Advertisement

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We note that Tong Kee (Holding) Limited (HKG:8305) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

See our latest analysis for Tong Kee (Holding)

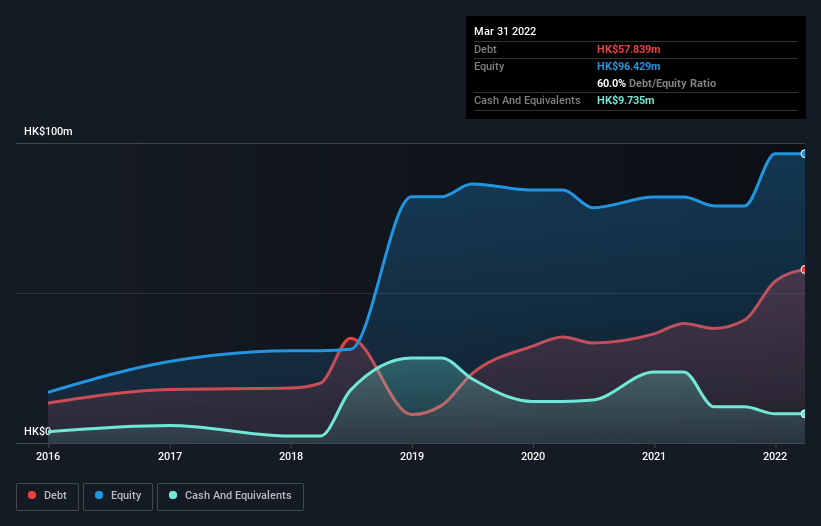

How Much Debt Does Tong Kee (Holding) Carry?

The image below, which you can click on for greater detail, shows that at December 2021 Tong Kee (Holding) had debt of HK$57.8m, up from HK$39.8m in one year. However, it also had HK$9.74m in cash, and so its net debt is HK$48.1m.

A Look At Tong Kee (Holding)'s Liabilities

According to the last reported balance sheet, Tong Kee (Holding) had liabilities of HK$137.9m due within 12 months, and liabilities of HK$1.25m due beyond 12 months. Offsetting this, it had HK$9.74m in cash and HK$154.0m in receivables that were due within 12 months. So it can boast HK$24.6m more liquid assets than total liabilities.

This short term liquidity is a sign that Tong Kee (Holding) could probably pay off its debt with ease, as its balance sheet is far from stretched. When analysing debt levels, the balance sheet is the obvious place to start. But it is Tong Kee (Holding)'s earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

In the last year Tong Kee (Holding)'s revenue was pretty flat, and it made a negative EBIT. While that's not too bad, we'd prefer see growth.

Caveat Emptor

Importantly, Tong Kee (Holding) had an earnings before interest and tax (EBIT) loss over the last year. Indeed, it lost HK$9.4m at the EBIT level. Looking on the brighter side, the business has adequate liquid assets, which give it time to grow and develop before its debt becomes a near-term issue. But we'd want to see some positive free cashflow before spending much time on trying to understand the stock. This one is a bit too risky for our liking. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. Case in point: We've spotted 4 warning signs for Tong Kee (Holding) you should be aware of, and 2 of them are concerning.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:8305

Sheng Tang Holdings

An investment holding company, operates as a multi-disciplinary contractor in the construction industry in Hong Kong.

Flawless balance sheet with low risk.

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|12.2% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|17.1% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.7% undervalued

TR

Community Contributor