Advertisement

- Hong Kong

- /

- Construction

- /

- SEHK:9893

Here's Why Pizu Group Holdings (HKG:9893) Can Manage Its Debt Responsibly

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. Importantly, Pizu Group Holdings Limited (HKG:9893) does carry debt. But the more important question is: how much risk is that debt creating?

When Is Debt Dangerous?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

How Much Debt Does Pizu Group Holdings Carry?

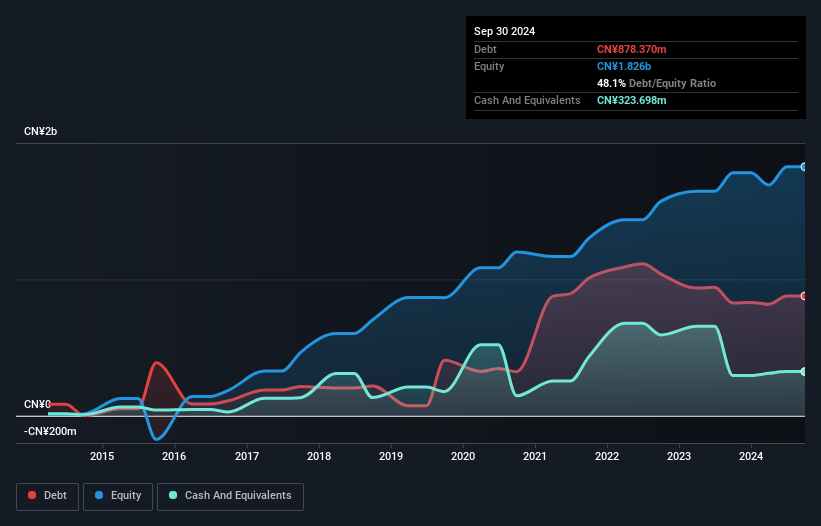

The image below, which you can click on for greater detail, shows that at September 2024 Pizu Group Holdings had debt of CN¥878.4m, up from CN¥826.8m in one year. However, it does have CN¥323.7m in cash offsetting this, leading to net debt of about CN¥554.7m.

How Strong Is Pizu Group Holdings' Balance Sheet?

We can see from the most recent balance sheet that Pizu Group Holdings had liabilities of CN¥1.75b falling due within a year, and liabilities of CN¥800.9m due beyond that. On the other hand, it had cash of CN¥323.7m and CN¥878.8m worth of receivables due within a year. So its liabilities total CN¥1.35b more than the combination of its cash and short-term receivables.

This is a mountain of leverage relative to its market capitalization of CN¥1.79b. This suggests shareholders would be heavily diluted if the company needed to shore up its balance sheet in a hurry.

See our latest analysis for Pizu Group Holdings

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Pizu Group Holdings's net debt is only 1.3 times its EBITDA. And its EBIT covers its interest expense a whopping 13.5 times over. So you could argue it is no more threatened by its debt than an elephant is by a mouse. On top of that, Pizu Group Holdings grew its EBIT by 45% over the last twelve months, and that growth will make it easier to handle its debt. When analysing debt levels, the balance sheet is the obvious place to start. But you can't view debt in total isolation; since Pizu Group Holdings will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So it's worth checking how much of that EBIT is backed by free cash flow. Looking at the most recent three years, Pizu Group Holdings recorded free cash flow of 46% of its EBIT, which is weaker than we'd expect. That's not great, when it comes to paying down debt.

Our View

The good news is that Pizu Group Holdings's demonstrated ability to cover its interest expense with its EBIT delights us like a fluffy puppy does a toddler. But, on a more sombre note, we are a little concerned by its level of total liabilities. All these things considered, it appears that Pizu Group Holdings can comfortably handle its current debt levels. On the plus side, this leverage can boost shareholder returns, but the potential downside is more risk of loss, so it's worth monitoring the balance sheet. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. For example, we've discovered 2 warning signs for Pizu Group Holdings (1 is a bit concerning!) that you should be aware of before investing here.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:9893

Pizu Group Holdings

An investment holding company, engages in the manufactures, trades, and sales of civil explosives in the People's Republic of China and Tajikistan.

Good value with proven track record.

Market Insights

Advertisement

Community Narratives

Scaling up in building materials with smart M&A and growing profitability

Fair Value US$2.77|30.0% undervalued

CM

Community Contributor

Hims: The Platform Powering Personalised Healthcare

Fair Value US$114.01|51.9% undervalued

BL

Community Contributor

Undervalued lottery company with strong fundamentals

Fair Value AU$15.00|34.5% undervalued

RO

Community Contributor

Proximus, transferring money from the impatient to the patient investor

Fair Value €16.62|55.1% undervalued

AX

Community Contributor