- Hong Kong

- /

- Construction

- /

- SEHK:611

China Nuclear Energy Technology's (HKG:611) earnings trajectory could turn positive as the stock spikes 10% this past week

China Nuclear Energy Technology Corporation Limited (HKG:611) shareholders should be happy to see the share price up 12% in the last month. But that doesn't change the fact that the returns over the last three years have been disappointing. In that time, the share price dropped 57%. So it is really good to see an improvement. After all, could be that the fall was overdone.

The recent uptick of 10% could be a positive sign of things to come, so let's take a look at historical fundamentals.

View our latest analysis for China Nuclear Energy Technology

In his essay The Superinvestors of Graham-and-Doddsville Warren Buffett described how share prices do not always rationally reflect the value of a business. By comparing earnings per share (EPS) and share price changes over time, we can get a feel for how investor attitudes to a company have morphed over time.

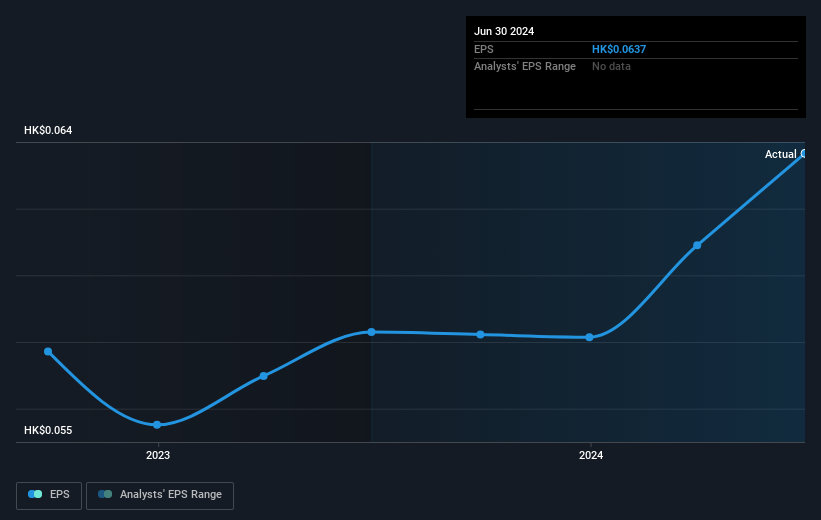

During the three years that the share price fell, China Nuclear Energy Technology's earnings per share (EPS) dropped by 1.4% each year. The share price decline of 25% is actually steeper than the EPS slippage. So it seems the market was too confident about the business, in the past. The less favorable sentiment is reflected in its current P/E ratio of 5.89.

The image below shows how EPS has tracked over time (if you click on the image you can see greater detail).

This free interactive report on China Nuclear Energy Technology's earnings, revenue and cash flow is a great place to start, if you want to investigate the stock further.

A Different Perspective

China Nuclear Energy Technology shareholders are up 32% for the year. But that was short of the market average. On the bright side, that's still a gain, and it's actually better than the average return of 5% over half a decade It is possible that returns will improve along with the business fundamentals. I find it very interesting to look at share price over the long term as a proxy for business performance. But to truly gain insight, we need to consider other information, too. Consider for instance, the ever-present spectre of investment risk. We've identified 3 warning signs with China Nuclear Energy Technology (at least 2 which make us uncomfortable) , and understanding them should be part of your investment process.

But note: China Nuclear Energy Technology may not be the best stock to buy. So take a peek at this free list of interesting companies with past earnings growth (and further growth forecast).

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on Hong Kong exchanges.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:611

China Nuclear Energy Technology

An investment holding company, provides engineering, procurement, and construction (EPC) services for photovoltaic power plants in the People’s Republic of China.

Proven track record low.

Market Insights

Community Narratives