- Greece

- /

- Metals and Mining

- /

- ATSE:ELHA

It's A Story Of Risk Vs Reward With Elvalhalcor Hellenic Copper and Aluminium Industry S.A. (ATH:ELHA)

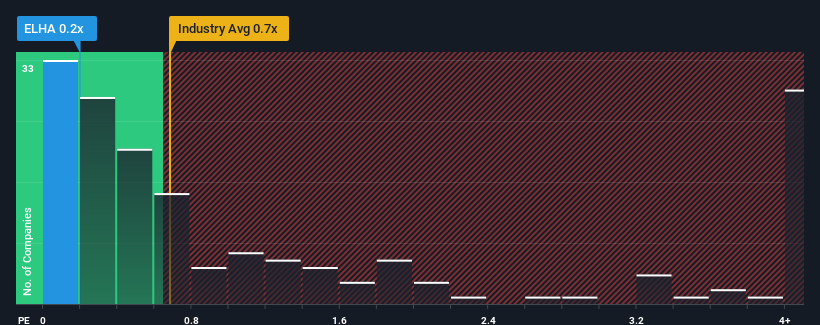

There wouldn't be many who think Elvalhalcor Hellenic Copper and Aluminium Industry S.A.'s (ATH:ELHA) price-to-sales (or "P/S") ratio of 0.2x is worth a mention when the median P/S for the Metals and Mining industry in Greece is very similar. Although, it's not wise to simply ignore the P/S without explanation as investors may be disregarding a distinct opportunity or a costly mistake.

View our latest analysis for Elvalhalcor Hellenic Copper and Aluminium Industry

How Elvalhalcor Hellenic Copper and Aluminium Industry Has Been Performing

For example, consider that Elvalhalcor Hellenic Copper and Aluminium Industry's financial performance has been poor lately as its revenue has been in decline. One possibility is that the P/S is moderate because investors think the company might still do enough to be in line with the broader industry in the near future. If not, then existing shareholders may be a little nervous about the viability of the share price.

Although there are no analyst estimates available for Elvalhalcor Hellenic Copper and Aluminium Industry, take a look at this free data-rich visualisation to see how the company stacks up on earnings, revenue and cash flow.Do Revenue Forecasts Match The P/S Ratio?

There's an inherent assumption that a company should be matching the industry for P/S ratios like Elvalhalcor Hellenic Copper and Aluminium Industry's to be considered reasonable.

Taking a look back first, the company's revenue growth last year wasn't something to get excited about as it posted a disappointing decline of 15%. Even so, admirably revenue has lifted 48% in aggregate from three years ago, notwithstanding the last 12 months. Accordingly, while they would have preferred to keep the run going, shareholders would definitely welcome the medium-term rates of revenue growth.

Comparing that recent medium-term revenue trajectory with the industry's one-year growth forecast of 2.8% shows it's noticeably more attractive.

With this information, we find it interesting that Elvalhalcor Hellenic Copper and Aluminium Industry is trading at a fairly similar P/S compared to the industry. It may be that most investors are not convinced the company can maintain its recent growth rates.

The Final Word

It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

We didn't quite envision Elvalhalcor Hellenic Copper and Aluminium Industry's P/S sitting in line with the wider industry, considering the revenue growth over the last three-year is higher than the current industry outlook. It'd be fair to assume that potential risks the company faces could be the contributing factor to the lower than expected P/S. While recent revenue trends over the past medium-term suggest that the risk of a price decline is low, investors appear to see the likelihood of revenue fluctuations in the future.

Having said that, be aware Elvalhalcor Hellenic Copper and Aluminium Industry is showing 3 warning signs in our investment analysis, and 1 of those is concerning.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Valuation is complex, but we're here to simplify it.

Discover if Elvalhalcor Hellenic Copper and Aluminium Industry might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ATSE:ELHA

Elvalhalcor Hellenic Copper and Aluminium Industry

Elvalhalcor Hellenic Copper and Aluminium Industry S.A.

Solid track record with excellent balance sheet.

Similar Companies

Market Insights

Community Narratives