Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We note that China Tianbao Group Development Company Limited (HKG:1427) does have debt on its balance sheet. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we examine debt levels, we first consider both cash and debt levels, together.

Our analysis indicates that 1427 is potentially overvalued!

What Is China Tianbao Group Development's Net Debt?

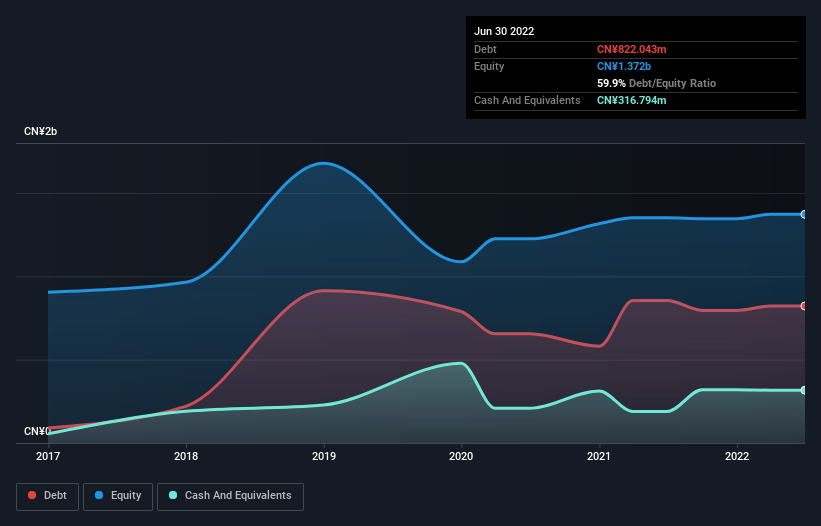

As you can see below, China Tianbao Group Development had CN¥822.0m of debt, at June 2022, which is about the same as the year before. You can click the chart for greater detail. However, because it has a cash reserve of CN¥316.8m, its net debt is less, at about CN¥505.2m.

How Strong Is China Tianbao Group Development's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that China Tianbao Group Development had liabilities of CN¥5.44b due within 12 months and liabilities of CN¥169.7m due beyond that. Offsetting these obligations, it had cash of CN¥316.8m as well as receivables valued at CN¥2.30b due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by CN¥3.00b.

Given this deficit is actually higher than the company's market capitalization of CN¥2.12b, we think shareholders really should watch China Tianbao Group Development's debt levels, like a parent watching their child ride a bike for the first time. Hypothetically, extremely heavy dilution would be required if the company were forced to pay down its liabilities by raising capital at the current share price.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

While we wouldn't worry about China Tianbao Group Development's net debt to EBITDA ratio of 4.4, we think its super-low interest cover of 2.0 times is a sign of high leverage. So shareholders should probably be aware that interest expenses appear to have really impacted the business lately. Worse, China Tianbao Group Development's EBIT was down 69% over the last year. If earnings continue to follow that trajectory, paying off that debt load will be harder than convincing us to run a marathon in the rain. The balance sheet is clearly the area to focus on when you are analysing debt. But it is China Tianbao Group Development's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. In the last three years, China Tianbao Group Development's free cash flow amounted to 40% of its EBIT, less than we'd expect. That weak cash conversion makes it more difficult to handle indebtedness.

Our View

To be frank both China Tianbao Group Development's level of total liabilities and its track record of (not) growing its EBIT make us rather uncomfortable with its debt levels. Having said that, its ability to convert EBIT to free cash flow isn't such a worry. After considering the datapoints discussed, we think China Tianbao Group Development has too much debt. That sort of riskiness is ok for some, but it certainly doesn't float our boat. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. Case in point: We've spotted 1 warning sign for China Tianbao Group Development you should be aware of.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1427

China Tianbao Group Development

Operates as a property developer and construction company in the People's Republic of China.

Slight and slightly overvalued.

Market Insights

Community Narratives