- Hong Kong

- /

- Auto Components

- /

- SEHK:1571

Does It Make Sense To Buy Xin Point Holdings Limited (HKG:1571) For Its Yield?

Could Xin Point Holdings Limited (HKG:1571) be an attractive dividend share to own for the long haul? Investors are often drawn to strong companies with the idea of reinvesting the dividends. Unfortunately, it's common for investors to be enticed in by the seemingly attractive yield, and lose money when the company has to cut its dividend payments.

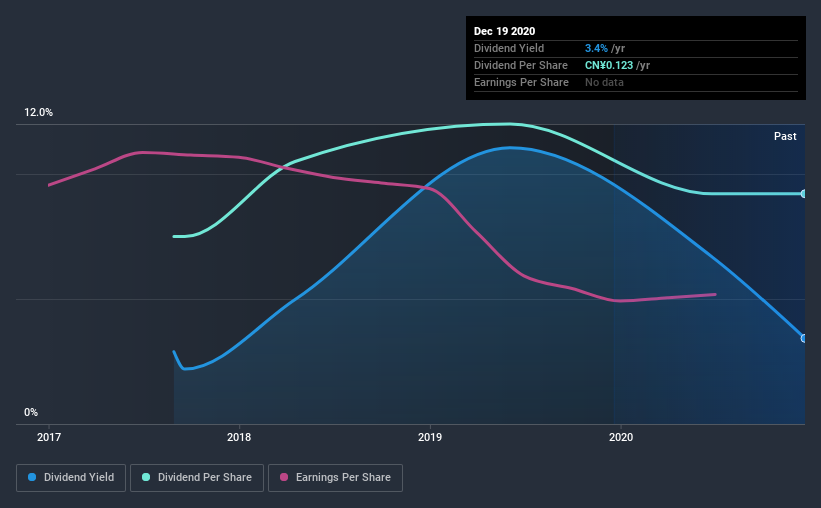

Xin Point Holdings pays a 3.4% dividend yield, and has been paying dividends for the past three years. It's certainly an attractive yield, but readers are likely curious about its staying power. Remember though, due to the recent spike in its share price, Xin Point Holdings's yield will look lower, even though the market may now be factoring in an improvement in its long-term prospects. Some simple analysis can reduce the risk of holding Xin Point Holdings for its dividend, and we'll focus on the most important aspects below.

Explore this interactive chart for our latest analysis on Xin Point Holdings!

Payout ratios

Companies (usually) pay dividends out of their earnings. If a company is paying more than it earns, the dividend might have to be cut. So we need to form a view on if a company's dividend is sustainable, relative to its net profit after tax. Xin Point Holdings paid out 58% of its profit as dividends, over the trailing twelve month period. This is a fairly normal payout ratio among most businesses. It allows a higher dividend to be paid to shareholders, but does limit the capital retained in the business - which could be good or bad.

We also measure dividends paid against a company's levered free cash flow, to see if enough cash was generated to cover the dividend. Xin Point Holdings paid out 69% of its cash flow as dividends last year, which is within a reasonable range for the average corporation. It's positive to see that Xin Point Holdings' dividend is covered by both profits and cash flow, since this is generally a sign that the dividend is sustainable, and a lower payout ratio usually suggests a greater margin of safety before the dividend gets cut.

While the above analysis focuses on dividends relative to a company's earnings, we do note Xin Point Holdings' strong net cash position, which will let it pay larger dividends for a time, should it choose.

We update our data on Xin Point Holdings every 24 hours, so you can always get our latest analysis of its financial health, here.

Dividend Volatility

From the perspective of an income investor who wants to earn dividends for many years, there is not much point buying a stock if its dividend is regularly cut or is not reliable. This company's dividend has been unstable, and with a relatively short history, we think it's a little soon to draw strong conclusions about its long term dividend potential. During the past three-year period, the first annual payment was CN¥0.1 in 2017, compared to CN¥0.1 last year. This works out to be a compound annual growth rate (CAGR) of approximately 7.1% a year over that time. The dividends haven't grown at precisely 7.1% every year, but this is a useful way to average out the historical rate of growth.

A reasonable rate of dividend growth is good to see, but we're wary that the dividend history is not as solid as we'd like, having been cut at least once.

Dividend Growth Potential

Given that the dividend has been cut in the past, we need to check if earnings are growing and if that might lead to stronger dividends in the future. Xin Point Holdings' EPS have fallen by approximately 22% per year during the past three years. A sharp decline in earnings per share is not great from from a dividend perspective, as even conservative payout ratios can come under pressure if earnings fall far enough.

Conclusion

To summarise, shareholders should always check that Xin Point Holdings' dividends are affordable, that its dividend payments are relatively stable, and that it has decent prospects for growing its earnings and dividend. Xin Point Holdings' is paying out more than half its income as dividends, but at least the dividend is covered by both reported earnings and cashflow. Earnings per share have been falling, and the company has cut its dividend at least once in the past. From a dividend perspective, this is a cause for concern. With this information in mind, we think Xin Point Holdings may not be an ideal dividend stock.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. To that end, Xin Point Holdings has 3 warning signs (and 1 which can't be ignored) we think you should know about.

We have also put together a list of global stocks with a market capitalisation above $1bn and yielding more 3%.

If you’re looking to trade Xin Point Holdings, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About SEHK:1571

Xin Point Holdings

An investment holding company, manufactures and sells automotive and electronic components in China, North America, Europe, and internationally.

Undervalued with solid track record.