- Hong Kong

- /

- Electrical

- /

- SEHK:8328

These 4 Measures Indicate That Xinyi Electric Storage Holdings (HKG:8328) Is Using Debt Reasonably Well

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. Importantly, Xinyi Electric Storage Holdings Limited (HKG:8328) does carry debt. But is this debt a concern to shareholders?

When Is Debt A Problem?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company's debt levels is to consider its cash and debt together.

Check out our latest analysis for Xinyi Electric Storage Holdings

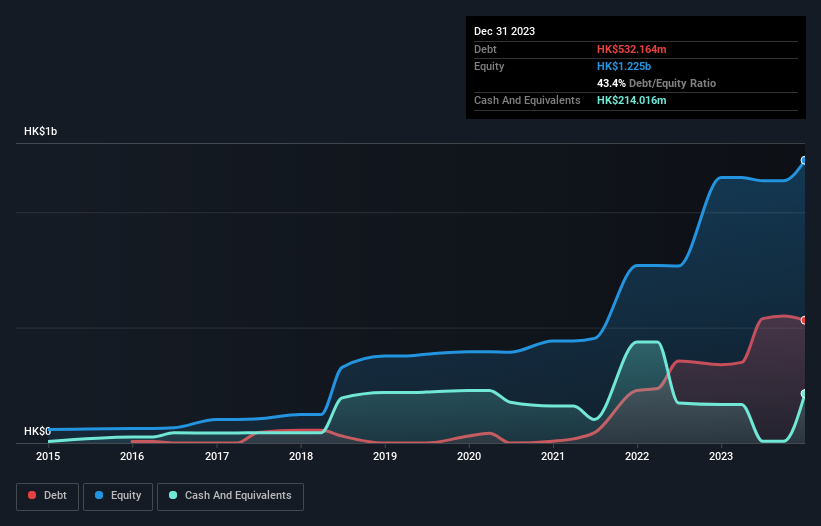

How Much Debt Does Xinyi Electric Storage Holdings Carry?

You can click the graphic below for the historical numbers, but it shows that as of December 2023 Xinyi Electric Storage Holdings had HK$532.2m of debt, an increase on HK$339.0m, over one year. However, because it has a cash reserve of HK$214.0m, its net debt is less, at about HK$318.1m.

A Look At Xinyi Electric Storage Holdings' Liabilities

According to the last reported balance sheet, Xinyi Electric Storage Holdings had liabilities of HK$907.4m due within 12 months, and liabilities of HK$200.7m due beyond 12 months. On the other hand, it had cash of HK$214.0m and HK$629.8m worth of receivables due within a year. So it has liabilities totalling HK$264.2m more than its cash and near-term receivables, combined.

Of course, Xinyi Electric Storage Holdings has a market capitalization of HK$1.33b, so these liabilities are probably manageable. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

With a debt to EBITDA ratio of 2.3, Xinyi Electric Storage Holdings uses debt artfully but responsibly. And the fact that its trailing twelve months of EBIT was 7.9 times its interest expenses harmonizes with that theme. It is well worth noting that Xinyi Electric Storage Holdings's EBIT shot up like bamboo after rain, gaining 51% in the last twelve months. That'll make it easier to manage its debt. There's no doubt that we learn most about debt from the balance sheet. But you can't view debt in total isolation; since Xinyi Electric Storage Holdings will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Over the last three years, Xinyi Electric Storage Holdings saw substantial negative free cash flow, in total. While that may be a result of expenditure for growth, it does make the debt far more risky.

Our View

Based on what we've seen Xinyi Electric Storage Holdings is not finding it easy, given its conversion of EBIT to free cash flow, but the other factors we considered give us cause to be optimistic. In particular, we are dazzled with its EBIT growth rate. Looking at all this data makes us feel a little cautious about Xinyi Electric Storage Holdings's debt levels. While debt does have its upside in higher potential returns, we think shareholders should definitely consider how debt levels might make the stock more risky. Over time, share prices tend to follow earnings per share, so if you're interested in Xinyi Electric Storage Holdings, you may well want to click here to check an interactive graph of its earnings per share history.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:8328

Xinyi Electric Storage Holdings

An investment holding company, engages in the energy storage, EPC services, automobile glass repair and replacement services, photovoltaic (PV) films, and other businesses in the People’s Republic of China, Hong Kong, Canada, Malaysia, and internationally.

Mediocre balance sheet and slightly overvalued.

Similar Companies

Market Insights

Community Narratives