Advertisement

- Hong Kong

- /

- Commercial Services

- /

- SEHK:1855

We Think ZONQING Environmental Limited's (HKG:1855) CEO Compensation Looks Fair

Key Insights

- ZONQING Environmental to hold its Annual General Meeting on 14th of June

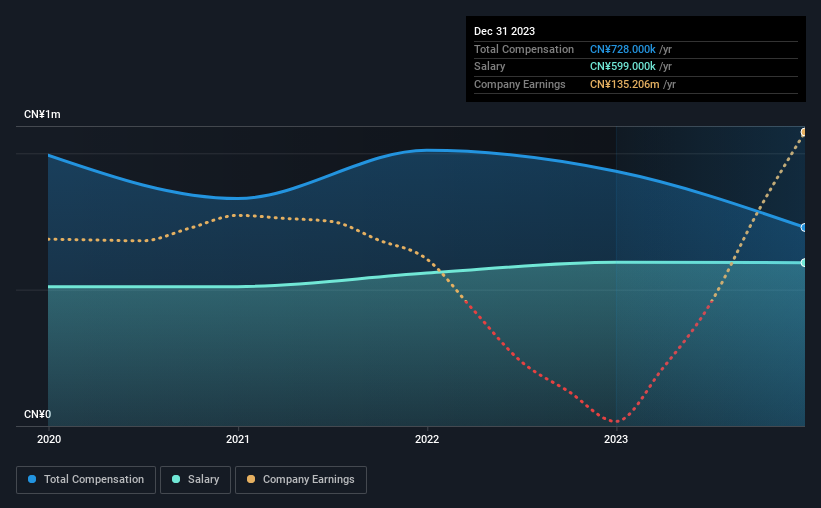

- Total pay for CEO Haitao Liu includes CN¥599.0k salary

- Total compensation is similar to the industry average

- ZONQING Environmental's EPS grew by 16% over the past three years while total shareholder return over the past three years was 1,229%

We have been pretty impressed with the performance at ZONQING Environmental Limited (HKG:1855) recently and CEO Haitao Liu deserves a mention for their role in it. The pleasing results would be something shareholders would keep in mind at the upcoming AGM on 14th of June. This would also be a chance for them to hear the board review the financial results, discuss future company strategy and vote on any resolutions such as executive remuneration. We think the CEO has done a pretty decent job and we discuss why the CEO compensation is appropriate.

View our latest analysis for ZONQING Environmental

How Does Total Compensation For Haitao Liu Compare With Other Companies In The Industry?

According to our data, ZONQING Environmental Limited has a market capitalization of HK$7.8b, and paid its CEO total annual compensation worth CN¥728k over the year to December 2023. We note that's a decrease of 22% compared to last year. In particular, the salary of CN¥599.0k, makes up a huge portion of the total compensation being paid to the CEO.

On comparing similar companies from the Hong Kong Commercial Services industry with market caps ranging from HK$3.1b to HK$12b, we found that the median CEO total compensation was CN¥976k. So it looks like ZONQING Environmental compensates Haitao Liu in line with the median for the industry.

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | CN¥599k | CN¥600k | 82% |

| Other | CN¥129k | CN¥334k | 18% |

| Total Compensation | CN¥728k | CN¥934k | 100% |

Speaking on an industry level, nearly 82% of total compensation represents salary, while the remainder of 18% is other remuneration. Our data reveals that ZONQING Environmental allocates salary more or less in line with the wider market. If salary dominates total compensation, it suggests that CEO compensation is leaning less towards the variable component, which is usually linked with performance.

ZONQING Environmental Limited's Growth

ZONQING Environmental Limited's earnings per share (EPS) grew 16% per year over the last three years. In the last year, its revenue is up 111%.

This demonstrates that the company has been improving recently and is good news for the shareholders. It's great to see that revenue growth is strong, too. These metrics suggest the business is growing strongly. Although we don't have analyst forecasts, you might want to assess this data-rich visualization of earnings, revenue and cash flow.

Has ZONQING Environmental Limited Been A Good Investment?

Most shareholders would probably be pleased with ZONQING Environmental Limited for providing a total return of 1,229% over three years. So they may not be at all concerned if the CEO were to be paid more than is normal for companies around the same size.

To Conclude...

Given the improved performance, shareholders may be more forgiving of CEO compensation in the upcoming AGM. Seeing that earnings growth and share price performance seems to be on the right path, the more pressing focus for shareholders at the AGM may be how the board and management plans to turn the company into a sustainably profitable one.

It is always advisable to analyse CEO pay, along with performing a thorough analysis of the company's key performance areas. In our study, we found 2 warning signs for ZONQING Environmental you should be aware of, and 1 of them is a bit unpleasant.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

Valuation is complex, but we're here to simplify it.

Discover if ZONQING Environmental might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1855

ZONQING Environmental

Engages in landscaping, ecological restoration, and other related activities in the People’s Republic of China.

Mediocre balance sheet with questionable track record.

Market Insights

Advertisement

Community Narratives

Apple: A Dying Star with an Overpriced Valuation

Fair Value US$177.34|20.1% overvalued

IN

Community Contributor

Avino a case for USD$20 per share within 5 years (assuming $3,500 gold, $100 silver and $4 copper).

Fair Value CA$26.79|87.5% undervalued

AG

Community Contributor

Riding the Defense Boom RENK Sees Revenue Climb at 15% CAGR by FY 2029

Fair Value €69.87|20.5% undervalued

CH

Community Contributor