CIMC Vehicles (Group)'s (HKG:1839) Returns On Capital Are Heading Higher

If you're looking for a multi-bagger, there's a few things to keep an eye out for. Firstly, we'd want to identify a growing return on capital employed (ROCE) and then alongside that, an ever-increasing base of capital employed. If you see this, it typically means it's a company with a great business model and plenty of profitable reinvestment opportunities. So when we looked at CIMC Vehicles (Group) (HKG:1839) and its trend of ROCE, we really liked what we saw.

What is Return On Capital Employed (ROCE)?

If you haven't worked with ROCE before, it measures the 'return' (pre-tax profit) a company generates from capital employed in its business. The formula for this calculation on CIMC Vehicles (Group) is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

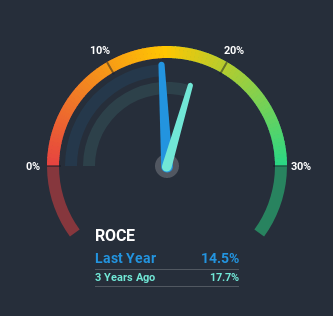

0.14 = CN¥1.6b ÷ (CN¥20b - CN¥8.6b) (Based on the trailing twelve months to December 2020).

Therefore, CIMC Vehicles (Group) has an ROCE of 14%. On its own, that's a standard return, however it's much better than the 8.5% generated by the Machinery industry.

See our latest analysis for CIMC Vehicles (Group)

In the above chart we have measured CIMC Vehicles (Group)'s prior ROCE against its prior performance, but the future is arguably more important. If you'd like, you can check out the forecasts from the analysts covering CIMC Vehicles (Group) here for free.

How Are Returns Trending?

CIMC Vehicles (Group) is displaying some positive trends. The numbers show that in the last four years, the returns generated on capital employed have grown considerably to 14%. The company is effectively making more money per dollar of capital used, and it's worth noting that the amount of capital has increased too, by 33%. This can indicate that there's plenty of opportunities to invest capital internally and at ever higher rates, a combination that's common among multi-baggers.

Another thing to note, CIMC Vehicles (Group) has a high ratio of current liabilities to total assets of 43%. This effectively means that suppliers (or short-term creditors) are funding a large portion of the business, so just be aware that this can introduce some elements of risk. Ideally we'd like to see this reduce as that would mean fewer obligations bearing risks.

In Conclusion...

In summary, it's great to see that CIMC Vehicles (Group) can compound returns by consistently reinvesting capital at increasing rates of return, because these are some of the key ingredients of those highly sought after multi-baggers. And investors seem to expect more of this going forward, since the stock has rewarded shareholders with a 14% return over the last year. In light of that, we think it's worth looking further into this stock because if CIMC Vehicles (Group) can keep these trends up, it could have a bright future ahead.

CIMC Vehicles (Group) does have some risks though, and we've spotted 2 warning signs for CIMC Vehicles (Group) that you might be interested in.

If you want to search for solid companies with great earnings, check out this free list of companies with good balance sheets and impressive returns on equity.

If you decide to trade CIMC Vehicles (Group), use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

If you're looking to trade CIMC Vehicles (Group), open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SEHK:1839

CIMC Vehicles (Group)

Designs, develops, produces, and sells specialty vehicles, semi-trailers, spare parts, and related technical services in China.

Flawless balance sheet with solid track record.

Similar Companies

Market Insights

Community Narratives