- Hong Kong

- /

- Construction

- /

- SEHK:552

China Communications Services (SEHK:552) Appoints New President as Earnings Growth Outpaces Industry

Reviewed by Simply Wall St

China Communications Services (SEHK:552) is navigating a pivotal moment with the recent appointment of Mr. Cui Zhanwei as President, bringing over two decades of telecom management experience to the helm. Despite a promising earnings growth forecast and strategic market expansions, the company faces challenges such as a below-par Return on Equity and lagging revenue growth compared to the Hong Kong market. In the following discussion, we will explore the company's financial health, strategic initiatives, and the key risks and opportunities shaping its future trajectory.

Dive into the specifics of China Communications Services here with our thorough analysis report.

Innovative Factors Supporting China Communications Services

With a forecasted earnings growth of 6.01% annually, China Communications Services demonstrates strong financial health, further supported by a net profit margin improvement to 2.5%. The company's strategic initiatives, such as product innovation, have led to a 15% year-over-year revenue increase, significantly outperforming industry averages. This growth is bolstered by high-quality earnings and a solid cash position exceeding total debt. The recent appointment of Mr. Cui Zhanwei, with over 20 years of telecom management experience, as President, underscores the company's leadership strength. Explore the current health of China Communications Services and how it reflects on its financial stability and growth potential.

Vulnerabilities Impacting China Communications Services

Despite the promising growth, the company's Return on Equity at 8.5% remains below the desired threshold, highlighting potential inefficiencies. Revenue growth at 4.4% lags behind the Hong Kong market's 7.8%, suggesting room for improvement in market competitiveness. The volatility in dividend payments over the past decade further underscores financial unpredictability. These factors, coupled with the company's trading below its estimated fair value, suggest areas needing strategic focus. To gain deeper insights into China Communications Services's historical performance, explore our detailed analysis of past performance.

Future Prospects for China Communications Services in the Market

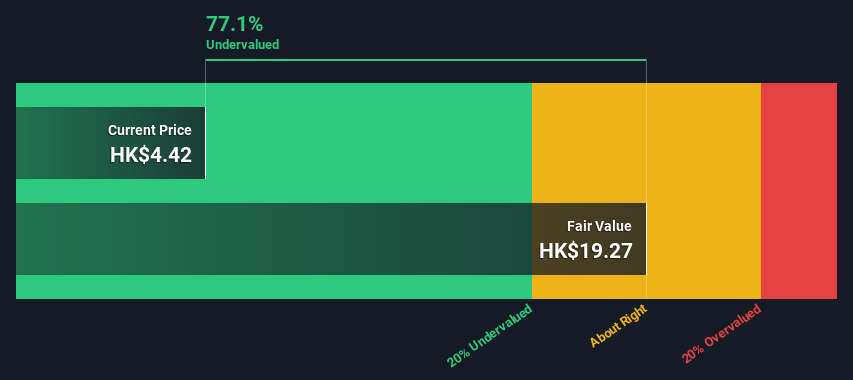

The company's significant undervaluation presents a potential opportunity for market repositioning, with its fair value estimated at HK$17.74 compared to the current HK$4.24. Expansion into new geographic markets is being explored, leveraging digital transformation to enhance customer engagement and operational efficiency. Regulatory changes offer additional avenues for growth, particularly in compliance-heavy industries. See what the latest analyst reports say about China Communications Services's future prospects and potential market movements.

Key Risks and Challenges That Could Impact China Communications Services's Success

Economic headwinds, such as inflationary pressures, pose risks to consumer spending and profitability. Supply chain disruptions continue to threaten production timelines, potentially affecting service delivery. Additionally, the company's unstable dividend track record may deter investor confidence, necessitating a focus on maintaining financial stability amidst regulatory changes. Learn about China Communications Services's dividend strategy and how it impacts shareholder returns and financial stability.

Conclusion

China Communications Services showcases promising financial health with a forecasted annual earnings growth of 6.01% and a net profit margin improvement to 2.5%, driven by strategic product innovations and strong leadership. However, challenges such as a Return on Equity of 8.5% and revenue growth lagging behind the Hong Kong market highlight areas for strategic enhancement. The company's current market valuation at HK$4.24, significantly below its estimated fair value of HK$17.74, suggests a potential opportunity for repositioning. Addressing economic headwinds and supply chain disruptions while stabilizing dividend payments will be crucial for sustaining investor confidence and capitalizing on future growth prospects.

Turning Ideas Into Actions

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Simply Wall St and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

About SEHK:552

China Communications Services

Provides telecommunications support services worldwide.

Solid track record with excellent balance sheet and pays a dividend.