Advertisement

- United Kingdom

- /

- Airlines

- /

- LSE:IAG

International Consolidated Airlines Group (LON:IAG) Has A Somewhat Strained Balance Sheet

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. As with many other companies International Consolidated Airlines Group S.A. (LON:IAG) makes use of debt. But should shareholders be worried about its use of debt?

When Is Debt A Problem?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. The first step when considering a company's debt levels is to consider its cash and debt together.

Check out our latest analysis for International Consolidated Airlines Group

How Much Debt Does International Consolidated Airlines Group Carry?

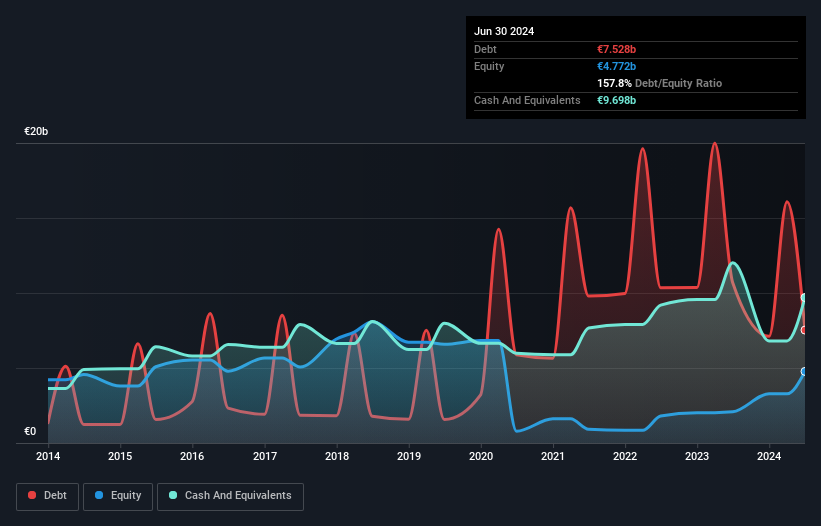

The image below, which you can click on for greater detail, shows that International Consolidated Airlines Group had debt of €7.53b at the end of June 2024, a reduction from €10.7b over a year. However, it does have €9.70b in cash offsetting this, leading to net cash of €2.17b.

How Healthy Is International Consolidated Airlines Group's Balance Sheet?

According to the last reported balance sheet, International Consolidated Airlines Group had liabilities of €21.0b due within 12 months, and liabilities of €16.7b due beyond 12 months. Offsetting these obligations, it had cash of €9.70b as well as receivables valued at €2.25b due within 12 months. So it has liabilities totalling €25.7b more than its cash and near-term receivables, combined.

This deficit casts a shadow over the €11.6b company, like a colossus towering over mere mortals. So we definitely think shareholders need to watch this one closely. At the end of the day, International Consolidated Airlines Group would probably need a major re-capitalization if its creditors were to demand repayment. Given that International Consolidated Airlines Group has more cash than debt, we're pretty confident it can handle its debt, despite the fact that it has a lot of liabilities in total.

Another good sign is that International Consolidated Airlines Group has been able to increase its EBIT by 21% in twelve months, making it easier to pay down debt. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine International Consolidated Airlines Group's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. While International Consolidated Airlines Group has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. During the last two years, International Consolidated Airlines Group produced sturdy free cash flow equating to 64% of its EBIT, about what we'd expect. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Summing Up

While International Consolidated Airlines Group does have more liabilities than liquid assets, it also has net cash of €2.17b. And it impressed us with its EBIT growth of 21% over the last year. So while International Consolidated Airlines Group does not have a great balance sheet, it's certainly not too bad. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. To that end, you should learn about the 2 warning signs we've spotted with International Consolidated Airlines Group (including 1 which can't be ignored) .

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About LSE:IAG

International Consolidated Airlines Group

Engages in the provision of passenger and cargo transportation services in the North Atlantic, Latin America, the Caribbean, Europe, Africa, the Middle East, South Asia, the Asia Pacific, and internationally.

Undervalued with proven track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Next Phase of Energy Storage: How NeoVolta Is Tackling America’s Power Crunch

Fair Value US$7.50|30.4% undervalued

MA

Community Contributor

A formidable player in AI and enterprise computing.

Fair Value US$210.00|3.0% undervalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|20.4% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.1% undervalued

TR

Community Contributor