (SHSE:688525) | 18.9% | 57.6% |

| Fulin Precision (SZSE:300432) | 13.6% | 78.6% |

| Ascentage Pharma Group International (SEHK:6855) | 17.9% | 59.9% |

| Synspective (TSE:290A) | 13.2% | 37.4% |

We'll examine a selection from our screener results.

DPC Dash (SEHK:1405)

Simply Wall St Growth Rating: ★★★★★☆

Overview: DPC Dash Ltd, along with its subsidiaries, operates a chain of fast-food restaurants in the People's Republic of China and has a market cap of HK$14.12 billion.

Operations: The company's revenue primarily comes from its fast-food restaurant operations in the People's Republic of China, totaling CN¥3.72 billion.

Insider Ownership: 38.1%

Revenue Growth Forecast: 25.7% p.a.

DPC Dash is experiencing significant growth, with revenue forecasted to increase by 25.7% annually, outpacing the Hong Kong market's 7.6% growth rate. The company reported a net income of CNY 55.2 million for 2024, reversing a prior loss and reflecting strong earnings momentum with profits expected to grow over the next three years. Despite trading slightly below fair value estimates and low Return on Equity forecasts, these factors may appeal to investors prioritizing insider ownership stability amidst board changes.

- Click here to discover the nuances of DPC Dash with our detailed analytical future growth report.

- Our valuation report unveils the possibility DPC Dash's shares may be trading at a premium.

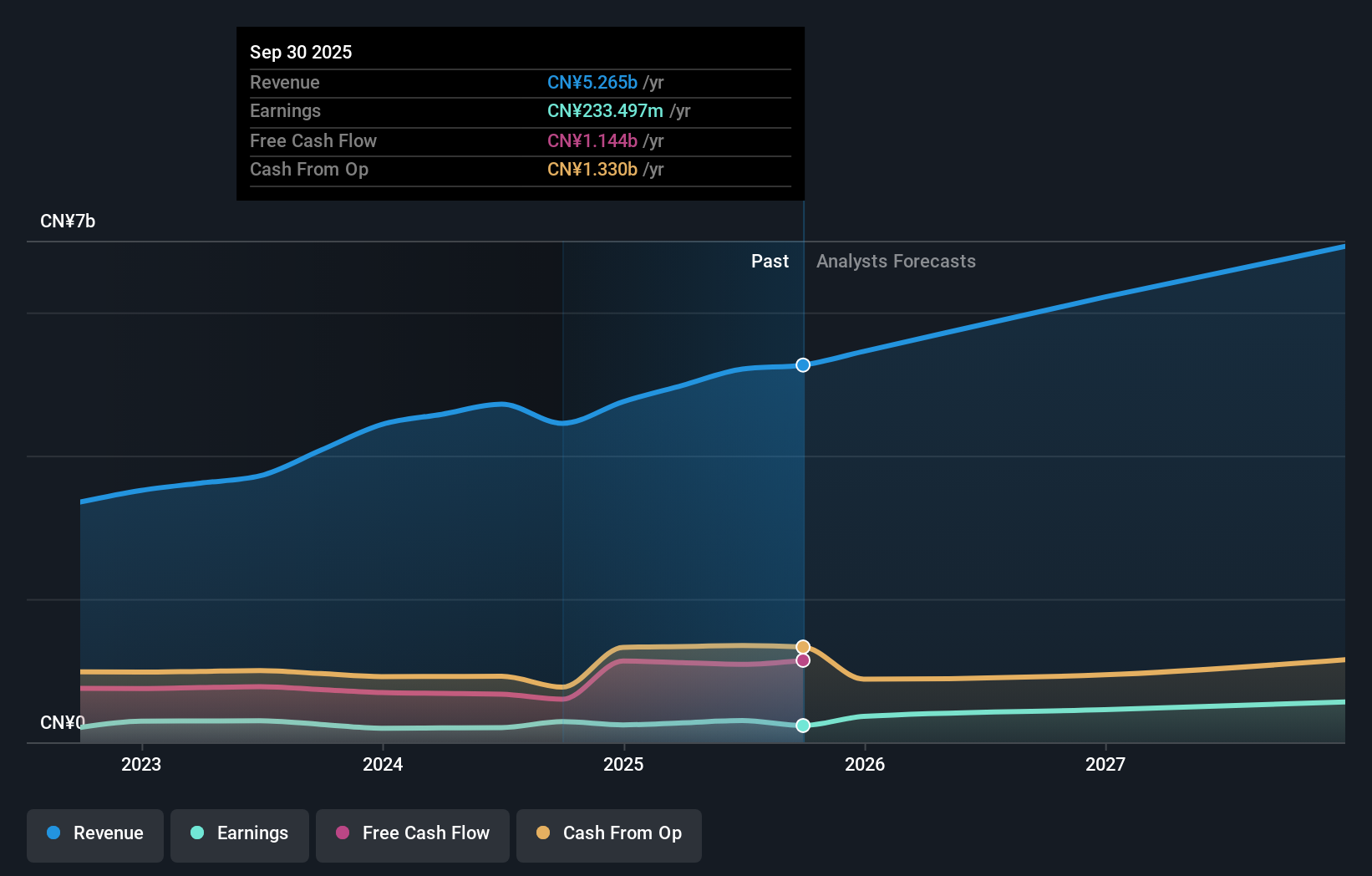

Anton Oilfield Services Group (SEHK:3337)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Anton Oilfield Services Group is an investment holding company offering oilfield engineering and technical services to oil companies in China, Iraq, and internationally, with a market cap of HK$2.78 billion.

Operations: The company's revenue segments consist of Inspection Services (CN¥421.04 million), Drilling Rig Services (CN¥358.89 million), Oilfield Technical Services (CN¥2.13 billion), and Oilfield Management Services (CN¥1.85 billion).

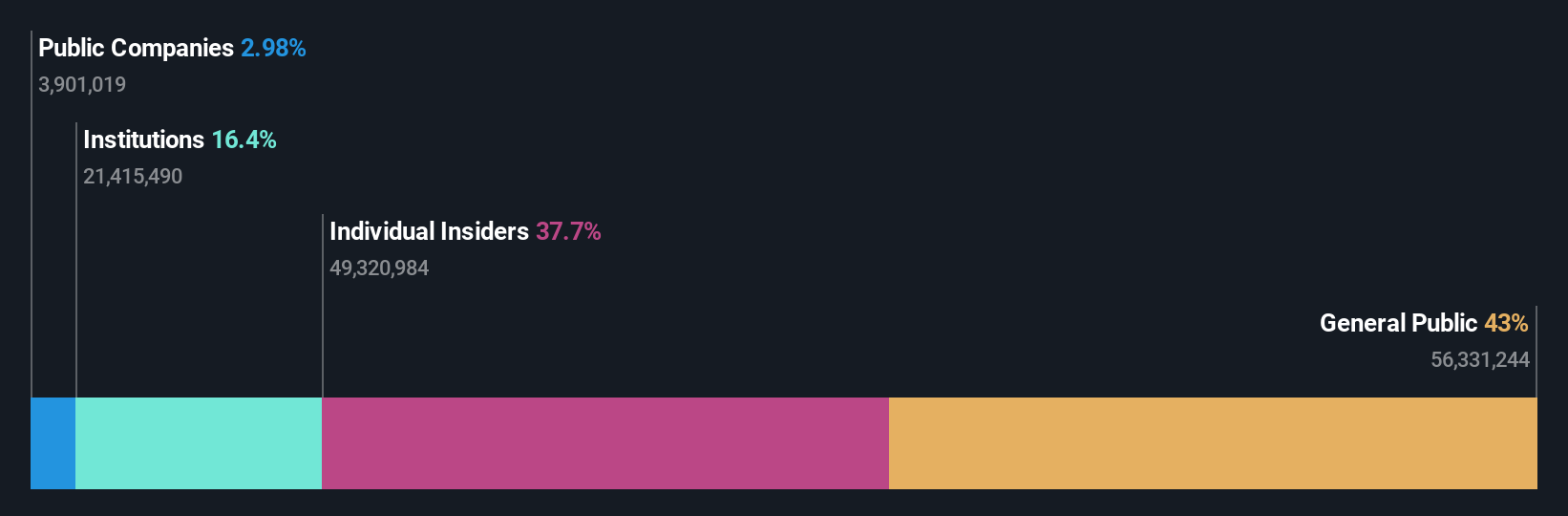

Insider Ownership: 25.9%

Revenue Growth Forecast: 15.4% p.a.

Anton Oilfield Services Group is trading significantly below its estimated fair value, with earnings projected to grow substantially at 23.6% annually, surpassing the Hong Kong market's growth rate. Despite a recent decline in sales to CNY 146.51 million, revenue and net income have increased year-over-year. The company's Return on Equity forecast remains low at 9.5%, yet insider ownership stability may attract investors amid strategic board changes and a proposed dividend of RMB 0.025 per share for 2024.

- Unlock comprehensive insights into our analysis of Anton Oilfield Services Group stock in this growth report.

- Our expertly prepared valuation report Anton Oilfield Services Group implies its share price may be lower than expected.

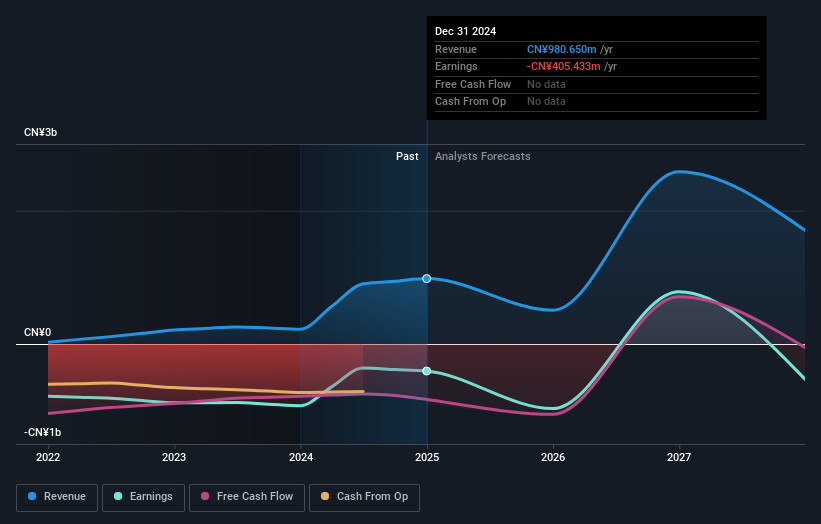

Ascentage Pharma Group International (SEHK:6855)

Simply Wall St Growth Rating: ★★★★★★

Overview: Ascentage Pharma Group International is a clinical-stage biotechnology company focused on developing therapies for cancers, chronic hepatitis B virus (HBV), and age-related diseases in Mainland China, with a market cap of HK$12.61 billion.

Operations: The company's revenue primarily comes from the development and sale of novel small-scale therapies, amounting to CN¥903.03 million.

Insider Ownership: 17.9%

Revenue Growth Forecast: 22.9% p.a.

Ascentage Pharma Group International shows promising growth potential with a significant increase in sales from CNY 221.98 million to CNY 980.65 million year-over-year, while reducing its net loss substantially. Its pipeline of innovative cancer therapies, including drugs with Breakthrough Therapy Designations in China, highlights its strategic focus on unmet medical needs. Although shareholders faced dilution recently, the company's high insider ownership and expected profitability within three years suggest strong alignment with long-term growth objectives.

- Take a closer look at Ascentage Pharma Group International's potential here in our earnings growth report.

- According our valuation report, there's an indication that Ascentage Pharma Group International's share price might be on the expensive side.

Make It Happen

- Navigate through the entire inventory of 648 Fast Growing Asian Companies With High Insider Ownership here.

- Looking For Alternative Opportunities? AI is about to change healthcare. These 24 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:3337

Anton Oilfield Services Group

An investment holding company, operates as an integrated oilfield technology services company in the People’s Republic of China, Iraq, and internationally.

Flawless balance sheet and undervalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.4% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|6.1% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.2% undervalued

YI

Community Contributor

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.6% undervalued

BE

Community Contributor