- Hong Kong

- /

- Medical Equipment

- /

- SEHK:2190

Top 3 Growth Companies With High Insider Ownership On SEHK In August 2024

Reviewed by Simply Wall St

As global markets navigate through volatility and economic uncertainties, the Hong Kong market has shown resilience with the Hang Seng Index gaining 0.85% recently. In this environment, growth companies with high insider ownership can be particularly appealing as they often signal strong internal confidence and alignment of interests between shareholders and management. When evaluating stocks in such a climate, focusing on firms where insiders hold significant stakes can provide added assurance of their commitment to driving long-term value. Here are three standout growth companies on the SEHK that exemplify these qualities in August 2024.

Top 10 Growth Companies With High Insider Ownership In Hong Kong

| Name | Insider Ownership | Earnings Growth |

| iDreamSky Technology Holdings (SEHK:1119) | 18.8% | 104.1% |

| Pacific Textiles Holdings (SEHK:1382) | 11.2% | 37.7% |

| Tian Tu Capital (SEHK:1973) | 34% | 70.5% |

| Adicon Holdings (SEHK:9860) | 22.4% | 28.3% |

| Zylox-Tonbridge Medical Technology (SEHK:2190) | 18.7% | 79.3% |

| Zhejiang Leapmotor Technology (SEHK:9863) | 15% | 74.3% |

| Biocytogen Pharmaceuticals (Beijing) (SEHK:2315) | 13.9% | 100.1% |

| Ocumension Therapeutics (SEHK:1477) | 23.3% | 93.7% |

| Beijing Airdoc Technology (SEHK:2251) | 28.6% | 83.9% |

| DPC Dash (SEHK:1405) | 38.2% | 91.4% |

Here's a peek at a few of the choices from the screener.

Kuaishou Technology (SEHK:1024)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Kuaishou Technology, an investment holding company with a market cap of HK$196.19 billion, offers live streaming, online marketing, and other services in the People’s Republic of China.

Operations: The company generates CN¥114.72 billion from domestic operations and CN¥2.94 billion from overseas activities.

Insider Ownership: 19.2%

Kuaishou Technology, known for its substantial insider ownership, is trading at 53% below estimated fair value and has a high forecasted annual profit growth of 22.4%, outpacing the Hong Kong market. Despite slower revenue growth (9.7%), it remains profitable with significant upgrades to its Kling AI video generation model, enhancing user engagement and expanding subscription services. Recent earnings showed strong performance with CNY 4.12 billion net income for Q1 2024, reversing losses from the previous year.

- Unlock comprehensive insights into our analysis of Kuaishou Technology stock in this growth report.

- According our valuation report, there's an indication that Kuaishou Technology's share price might be on the cheaper side.

Pacific Textiles Holdings (SEHK:1382)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Pacific Textiles Holdings Limited manufactures and trades textile products across various regions including China, Vietnam, Bangladesh, Hong Kong, and internationally, with a market cap of HK$2.26 billion.

Operations: The company's revenue primarily stems from the manufacturing and trading of textile products, amounting to HK$4.67 billion.

Insider Ownership: 11.2%

Pacific Textiles Holdings shows strong insider ownership and is trading at 45.8% below its estimated fair value. However, the company's revenue growth forecast of 11.8% per year is slower than desired for high-growth companies, and recent earnings have declined with net income dropping from HK$268.57 million to HK$167.12 million year-over-year. Despite a significant earnings growth forecast of 37.67% annually, profit margins have decreased from 5.4% to 3.6%.

- Get an in-depth perspective on Pacific Textiles Holdings' performance by reading our analyst estimates report here.

- Our valuation report here indicates Pacific Textiles Holdings may be undervalued.

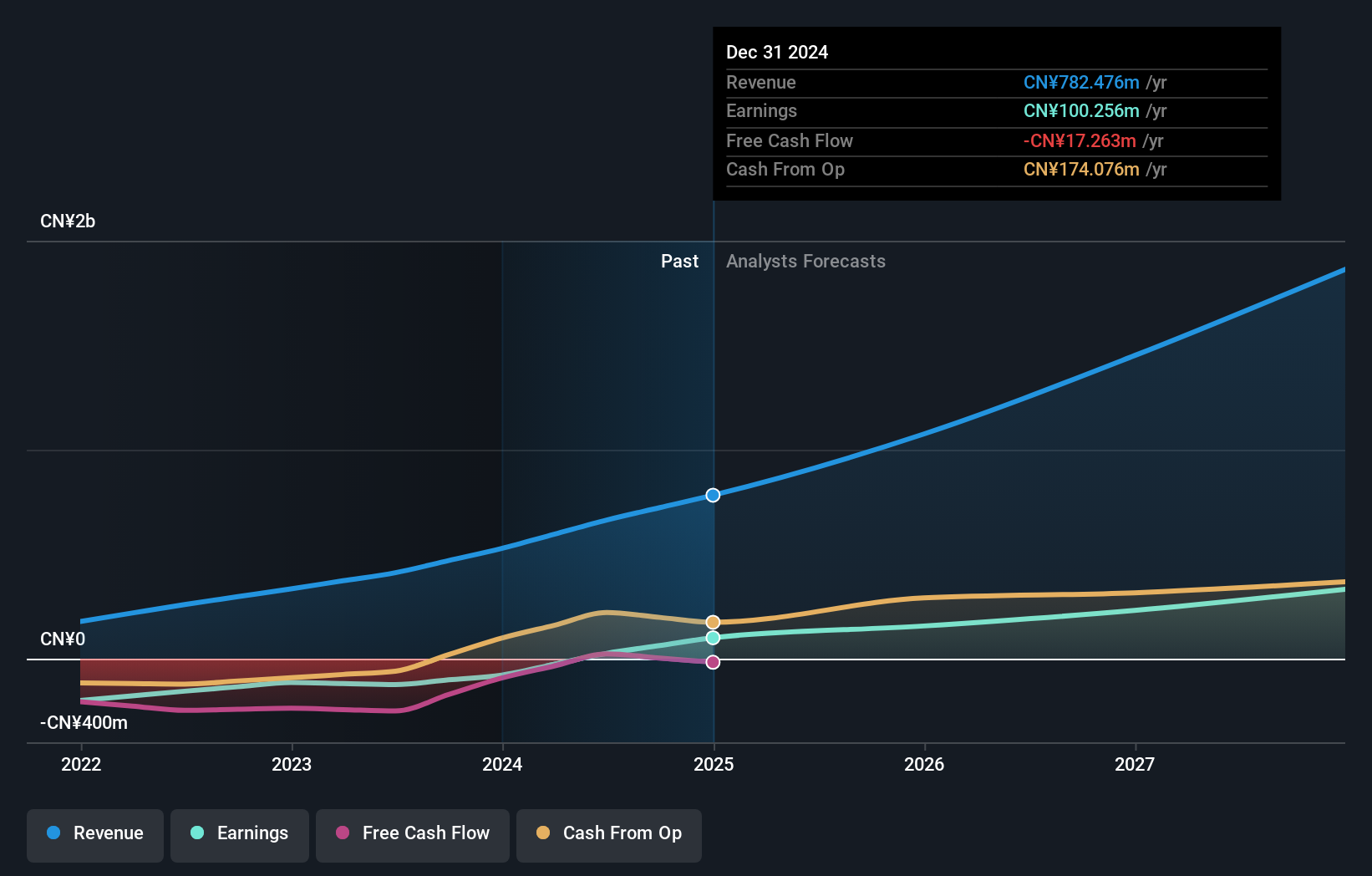

Zylox-Tonbridge Medical Technology (SEHK:2190)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Zylox-Tonbridge Medical Technology Co., Ltd. is a medical device company that offers neuro- and peripheral-vascular interventional devices in China and internationally, with a market cap of HK$3.29 billion.

Operations: The company generates revenue from the sales of neurovascular and peripheral-vascular interventional surgical devices, amounting to CN¥527.75 million.

Insider Ownership: 18.7%

Zylox-Tonbridge Medical Technology is expected to see revenue growth of 24.1% per year, surpassing the Hong Kong market average. The company anticipates becoming profitable within three years, driven by a strong product portfolio and strategic sales efforts. Recent guidance indicates a significant revenue increase to at least RMB 360 million for H1 2024, alongside an expected net profit of RMB 50 million. High insider ownership aligns with these positive growth prospects.

- Take a closer look at Zylox-Tonbridge Medical Technology's potential here in our earnings growth report.

- Our expertly prepared valuation report Zylox-Tonbridge Medical Technology implies its share price may be lower than expected.

Summing It All Up

- Explore the 51 names from our Fast Growing SEHK Companies With High Insider Ownership screener here.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Zylox-Tonbridge Medical Technology might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:2190

Zylox-Tonbridge Medical Technology

A medical device company, provides neuro- and peripheral-vascular interventional medical devices the People’s Republic of China and internationally.

High growth potential with adequate balance sheet.