Advertisement

- Greece

- /

- Construction

- /

- ATSE:GEKTERNA

Here's Why GEK TERNA Holdings Real Estate Construction (ATH:GEKTERNA) Is Weighed Down By Its Debt Load

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We note that GEK TERNA Holdings, Real Estate, Construction S.A. (ATH:GEKTERNA) does have debt on its balance sheet. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

View our latest analysis for GEK TERNA Holdings Real Estate Construction

How Much Debt Does GEK TERNA Holdings Real Estate Construction Carry?

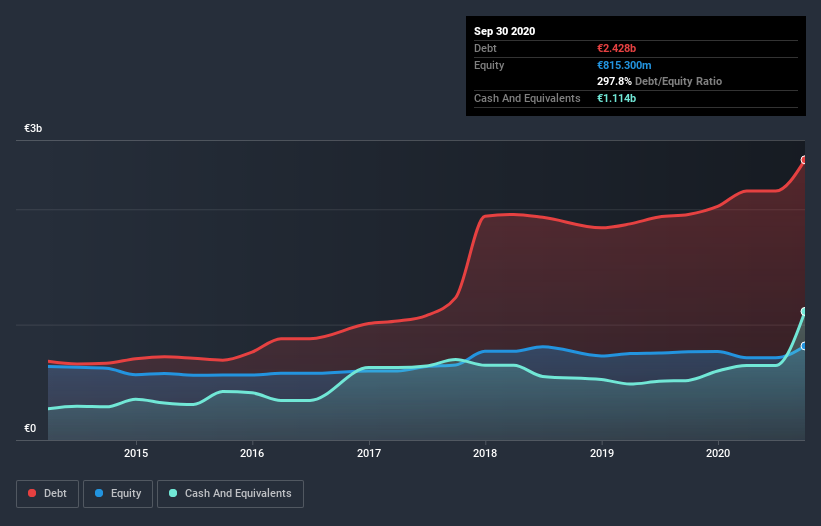

The image below, which you can click on for greater detail, shows that at September 2020 GEK TERNA Holdings Real Estate Construction had debt of €2.41b, up from €1.95b in one year. However, it does have €1.11b in cash offsetting this, leading to net debt of about €1.29b.

How Healthy Is GEK TERNA Holdings Real Estate Construction's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that GEK TERNA Holdings Real Estate Construction had liabilities of €907.6m due within 12 months and liabilities of €2.87b due beyond that. Offsetting these obligations, it had cash of €1.11b as well as receivables valued at €557.7m due within 12 months. So it has liabilities totalling €2.11b more than its cash and near-term receivables, combined.

The deficiency here weighs heavily on the €743.8m company itself, as if a child were struggling under the weight of an enormous back-pack full of books, his sports gear, and a trumpet. So we'd watch its balance sheet closely, without a doubt. At the end of the day, GEK TERNA Holdings Real Estate Construction would probably need a major re-capitalization if its creditors were to demand repayment.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

While we wouldn't worry about GEK TERNA Holdings Real Estate Construction's net debt to EBITDA ratio of 4.6, we think its super-low interest cover of 1.8 times is a sign of high leverage. It seems clear that the cost of borrowing money is negatively impacting returns for shareholders, of late. Given the debt load, it's hardly ideal that GEK TERNA Holdings Real Estate Construction's EBIT was pretty flat over the last twelve months. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if GEK TERNA Holdings Real Estate Construction can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Considering the last three years, GEK TERNA Holdings Real Estate Construction actually recorded a cash outflow, overall. Debt is far more risky for companies with unreliable free cash flow, so shareholders should be hoping that the past expenditure will produce free cash flow in the future.

Our View

To be frank both GEK TERNA Holdings Real Estate Construction's interest cover and its track record of staying on top of its total liabilities make us rather uncomfortable with its debt levels. But at least its EBIT growth rate is not so bad. Taking into account all the aforementioned factors, it looks like GEK TERNA Holdings Real Estate Construction has too much debt. While some investors love that sort of risky play, it's certainly not our cup of tea. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. For example, we've discovered 1 warning sign for GEK TERNA Holdings Real Estate Construction that you should be aware of before investing here.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

If you decide to trade GEK TERNA Holdings Real Estate Construction, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About ATSE:GEKTERNA

Gek Terna

Engages in the construction, energy, industry, real estate, and concession businesses in Greece, the Balkans, the Middle East, Eastern Europe, North America, and internationally.

Slight with moderate growth potential.

Market Insights

Advertisement

Community Narratives

Apple: A Dying Star with an Overpriced Valuation

Fair Value US$177.34|19.1% overvalued

IN

Community Contributor

Avino a case for USD$20 per share within 5 years (assuming $3,500 gold, $100 silver and $4 copper).

Fair Value CA$26.79|86.0% undervalued

AG

Community Contributor

Riding the Defense Boom RENK Sees Revenue Climb at 15% CAGR by FY 2029

Fair Value €69.87|14.3% undervalued

CH

Community Contributor