Advertisement

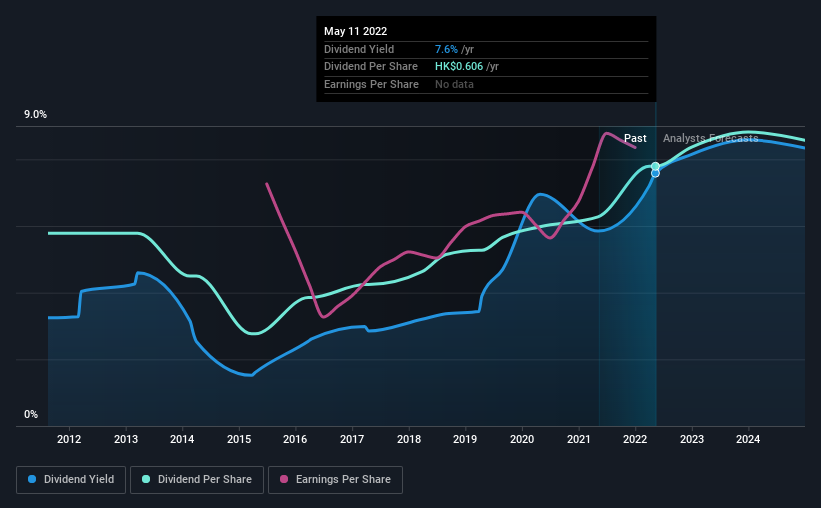

The board of CITIC Limited (HKG:267) has announced that it will be increasing its dividend on the 8th of August to HK$0.46. This will take the annual payment from 7.6% to 7.6% of the stock price, which is above what most companies in the industry pay.

Check out our latest analysis for CITIC

CITIC's Payment Has Solid Earnings Coverage

While it is great to have a strong dividend yield, we should also consider whether the payment is sustainable. CITIC is quite easily earning enough to cover the dividend, however it is being let down by weak cash flows. We think that cash flows should take priority over earnings, so this is definitely a worry for the dividend going forward.

Looking forward, earnings per share is forecast to rise by 6.1% over the next year. If the dividend continues on this path, the payout ratio could be 26% by next year, which we think can be pretty sustainable going forward.

Dividend Volatility

The company has a long dividend track record, but it doesn't look great with cuts in the past. Since 2012, the first annual payment was HK$0.45, compared to the most recent full-year payment of HK$0.61. This works out to be a compound annual growth rate (CAGR) of approximately 3.0% a year over that time. The dividend has seen some fluctuations in the past, so even though the dividend was raised this year, we should remember that it has been cut in the past.

The Dividend Looks Likely To Grow

With a relatively unstable dividend, it's even more important to evaluate if earnings per share is growing, which could point to a growing dividend in the future. We are encouraged to see that CITIC has grown earnings per share at 16% per year over the past five years. Growth in EPS bodes well for the dividend, as does the low payout ratio that the company is currently reporting.

In Summary

In summary, while it's always good to see the dividend being raised, we don't think CITIC's payments are rock solid. While the low payout ratio is redeeming feature, this is offset by the minimal cash to cover the payments. This company is not in the top tier of income providing stocks.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. However, there are other things to consider for investors when analysing stock performance. Just as an example, we've come across 2 warning signs for CITIC you should be aware of, and 1 of them is a bit concerning. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:267

CITIC

Operates in the financial services, advanced intelligent manufacturing, advanced materials, consumption, and urbanization businesses in the Mainland of China, Hong Kong, Macau, Taiwan, and internationally.

Good value average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

Quality at a Premium. A time to watch, not to buy?

Fair Value US$154.56|29.3% undervalued

DA

Community Contributor

GRAB: The Super-App at the Heart of Southeast Asia’s Digital Boom

Fair Value US$6.60|7.0% undervalued

BL

Community Contributor

Verve Group to Surge with 51.61% Revenue Growth

Fair Value €6.00|65.0% undervalued

ME

Community Contributor