Advertisement

- Hong Kong

- /

- Industrials

- /

- SEHK:267

New Forecasts: Here's What Analysts Think The Future Holds For CITIC Limited (HKG:267)

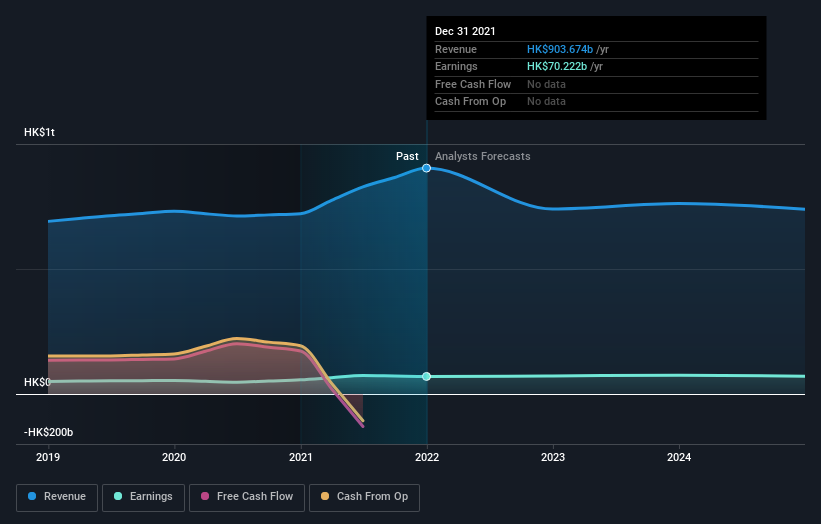

CITIC Limited (HKG:267) shareholders will have a reason to smile today, with the analysts making substantial upgrades to this year's statutory forecasts. The consensus estimated revenue numbers rose, with their view now clearly much more bullish on the company's business prospects.

Following the latest upgrade, the current consensus, from the six analysts covering CITIC, is for revenues of HK$740b in 2022, which would reflect a considerable 18% reduction in CITIC's sales over the past 12 months. Statutory earnings per share are presumed to rise 6.3% to HK$2.56. Prior to this update, the analysts had been forecasting revenues of HK$670b and earnings per share (EPS) of HK$2.43 in 2022. The most recent forecasts are noticeably more optimistic, with a solid increase in revenue estimates and a lift to earnings per share as well.

Check out our latest analysis for CITIC

Although the analysts have upgraded their earnings estimates, there was no change to the consensus price target of HK$9.94, suggesting that the forecast performance does not have a long term impact on the company's valuation. There's another way to think about price targets though, and that's to look at the range of price targets put forward by analysts, because a wide range of estimates could suggest a diverse view on possible outcomes for the business. The most optimistic CITIC analyst has a price target of HK$11.50 per share, while the most pessimistic values it at HK$7.40. These price targets show that analysts do have some differing views on the business, but the estimates do not vary enough to suggest to us that some are betting on wild success or utter failure.

Of course, another way to look at these forecasts is to place them into context against the industry itself. We would highlight that sales are expected to reverse, with a forecast 18% annualised revenue decline to the end of 2022. That is a notable change from historical growth of 9.5% over the last five years. By contrast, our data suggests that other companies (with analyst coverage) in the same industry are forecast to see their revenue grow 3.2% annually for the foreseeable future. So although its revenues are forecast to shrink, this cloud does not come with a silver lining - CITIC is expected to lag the wider industry.

The Bottom Line

The biggest takeaway for us from these new estimates is that analysts upgraded their earnings per share estimates, with improved earnings power expected for this year. Fortunately, they also upgraded their revenue estimates, and are forecasting revenues to grow slower than the wider market. Seeing the dramatic upgrade to this year's forecasts, it might be time to take another look at CITIC.

Using these estimates as a starting point, we've run a discounted cash flow calculation (DCF) on CITIC that suggests the company could be somewhat undervalued. For more information, you can click through to our platform to learn more about our valuation approach.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies that insiders are buying.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:267

CITIC

Operates in the financial services, advanced intelligent manufacturing, advanced materials, consumption, and urbanization businesses in the Mainland of China, Hong Kong, Macau, Taiwan, and internationally.

Good value average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|4.9% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|32.5% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$384.84|21.9% undervalued

BL

Community Contributor