Advertisement

- Taiwan

- /

- Real Estate

- /

- TWSE:1436

Metallurgical Corporation of China And 2 Other High-Yield Dividend Stocks

Simply Wall St

Reviewed by Simply Wall St

As global markets navigate a landscape of easing inflation and strong earnings reports, investors are witnessing significant rebounds across major indices, with value stocks particularly outperforming growth shares. Amid this backdrop, dividend stocks remain an attractive option for those seeking steady income streams in a fluctuating market environment.

Top 10 Dividend Stocks

| Name | Dividend Yield | Dividend Rating |

| Peoples Bancorp (NasdaqGS:PEBO) | 5.11% | ★★★★★★ |

| Tsubakimoto Chain (TSE:6371) | 4.32% | ★★★★★★ |

| Guaranty Trust Holding (NGSE:GTCO) | 6.38% | ★★★★★★ |

| CAC Holdings (TSE:4725) | 4.68% | ★★★★★★ |

| Southside Bancshares (NYSE:SBSI) | 4.49% | ★★★★★★ |

| Yamato Kogyo (TSE:5444) | 4.03% | ★★★★★★ |

| Padma Oil (DSE:PADMAOIL) | 7.47% | ★★★★★★ |

| GakkyushaLtd (TSE:9769) | 4.45% | ★★★★★★ |

| E J Holdings (TSE:2153) | 4.02% | ★★★★★★ |

| DoshishaLtd (TSE:7483) | 3.97% | ★★★★★★ |

Click here to see the full list of 1975 stocks from our Top Dividend Stocks screener.

We're going to check out a few of the best picks from our screener tool.

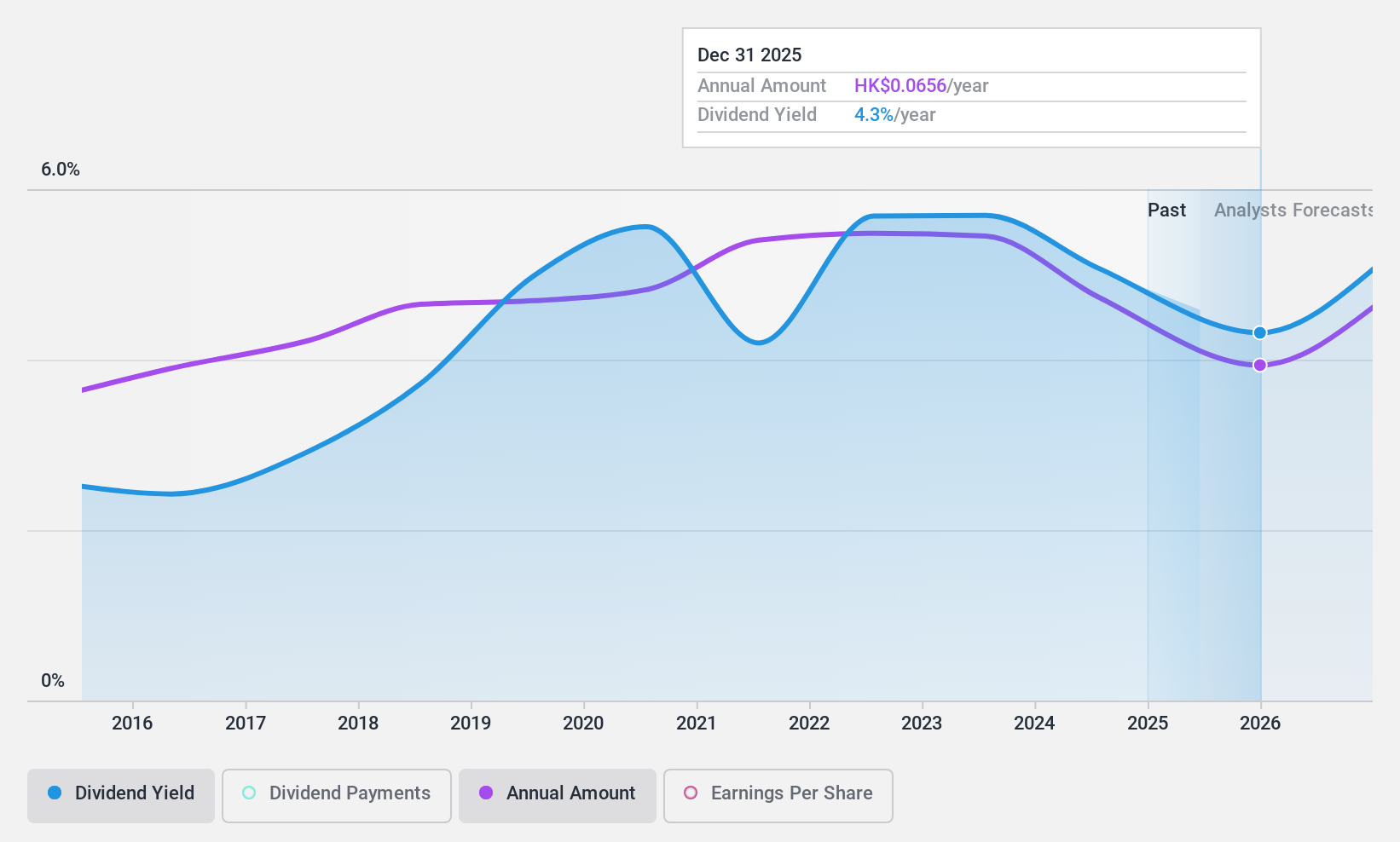

Metallurgical Corporation of China (SEHK:1618)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Metallurgical Corporation of China Ltd., with a market cap of HK$63.77 billion, operates in engineering contracting, resource development, specialty businesses, integrated real estate, and other sectors in China.

Operations: Metallurgical Corporation of China Ltd.'s revenue segments include engineering contracting, resource development, specialty businesses, and integrated real estate.

Dividend Yield: 4.9%

Metallurgical Corporation of China offers stable dividend payments with a low payout ratio of 29%, indicating earnings comfortably cover dividends. However, the dividend yield of 4.92% is below the top tier in Hong Kong, and free cash flow does not cover these payouts, raising sustainability concerns. Despite a recent decline in profit margins and contract value, the company maintains consistent dividend growth over ten years. Recent board changes may influence strategic directions impacting future dividends.

- Dive into the specifics of Metallurgical Corporation of China here with our thorough dividend report.

- Our valuation report unveils the possibility Metallurgical Corporation of China's shares may be trading at a discount.

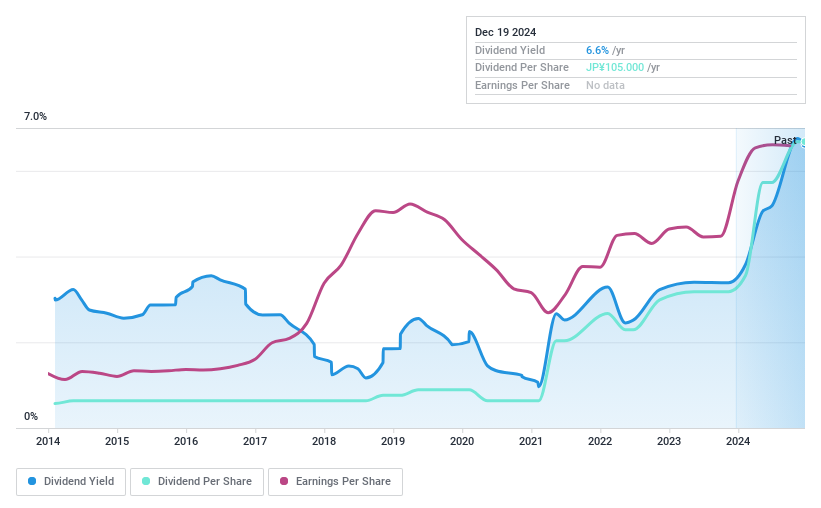

Yotai Refractories (TSE:5357)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Yotai Refractories Co., Ltd. is involved in the manufacture and sale of refractories and new ceramics, along with related engineering services in Japan, with a market cap of ¥29.58 billion.

Operations: Yotai Refractories Co., Ltd. generates revenue from its Refractory segment, amounting to ¥24.43 billion, and its Engineering segment, contributing ¥5.03 billion.

Dividend Yield: 6.3%

Yotai Refractories' dividend yield of 6.3% ranks in the top 25% of Japan's market, but its sustainability is questionable due to a high cash payout ratio of 257.2%. While dividends have grown over the past decade, they remain volatile and unreliable. Recent share buybacks totaling ¥560.04 million aim to enhance shareholder returns amidst lowered earnings guidance for fiscal year-end March 2025, suggesting a cautious approach to future dividend stability.

- Click here to discover the nuances of Yotai Refractories with our detailed analytical dividend report.

- The valuation report we've compiled suggests that Yotai Refractories' current price could be quite moderate.

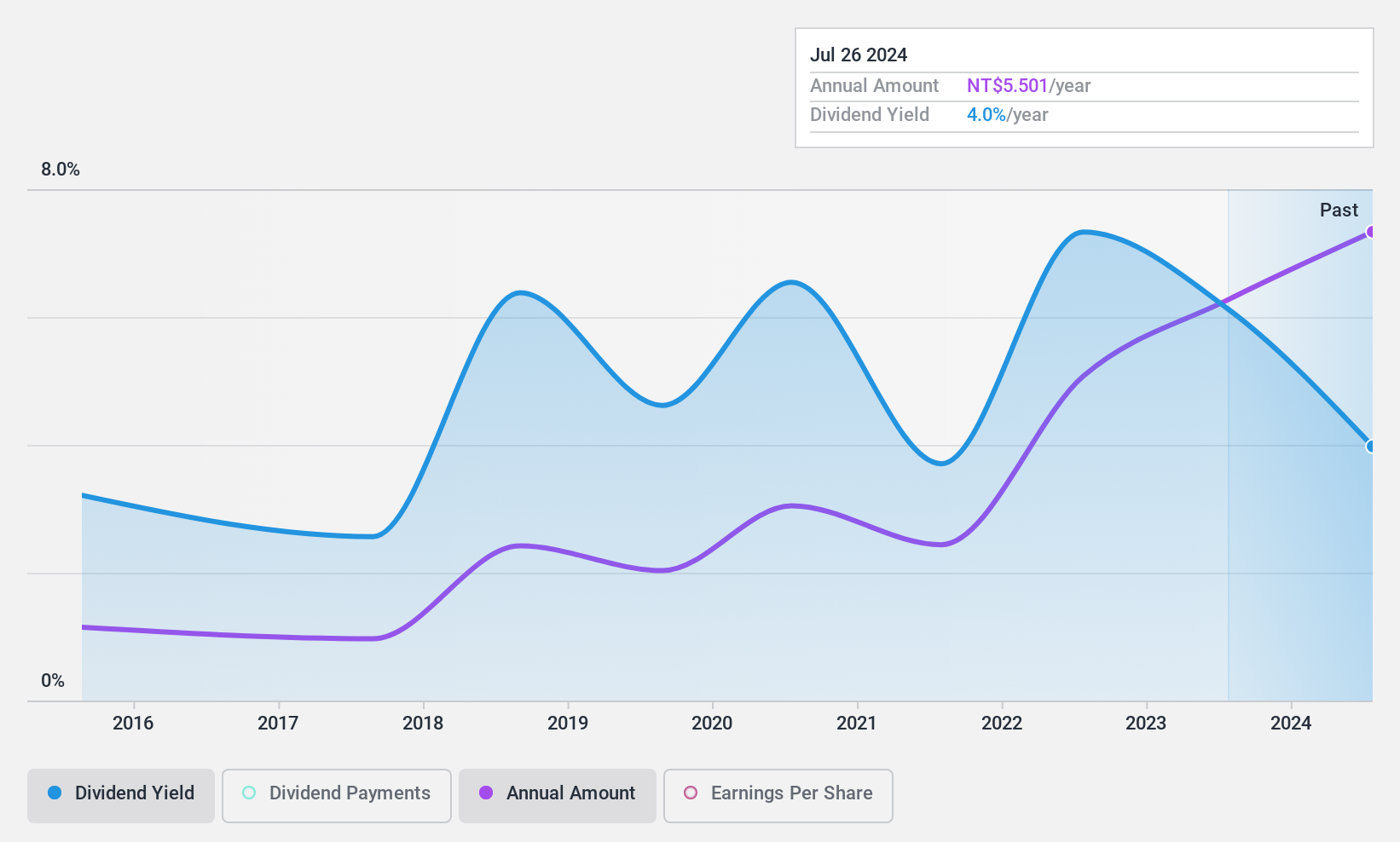

Hua Yu Lien Development (TWSE:1436)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Hua Yu Lien Development Co., Ltd. operates in the real estate sector in Taiwan with a market capitalization of NT$14.75 billion.

Operations: Hua Yu Lien Development Co., Ltd.'s revenue is primarily derived from the Construction Sector, contributing NT$7.46 billion, and the Engineering Department, contributing NT$643.99 million.

Dividend Yield: 4.6%

Hua Yu Lien Development's dividend yield of 4.64% is among the top 25% in Taiwan, yet its sustainability is challenged by a high cash payout ratio of 97.1%. Despite impressive recent earnings growth, dividends have been volatile over the past decade. The company's strategic expansion through a TWD 3 billion investment in new subsidiaries and a joint venture with Mitsui Fudosan Taiwan may impact future dividend stability and financial positioning.

- Unlock comprehensive insights into our analysis of Hua Yu Lien Development stock in this dividend report.

- The analysis detailed in our Hua Yu Lien Development valuation report hints at an inflated share price compared to its estimated value.

Turning Ideas Into Actions

- Dive into all 1975 of the Top Dividend Stocks we have identified here.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Hua Yu Lien Development might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TWSE:1436

Good value with proven track record and pays a dividend.

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|26.1% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|4.2% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|27.0% undervalued

KA

Community Contributor