Advertisement

- Hong Kong

- /

- Electrical

- /

- SEHK:3919

Golden Power Group Holdings (HKG:3919) Has Debt But No Earnings; Should You Worry?

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that Golden Power Group Holdings Limited (HKG:3919) does use debt in its business. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we think about a company's use of debt, we first look at cash and debt together.

Check out our latest analysis for Golden Power Group Holdings

What Is Golden Power Group Holdings's Net Debt?

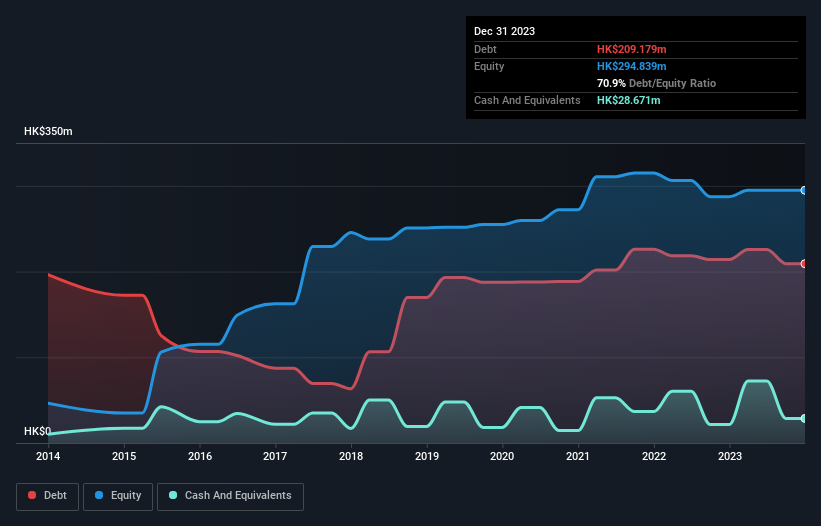

The chart below, which you can click on for greater detail, shows that Golden Power Group Holdings had HK$209.2m in debt in December 2023; about the same as the year before. However, it also had HK$28.7m in cash, and so its net debt is HK$180.5m.

How Strong Is Golden Power Group Holdings' Balance Sheet?

The latest balance sheet data shows that Golden Power Group Holdings had liabilities of HK$308.3m due within a year, and liabilities of HK$29.4m falling due after that. Offsetting these obligations, it had cash of HK$28.7m as well as receivables valued at HK$55.9m due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by HK$253.1m.

This deficit casts a shadow over the HK$31.3m company, like a colossus towering over mere mortals. So we'd watch its balance sheet closely, without a doubt. After all, Golden Power Group Holdings would likely require a major re-capitalisation if it had to pay its creditors today. When analysing debt levels, the balance sheet is the obvious place to start. But you can't view debt in total isolation; since Golden Power Group Holdings will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

In the last year Golden Power Group Holdings had a loss before interest and tax, and actually shrunk its revenue by 18%, to HK$270m. That's not what we would hope to see.

Caveat Emptor

While Golden Power Group Holdings's falling revenue is about as heartwarming as a wet blanket, arguably its earnings before interest and tax (EBIT) loss is even less appealing. To be specific the EBIT loss came in at HK$575k. When you combine this with the very significant balance sheet liabilities mentioned above, we are so wary of it that we are basically at a loss for the right words. Sure, the company might have a nice story about how they are going on to a brighter future. But the reality is that it is low on liquid assets relative to liabilities, and it burned through HK$1.5m in the last year. So we consider this a high risk stock, and we're worried its share price could sink faster than than a dingy with a great white shark attacking it. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. Be aware that Golden Power Group Holdings is showing 4 warning signs in our investment analysis , and 3 of those are potentially serious...

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:3919

Golden Power Group Holdings

An investment holding company, engages in the manufacture and sale batteries for various electronic devices in the People’s Republic of China, Hong Kong, and internationally.

Moderate and good value.

Market Insights

Advertisement

Community Narratives

Pole position to benefit from GENIUS Act

Fair Value US$233.04|59.1% undervalued

CH

Community Contributor

IREN will transform from bitcoin miner to leader in AI infrastructure

Fair Value US$21.48|15.5% undervalued

KA

Community Contributor

Behind the Assay: XRF Scientific’s Role in Modern Mining Economics

Fair Value AU$2.10|0% overvalued

RO

Community Contributor