Advertisement

- Hong Kong

- /

- Consumer Durables

- /

- SEHK:1070

These 4 Measures Indicate That TCL Electronics Holdings (HKG:1070) Is Using Debt Reasonably Well

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that TCL Electronics Holdings Limited (HKG:1070) does use debt in its business. But is this debt a concern to shareholders?

When Is Debt A Problem?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we think about a company's use of debt, we first look at cash and debt together.

How Much Debt Does TCL Electronics Holdings Carry?

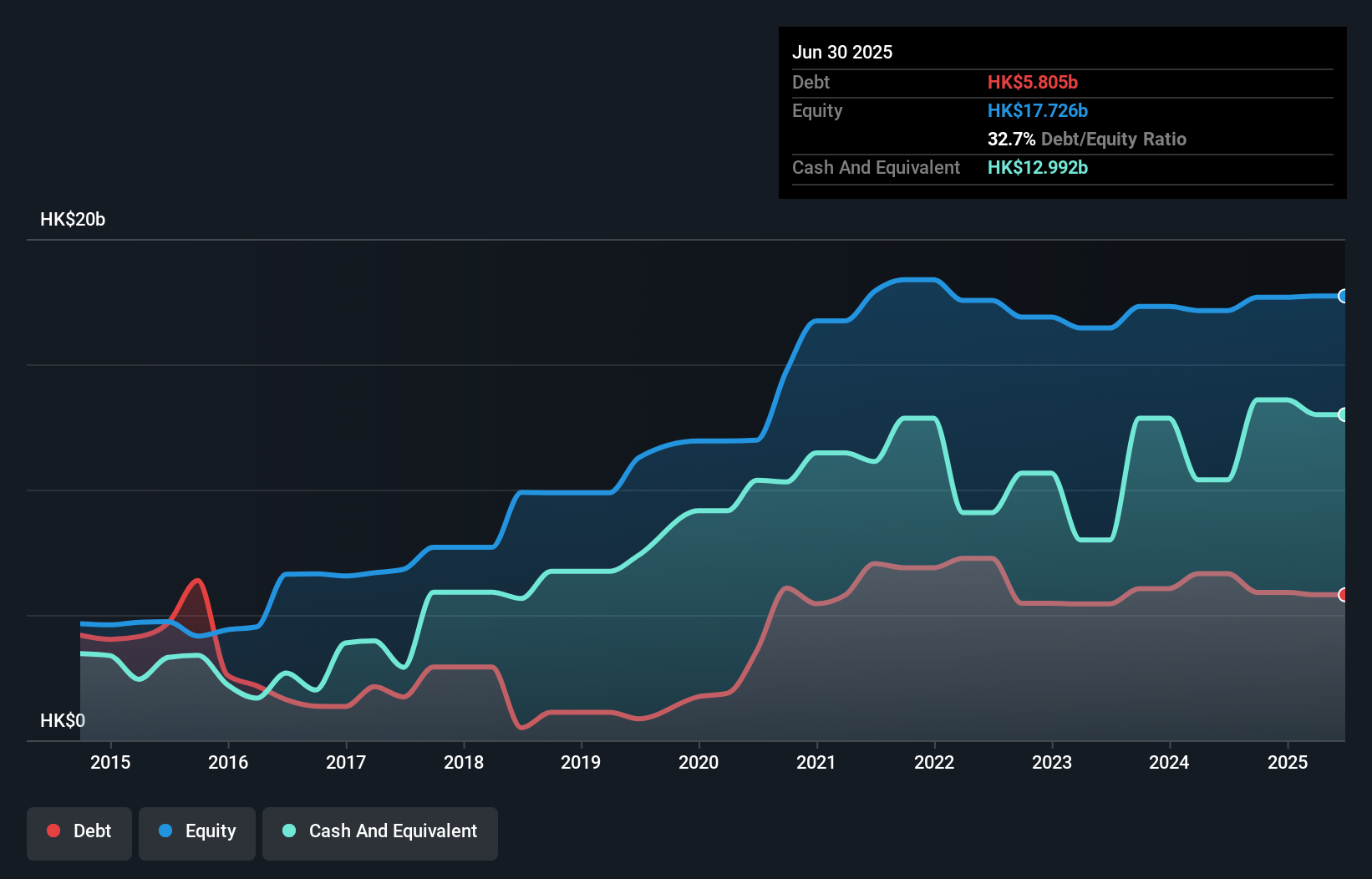

The image below, which you can click on for greater detail, shows that TCL Electronics Holdings had debt of HK$5.80b at the end of June 2025, a reduction from HK$6.65b over a year. But on the other hand it also has HK$13.0b in cash, leading to a HK$7.19b net cash position.

A Look At TCL Electronics Holdings' Liabilities

The latest balance sheet data shows that TCL Electronics Holdings had liabilities of HK$63.3b due within a year, and liabilities of HK$1.62b falling due after that. Offsetting this, it had HK$13.0b in cash and HK$26.3b in receivables that were due within 12 months. So its liabilities total HK$25.7b more than the combination of its cash and short-term receivables.

This deficit is considerable relative to its market capitalization of HK$26.3b, so it does suggest shareholders should keep an eye on TCL Electronics Holdings' use of debt. Should its lenders demand that it shore up the balance sheet, shareholders would likely face severe dilution. While it does have liabilities worth noting, TCL Electronics Holdings also has more cash than debt, so we're pretty confident it can manage its debt safely.

See our latest analysis for TCL Electronics Holdings

Better yet, TCL Electronics Holdings grew its EBIT by 147% last year, which is an impressive improvement. If maintained that growth will make the debt even more manageable in the years ahead. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine TCL Electronics Holdings's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. While TCL Electronics Holdings has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Happily for any shareholders, TCL Electronics Holdings actually produced more free cash flow than EBIT over the last two years. That sort of strong cash generation warms our hearts like a puppy in a bumblebee suit.

Summing Up

Although TCL Electronics Holdings's balance sheet isn't particularly strong, due to the total liabilities, it is clearly positive to see that it has net cash of HK$7.19b. And it impressed us with free cash flow of HK$1.7b, being 118% of its EBIT. So we are not troubled with TCL Electronics Holdings's debt use. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. Be aware that TCL Electronics Holdings is showing 2 warning signs in our investment analysis , you should know about...

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

Valuation is complex, but we're here to simplify it.

Discover if TCL Electronics Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1070

TCL Electronics Holdings

An investment holding company, operates as a consumer electronics company in Mainland China, Europe, North America, and internationally.

Excellent balance sheet, good value and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

100% Patient Improvement in trial puts this $16M Biotech on the radar

Fair Value US$5.30|72.3% undervalued

JO

Community Contributor

PayPal's Future Growth Through Venmo and Merchant Solutions

Fair Value US$105.25|35.0% undervalued

ZW

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$26.54|1.3% undervalued

BL

Community Contributor