Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We can see that Wai Kee Holdings Limited (HKG:610) does use debt in its business. But should shareholders be worried about its use of debt?

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

View our latest analysis for Wai Kee Holdings

What Is Wai Kee Holdings's Debt?

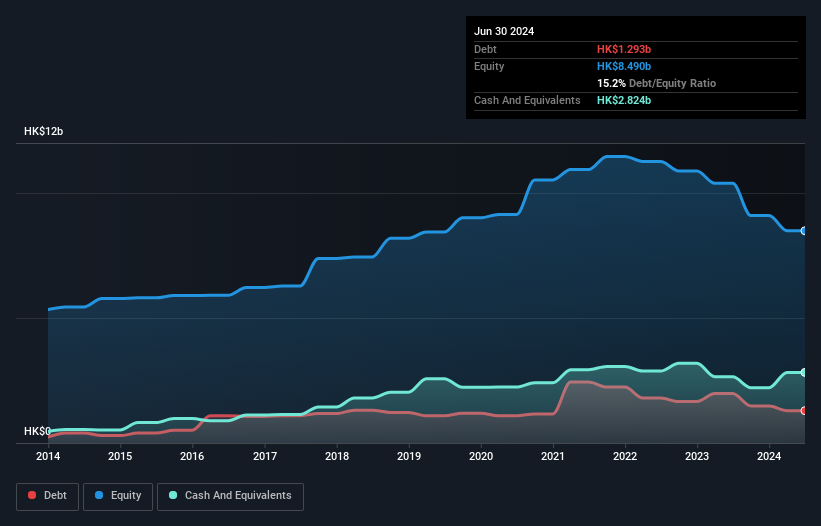

You can click the graphic below for the historical numbers, but it shows that Wai Kee Holdings had HK$1.29b of debt in June 2024, down from HK$1.98b, one year before. However, it does have HK$2.82b in cash offsetting this, leading to net cash of HK$1.53b.

How Healthy Is Wai Kee Holdings' Balance Sheet?

According to the last reported balance sheet, Wai Kee Holdings had liabilities of HK$6.31b due within 12 months, and liabilities of HK$199.1m due beyond 12 months. Offsetting these obligations, it had cash of HK$2.82b as well as receivables valued at HK$4.32b due within 12 months. So it actually has HK$635.3m more liquid assets than total liabilities.

This surplus liquidity suggests that Wai Kee Holdings' balance sheet could take a hit just as well as Homer Simpson's head can take a punch. On this view, lenders should feel as safe as the beloved of a black-belt karate master. Simply put, the fact that Wai Kee Holdings has more cash than debt is arguably a good indication that it can manage its debt safely.

But the bad news is that Wai Kee Holdings has seen its EBIT plunge 16% in the last twelve months. If that rate of decline in earnings continues, the company could find itself in a tight spot. The balance sheet is clearly the area to focus on when you are analysing debt. But you can't view debt in total isolation; since Wai Kee Holdings will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. While Wai Kee Holdings has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. In the last three years, Wai Kee Holdings's free cash flow amounted to 39% of its EBIT, less than we'd expect. That weak cash conversion makes it more difficult to handle indebtedness.

Summing Up

While we empathize with investors who find debt concerning, the bottom line is that Wai Kee Holdings has net cash of HK$1.53b and plenty of liquid assets. So is Wai Kee Holdings's debt a risk? It doesn't seem so to us. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. These risks can be hard to spot. Every company has them, and we've spotted 2 warning signs for Wai Kee Holdings (of which 1 is potentially serious!) you should know about.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

Valuation is complex, but we're here to simplify it.

Discover if Wai Kee Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:610

Wai Kee Holdings

An investment holding company, operates in the construction and infrastructure industries in Hong Kong and the People’s Republic of China.

Excellent balance sheet and good value.

Similar Companies

Market Insights

Community Narratives