- Hong Kong

- /

- Construction

- /

- SEHK:2132

Earnings Troubles May Signal Larger Issues for Landrich Holding (HKG:2132) Shareholders

Despite Landrich Holding Limited's (HKG:2132) most recent earnings report having soft headline numbers, its stock has had a positive performance. We looked at the details, and we think that investors may be responding to some encouraging factors.

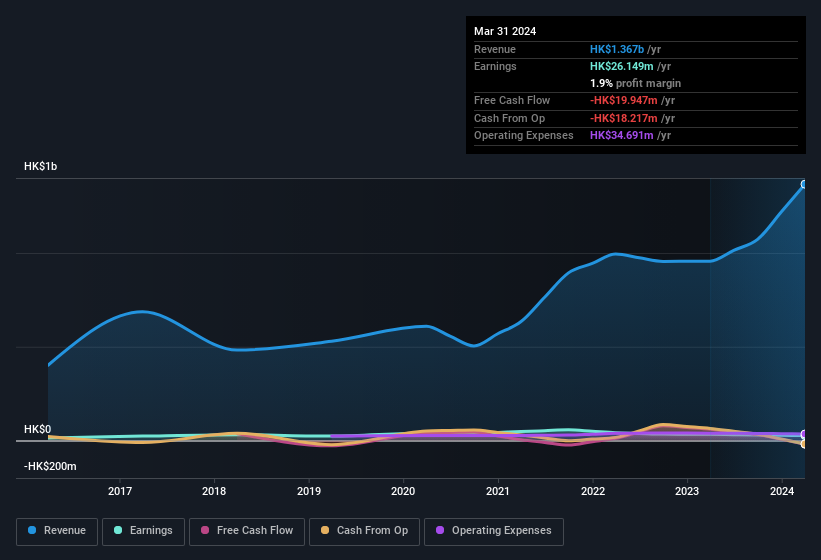

View our latest analysis for Landrich Holding

Zooming In On Landrich Holding's Earnings

As finance nerds would already know, the accrual ratio from cashflow is a key measure for assessing how well a company's free cash flow (FCF) matches its profit. In plain english, this ratio subtracts FCF from net profit, and divides that number by the company's average operating assets over that period. You could think of the accrual ratio from cashflow as the 'non-FCF profit ratio'.

That means a negative accrual ratio is a good thing, because it shows that the company is bringing in more free cash flow than its profit would suggest. That is not intended to imply we should worry about a positive accrual ratio, but it's worth noting where the accrual ratio is rather high. Notably, there is some academic evidence that suggests that a high accrual ratio is a bad sign for near-term profits, generally speaking.

For the year to March 2024, Landrich Holding had an accrual ratio of 0.29. Therefore, we know that it's free cashflow was significantly lower than its statutory profit, raising questions about how useful that profit figure really is. Even though it reported a profit of HK$26.1m, a look at free cash flow indicates it actually burnt through HK$20m in the last year. It's worth noting that Landrich Holding generated positive FCF of HK$60m a year ago, so at least they've done it in the past. However, that's not all there is to consider. The accrual ratio is reflecting the impact of unusual items on statutory profit, at least in part. The good news for shareholders is that Landrich Holding's accrual ratio was much better last year, so this year's poor reading might simply be a case of a short term mismatch between profit and FCF. As a result, some shareholders may be looking for stronger cash conversion in the current year.

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Landrich Holding.

The Impact Of Unusual Items On Profit

Landrich Holding's profit suffered from unusual items, which reduced profit by HK$13m in the last twelve months. If this was a non-cash charge, it would have made the accrual ratio better, if cashflow had stayed strong, so it's not great to see in combination with an uninspiring accrual ratio. While deductions due to unusual items are disappointing in the first instance, there is a silver lining. When we analysed the vast majority of listed companies worldwide, we found that significant unusual items are often not repeated. And that's hardly a surprise given these line items are considered unusual. If Landrich Holding doesn't see those unusual expenses repeat, then all else being equal we'd expect its profit to increase over the coming year.

Our Take On Landrich Holding's Profit Performance

Landrich Holding saw unusual items weigh on its profit, which should have made it easier to show high cash conversion, which it did not do, according to its accrual ratio. Based on these factors, it's hard to tell if Landrich Holding's profits are a reasonable reflection of its underlying profitability. If you want to do dive deeper into Landrich Holding, you'd also look into what risks it is currently facing. For instance, we've identified 5 warning signs for Landrich Holding (2 shouldn't be ignored) you should be familiar with.

In this article we've looked at a number of factors that can impair the utility of profit numbers, as a guide to a business. But there are plenty of other ways to inform your opinion of a company. Some people consider a high return on equity to be a good sign of a quality business. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks with significant insider holdings to be useful.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:2132

Landrich Holding

An investment holding company, provides construction engineering works in Hong Kong.

Excellent balance sheet moderate.

Market Insights

Community Narratives