- Hong Kong

- /

- Commercial Services

- /

- SEHK:6663

The Returns On Capital At IWS Group Holdings (HKG:6663) Don't Inspire Confidence

If we want to find a stock that could multiply over the long term, what are the underlying trends we should look for? Ideally, a business will show two trends; firstly a growing return on capital employed (ROCE) and secondly, an increasing amount of capital employed. Put simply, these types of businesses are compounding machines, meaning they are continually reinvesting their earnings at ever-higher rates of return. Having said that, from a first glance at IWS Group Holdings (HKG:6663) we aren't jumping out of our chairs at how returns are trending, but let's have a deeper look.

What Is Return On Capital Employed (ROCE)?

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. Analysts use this formula to calculate it for IWS Group Holdings:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

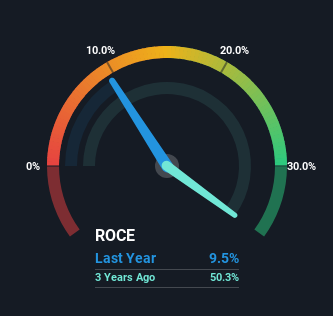

0.095 = HK$20m ÷ (HK$246m - HK$39m) (Based on the trailing twelve months to March 2023).

Thus, IWS Group Holdings has an ROCE of 9.5%. In absolute terms, that's a low return but it's around the Commercial Services industry average of 8.2%.

See our latest analysis for IWS Group Holdings

While the past is not representative of the future, it can be helpful to know how a company has performed historically, which is why we have this chart above. If you're interested in investigating IWS Group Holdings' past further, check out this free graph of past earnings, revenue and cash flow.

How Are Returns Trending?

On the surface, the trend of ROCE at IWS Group Holdings doesn't inspire confidence. Around five years ago the returns on capital were 48%, but since then they've fallen to 9.5%. Given the business is employing more capital while revenue has slipped, this is a bit concerning. If this were to continue, you might be looking at a company that is trying to reinvest for growth but is actually losing market share since sales haven't increased.

On a side note, IWS Group Holdings has done well to pay down its current liabilities to 16% of total assets. So we could link some of this to the decrease in ROCE. What's more, this can reduce some aspects of risk to the business because now the company's suppliers or short-term creditors are funding less of its operations. Some would claim this reduces the business' efficiency at generating ROCE since it is now funding more of the operations with its own money.

Our Take On IWS Group Holdings' ROCE

From the above analysis, we find it rather worrisome that returns on capital and sales for IWS Group Holdings have fallen, meanwhile the business is employing more capital than it was five years ago. Investors haven't taken kindly to these developments, since the stock has declined 14% from where it was three years ago. Unless there is a shift to a more positive trajectory in these metrics, we would look elsewhere.

One more thing, we've spotted 3 warning signs facing IWS Group Holdings that you might find interesting.

While IWS Group Holdings isn't earning the highest return, check out this free list of companies that are earning high returns on equity with solid balance sheets.

If you're looking to trade IWS Group Holdings, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:6663

IWS Group Holdings

A facility services company, provides security and facility management services to public and private sectors in Hong Kong.

Excellent balance sheet slight.