Should You Be Adding Channel Micron Holdings (HKG:2115) To Your Watchlist Today?

It's common for many investors, especially those who are inexperienced, to buy shares in companies with a good story even if these companies are loss-making. But as Peter Lynch said in One Up On Wall Street, 'Long shots almost never pay off.' A loss-making company is yet to prove itself with profit, and eventually the inflow of external capital may dry up.

So if this idea of high risk and high reward doesn't suit, you might be more interested in profitable, growing companies, like Channel Micron Holdings (HKG:2115). While this doesn't necessarily speak to whether it's undervalued, the profitability of the business is enough to warrant some appreciation - especially if its growing.

See our latest analysis for Channel Micron Holdings

Channel Micron Holdings' Earnings Per Share Are Growing

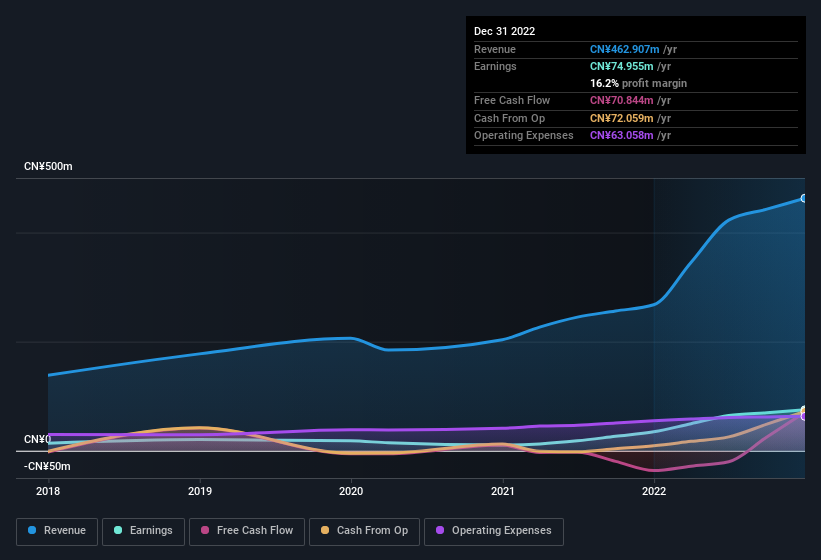

If you believe that markets are even vaguely efficient, then over the long term you'd expect a company's share price to follow its earnings per share (EPS) outcomes. That means EPS growth is considered a real positive by most successful long-term investors. To the delight of shareholders, Channel Micron Holdings has achieved impressive annual EPS growth of 46%, compound, over the last three years. That sort of growth rarely ever lasts long, but it is well worth paying attention to when it happens.

One way to double-check a company's growth is to look at how its revenue, and earnings before interest and tax (EBIT) margins are changing. Channel Micron Holdings shareholders can take confidence from the fact that EBIT margins are up from 15% to 19%, and revenue is growing. Ticking those two boxes is a good sign of growth, in our book.

You can take a look at the company's revenue and earnings growth trend, in the chart below. To see the actual numbers, click on the chart.

Channel Micron Holdings isn't a huge company, given its market capitalisation of HK$427m. That makes it extra important to check on its balance sheet strength.

Are Channel Micron Holdings Insiders Aligned With All Shareholders?

Investors are always searching for a vote of confidence in the companies they hold and insider buying is one of the key indicators for optimism on the market. Because often, the purchase of stock is a sign that the buyer views it as undervalued. However, small purchases are not always indicative of conviction, and insiders don't always get it right.

Any way you look at it Channel Micron Holdings shareholders can gain quiet confidence from the fact that insiders shelled out CN¥1.9m to buy stock, over the last year. This, combined with the lack of sales from insiders, should be a great signal for shareholders in what's to come. Zooming in, we can see that the biggest insider purchase was by Executive Chairman Yew Sum Ng for HK$138k worth of shares, at about HK$0.24 per share.

These recent buys aren't the only encouraging sign for shareholders, as a look at the shareholder registry for Channel Micron Holdings will reveal that insiders own a significant piece of the pie. Indeed, with a collective holding of 53%, company insiders are in control and have plenty of capital behind the venture. This makes it apparent they will be incentivised to plan for the long term - a positive for shareholders with a sit and hold strategy. To give you an idea, the value of insiders' holdings in the business are valued at CN¥228m at the current share price. So there's plenty there to keep them focused!

Should You Add Channel Micron Holdings To Your Watchlist?

Channel Micron Holdings' earnings per share growth have been climbing higher at an appreciable rate. To make matters even better, the company insiders who know the company best have put their faith in the its future and have been buying more stock. This quick rundown suggests that the business may be of good quality, and also at an inflection point, so maybe Channel Micron Holdings deserves timely attention. Still, you should learn about the 2 warning signs we've spotted with Channel Micron Holdings.

Keen growth investors love to see insider buying. Thankfully, Channel Micron Holdings isn't the only one. You can see a a free list of them here.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

If you're looking to trade CM Hi-Tech Cleanroom, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:2115

CM Hi-Tech Cleanroom

Through its subsidiaries, engages in the manufacture and sale of cleanroom wall and ceiling systems, and cleanroom equipment.

Adequate balance sheet low.

Market Insights

Community Narratives