Advertisement

We Don’t Think Euroconsultants' (ATH:EUROC) Earnings Should Make Shareholders Too Comfortable

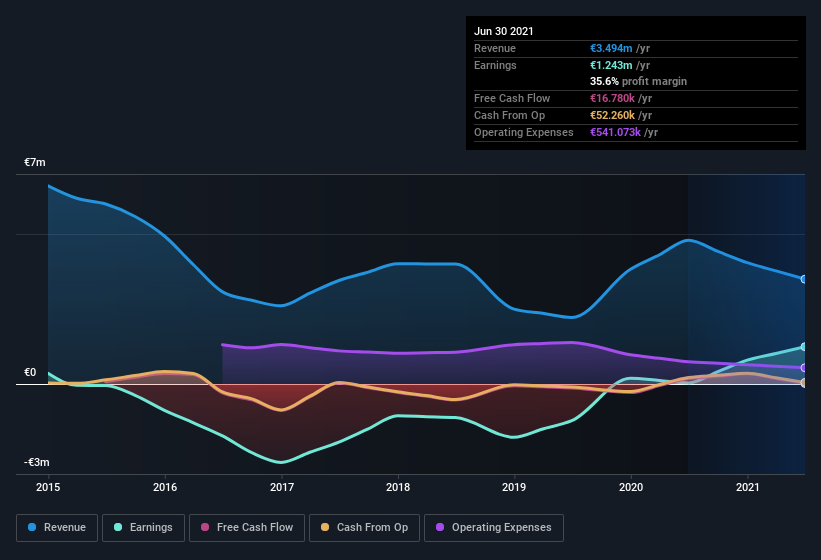

Euroconsultants SA's (ATH:EUROC) stock performed strongly after the recent earnings report. However, we think that investors should be cautious when interpreting the profit numbers.

Check out our latest analysis for Euroconsultants

Examining Cashflow Against Euroconsultants' Earnings

One key financial ratio used to measure how well a company converts its profit to free cash flow (FCF) is the accrual ratio. To get the accrual ratio we first subtract FCF from profit for a period, and then divide that number by the average operating assets for the period. You could think of the accrual ratio from cashflow as the 'non-FCF profit ratio'.

As a result, a negative accrual ratio is a positive for the company, and a positive accrual ratio is a negative. While having an accrual ratio above zero is of little concern, we do think it's worth noting when a company has a relatively high accrual ratio. Notably, there is some academic evidence that suggests that a high accrual ratio is a bad sign for near-term profits, generally speaking.

Over the twelve months to June 2021, Euroconsultants recorded an accrual ratio of 0.95. That means it didn't generate anywhere near enough free cash flow to match its profit. Statistically speaking, that's a real negative for future earnings. To wit, it produced free cash flow of €17k during the period, falling well short of its reported profit of €1.24m. Euroconsultants shareholders will no doubt be hoping that its free cash flow bounces back next year, since it was down over the last twelve months. Having said that, there is more to the story. The accrual ratio is reflecting the impact of unusual items on statutory profit, at least in part. One positive for Euroconsultants shareholders is that it's accrual ratio was significantly better last year, providing reason to believe that it may return to stronger cash conversion in the future. Shareholders should look for improved cashflow relative to profit in the current year, if that is indeed the case.

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Euroconsultants.

How Do Unusual Items Influence Profit?

The fact that the company had unusual items boosting profit by €651k, in the last year, probably goes some way to explain why its accrual ratio was so weak. While it's always nice to have higher profit, a large contribution from unusual items sometimes dampens our enthusiasm. When we crunched the numbers on thousands of publicly listed companies, we found that a boost from unusual items in a given year is often not repeated the next year. Which is hardly surprising, given the name. Euroconsultants had a rather significant contribution from unusual items relative to its profit to June 2021. As a result, we can surmise that the unusual items are making its statutory profit significantly stronger than it would otherwise be.

Our Take On Euroconsultants' Profit Performance

Euroconsultants had a weak accrual ratio, but its profit did receive a boost from unusual items. On reflection, the above-mentioned factors give us the strong impression that Euroconsultants'underlying earnings power is not as good as it might seem, based on the statutory profit numbers. If you'd like to know more about Euroconsultants as a business, it's important to be aware of any risks it's facing. To help with this, we've discovered 4 warning signs (3 can't be ignored!) that you ought to be aware of before buying any shares in Euroconsultants.

In this article we've looked at a number of factors that can impair the utility of profit numbers, and we've come away cautious. But there are plenty of other ways to inform your opinion of a company. Some people consider a high return on equity to be a good sign of a quality business. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

Valuation is complex, but we're here to simplify it.

Discover if European Innovation Solutions might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About ATSE:EIS

European Innovation Solutions

Provides consulting services in Greece, Bulgaria, Kazakhstan, Cyprus, Czech Republic, Romania, Albania, and Croatia.

Flawless balance sheet and fair value.

Market Insights

Advertisement

Community Narratives

Kodiak AI - a potential 100 bagger opportunity?

Fair Value US$14.00|44.7% undervalued

DA

Community Contributor

A Fair Price for a Great Business Facing Real Threats

Fair Value US$383.06|10.4% undervalued

IM

Community Contributor

AXON And Shopify Integration Will Unlock Global Mobile Advertising

Fair Value US$646.30|12.4% undervalued

AN

Based on Analyst Price Targets