- Hong Kong

- /

- Construction

- /

- SEHK:1220

We Think Zhidao International (Holdings) (HKG:1220) Can Stay On Top Of Its Debt

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, Zhidao International (Holdings) Limited (HKG:1220) does carry debt. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

View our latest analysis for Zhidao International (Holdings)

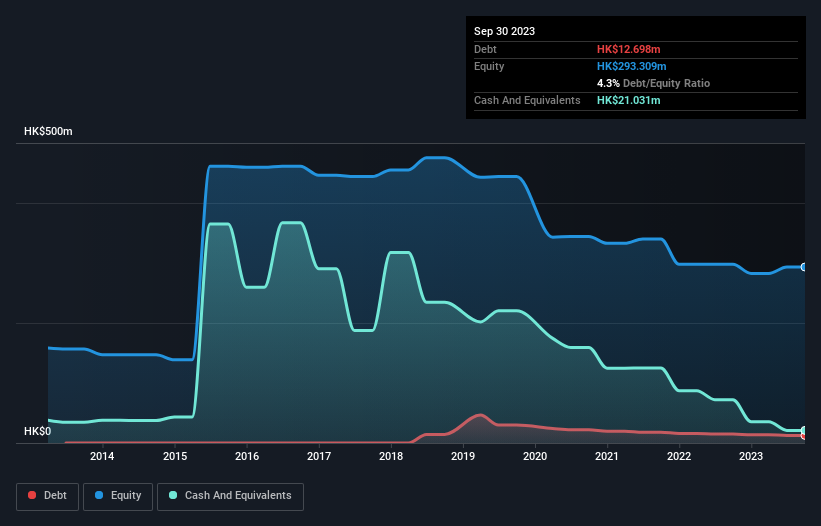

What Is Zhidao International (Holdings)'s Net Debt?

As you can see below, Zhidao International (Holdings) had HK$12.7m of debt at September 2023, down from HK$14.8m a year prior. But it also has HK$21.0m in cash to offset that, meaning it has HK$8.33m net cash.

How Strong Is Zhidao International (Holdings)'s Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Zhidao International (Holdings) had liabilities of HK$237.7m due within 12 months and liabilities of HK$4.15m due beyond that. On the other hand, it had cash of HK$21.0m and HK$389.7m worth of receivables due within a year. So it can boast HK$168.9m more liquid assets than total liabilities.

This luscious liquidity implies that Zhidao International (Holdings)'s balance sheet is sturdy like a giant sequoia tree. Having regard to this fact, we think its balance sheet is as strong as an ox. Succinctly put, Zhidao International (Holdings) boasts net cash, so it's fair to say it does not have a heavy debt load!

Although Zhidao International (Holdings) made a loss at the EBIT level, last year, it was also good to see that it generated HK$14m in EBIT over the last twelve months. The balance sheet is clearly the area to focus on when you are analysing debt. But you can't view debt in total isolation; since Zhidao International (Holdings) will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. While Zhidao International (Holdings) has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Over the last year, Zhidao International (Holdings) saw substantial negative free cash flow, in total. While investors are no doubt expecting a reversal of that situation in due course, it clearly does mean its use of debt is more risky.

Summing Up

While we empathize with investors who find debt concerning, the bottom line is that Zhidao International (Holdings) has net cash of HK$8.33m and plenty of liquid assets. So we don't have any problem with Zhidao International (Holdings)'s use of debt. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. We've identified 3 warning signs with Zhidao International (Holdings) (at least 2 which are significant) , and understanding them should be part of your investment process.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

Valuation is complex, but we're here to simplify it.

Discover if Zhidao International (Holdings) might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1220

Zhidao International (Holdings)

An investment holding company, provides construction and engineering services in Hong Kong and Macau.

Flawless balance sheet slight.

Market Insights

Community Narratives