- Hong Kong

- /

- Food and Staples Retail

- /

- SEHK:1587

Most Shareholders Will Probably Find That The Compensation For Shineroad International Holdings Limited's (HKG:1587) CEO Is Reasonable

Key Insights

- Shineroad International Holdings' Annual General Meeting to take place on 17th of May

- Salary of CN¥652.0k is part of CEO Xin Rong Huang's total remuneration

- Total compensation is 64% below industry average

- Shineroad International Holdings' total shareholder return over the past three years was 11% while its EPS was down 17% over the past three years

Performance at Shineroad International Holdings Limited (HKG:1587) has been rather uninspiring recently and shareholders may be wondering how CEO Xin Rong Huang plans to fix this. One way they can exercise their influence on management is through voting on resolutions, such as executive remuneration at the next AGM, coming up on 17th of May. Voting on executive pay could be a powerful way to influence management, as studies have shown that the right compensation incentives impact company performance. We think CEO compensation looks appropriate given the data we have put together.

See our latest analysis for Shineroad International Holdings

How Does Total Compensation For Xin Rong Huang Compare With Other Companies In The Industry?

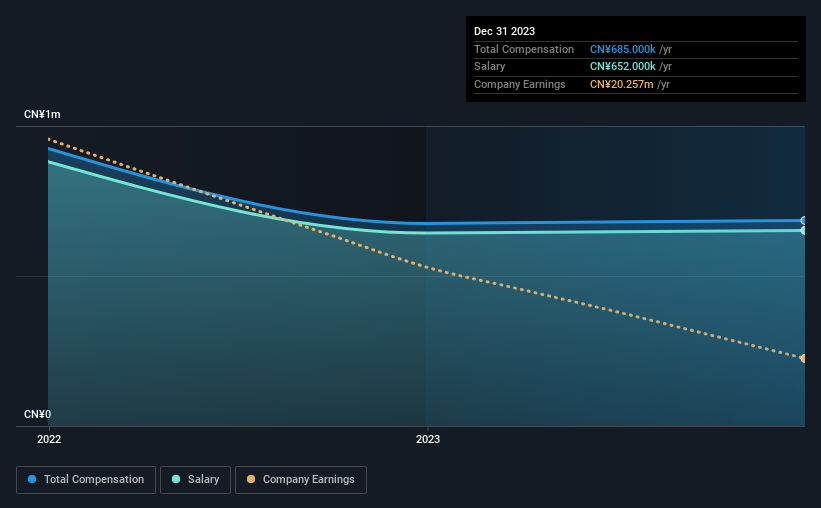

Our data indicates that Shineroad International Holdings Limited has a market capitalization of HK$299m, and total annual CEO compensation was reported as CN¥685k for the year to December 2023. That is, the compensation was roughly the same as last year. We note that the salary portion, which stands at CN¥652.0k constitutes the majority of total compensation received by the CEO.

On comparing similar-sized companies in the Hong Kong Consumer Retailing industry with market capitalizations below HK$1.6b, we found that the median total CEO compensation was CN¥1.9m. Accordingly, Shineroad International Holdings pays its CEO under the industry median.

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | CN¥652k | CN¥643k | 95% |

| Other | CN¥33k | CN¥32k | 5% |

| Total Compensation | CN¥685k | CN¥675k | 100% |

Speaking on an industry level, nearly 63% of total compensation represents salary, while the remainder of 37% is other remuneration. Shineroad International Holdings pays a high salary, concentrating more on this aspect of compensation in comparison to non-salary pay. If total compensation veers towards salary, it suggests that the variable portion - which is generally tied to performance, is lower.

Shineroad International Holdings Limited's Growth

Over the last three years, Shineroad International Holdings Limited has shrunk its earnings per share by 17% per year. Its revenue is down 6.1% over the previous year.

Few shareholders would be pleased to read that EPS have declined. And the impression is worse when you consider revenue is down year-on-year. These factors suggest that the business performance wouldn't really justify a high pay packet for the CEO. We don't have analyst forecasts, but you could get a better understanding of its growth by checking out this more detailed historical graph of earnings, revenue and cash flow.

Has Shineroad International Holdings Limited Been A Good Investment?

Shineroad International Holdings Limited has served shareholders reasonably well, with a total return of 11% over three years. But they probably don't want to see the CEO paid more than is normal for companies around the same size.

To Conclude...

Shineroad International Holdings pays its CEO a majority of compensation through a salary. While it's true that shareholders have seen decent returns, it's hard to overlook the lack of earnings growth and this makes us wonder if the current returns can continue. These are are some concerns that shareholders may want to address the board when they revisit their investment thesis.

CEO compensation is a crucial aspect to keep your eyes on but investors also need to keep their eyes open for other issues related to business performance. We did our research and spotted 3 warning signs for Shineroad International Holdings that investors should look into moving forward.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1587

Shineroad International Holdings

An investment holding company, distributes food ingredients, food additives, and packaging materials in Mainland China.

Excellent balance sheet with proven track record.

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

A tech powerhouse quietly powering the world’s AI infrastructure.

Keppel DC REIT (SGX: AJBU) is a resilient gem in the data center space.

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)